Alternative forms of payment: A concise guide to boosting sales

When you hear "alternative payment methods," what comes to mind? We're talking about any way a customer can pay you that isn't a traditional credit or debit card. Think digital wallets, Buy Now, Pay Later plans, or direct bank transfers. For anyone running an ecommerce store, these aren't just trendy options anymore; they're critical for keeping up with what your customers actually want and preventing them from ditching their carts at the last second.

Why Alternative Forms of Payment Are a Necessity, Not a Novelty

Picture your online shop only taking Visa. You'd be slamming the door on a massive chunk of your potential audience, right? Sticking only to traditional card payments in today's world is a similar, just less obvious, misstep. Offering a variety of payment methods has moved from being a "nice-to-have" perk to a must-have for survival.

This whole shift is being pushed by one thing: customer demand. A checkout page with plenty of payment choices is like a digital welcome mat. It shows a diverse, global audience that you're ready to do business the way they want to.

Expanding Your Customer Base

Here's a reality check: not every shopper has a credit card, and even if they do, they might not want to use it for every purchase. Younger customers, for example, often gravitate toward the flexibility of Buy Now, Pay Later (BNPL) services. Meanwhile, security-focused buyers might feel safer using a digital wallet. By catering to these different preferences, you're opening your doors to shoppers your competitors might be completely missing.

Giving customers these choices has a direct, measurable impact on your business:

- Reduced Cart Abandonment: One of the top reasons people bail on a purchase is not seeing their preferred payment option at checkout.

- Increased Conversion Rates: When paying is easy and familiar, the journey from "I want this" to "It's mine" is a whole lot smoother.

- Enhanced Customer Loyalty: Getting the payment experience right builds trust and gives people a great reason to come back.

Think of it this way: Your product pages get people interested, but your checkout is where the sale is actually made. A limited set of payment options is like throwing up a hurdle right at the finish line.

Meeting Modern Expectations

We live in an age of one-click checkouts and mobile shopping. Customers are now hardwired to expect speed and convenience. Alternative payment methods are built from the ground up to provide exactly that. Digital wallets like Apple Pay or PayPal get rid of the annoying task of punching in card numbers and shipping addresses—a small tweak that can make a huge difference in conversions, especially on mobile.

Likewise, things like BNPL and direct bank transfers appeal to very specific needs. BNPL makes big-ticket items feel more affordable by splitting up the cost, while direct transfers are a simple, low-fee way to handle subscriptions or large one-off payments. When you add these tools, you aren't just slapping more buttons on your checkout page. You're building a more welcoming and effective path to purchase for everyone.

Decoding the World of Alternative Payment Methods

Think of your checkout page as the final, crucial step in a conversation with your customer. When they're ready to buy, the last thing you want is a language barrier. Only offering credit cards is like speaking a single dialect when your customers are fluent in many different payment languages. To really connect and close the sale, you have to speak their language.

Diving into alternative forms of payment isn’t just about slapping more logos on your site. It's about understanding the unique habits and needs each method serves. Let's break down the major players so you can see how they work for both you and your customers.

Digital and Mobile Wallets: The Express Lane

Digital wallets are the express checkout lanes of ecommerce. Think PayPal, Apple Pay, and Google Pay. They securely vault a customer's payment and shipping details, transforming a clunky, multi-step checkout into a simple click or tap.

For the shopper, this is pure, unadulterated convenience. No more digging for a credit card or pecking out an address on a tiny phone screen. For you, the merchant, this smooth experience is your secret weapon against cart abandonment, especially for mobile shoppers who live and die by speed.

A clunky checkout is a conversion killer. Digital wallets remove that friction, turning a potential moment of frustration into a seamless transaction. That builds confidence and keeps customers coming back.

Buy Now, Pay Later: Turning Browsers into Buyers

Services like Klarna and Afterpay have completely changed how people approach bigger purchases. They work like instant, interest-free installment plans, letting shoppers get their products right away and spread the cost over several weeks or months. This is Buy Now, Pay Later (BNPL), and it's a game-changer.

This model is incredibly powerful for overcoming price hesitation. A $400 jacket might seem steep, but when it's framed as four easy payments of $100, it suddenly feels much more attainable. The massive growth of BNPL is proof that it's reshaping online shopping, giving people flexibility without needing a traditional credit card. In fact, by 2025, the global BNPL market is expected to hit a staggering US$560.1 billion in transaction volume—a clear signal of a huge shift in how people prefer to pay.

Direct Bank Transfers: The Reliable Workhorse

Often called ACH (Automated Clearing House) payments in the U.S., direct bank transfers are the steady, reliable workhorse of the payment world. Instead of riding the card rails, money moves straight from the customer's bank account to yours.

It might not be as flashy as BNPL, but for certain business models, ACH is a cost-effective beast:

- Subscription Services: For recurring bills, ACH payments fail far less often than credit cards, which expire, get lost, or are declined.

- High-Ticket Items: The processing fees are typically a fraction of credit card rates, saving you a small fortune on large transactions.

The trade-off is usually speed; these payments can take a few business days to clear. But for businesses that value low costs and reliability over instant gratification, they're an essential part of the toolkit.

Cryptocurrencies: A Niche with Finality

Cryptocurrencies like Bitcoin and Ethereum are still a new frontier, but they bring something unique to the table. They run on a decentralized network, making them global, secure, and—most importantly—irreversible. Once a crypto transaction is confirmed on the blockchain, it's final. There are no chargebacks.

This finality makes crypto an intriguing choice for merchants in high-risk industries or those navigating the complexities of cross-border sales where fraud is a constant headache. While it's still a niche audience, adoption is growing among tech-savvy shoppers who value the privacy and control it gives them. For the right customer, seeing a crypto option is a powerful trust signal.

Localized Payment Options: Speaking the Global Language

Once you start selling internationally, you'll quickly realize that how people pay is intensely local. In the Netherlands, iDEAL (a bank transfer system) is king. Across parts of Africa and Asia, mobile money is the everyday standard.

Ignoring these local preferences is like putting up a "closed for business" sign in entire countries. Offering familiar, trusted payment methods is non-negotiable for any business with global ambitions. To really get this right, you'll want to see how a strong CRM with mobile money integration can pull everything together, streamlining your operations and unlocking new markets.

A Practical Comparison of Modern Payment Options

Picking the right payment options for your business isn't just about what’s convenient for customers—it's a critical financial decision that hits your bottom line. Every method comes with its own unique blend of costs, settlement speeds, and risks that can either help or hinder your cash flow. If you don't understand the trade-offs, you could be leaving money on the table or opening yourself up to unnecessary headaches.

To really get this right, you have to look past the marketing and compare these alternative forms of payment on the metrics that actually matter. We're talking about everything from the percentage you'll pay on every sale, to how long you have to wait for your money, and who’s on the hook when something goes wrong.

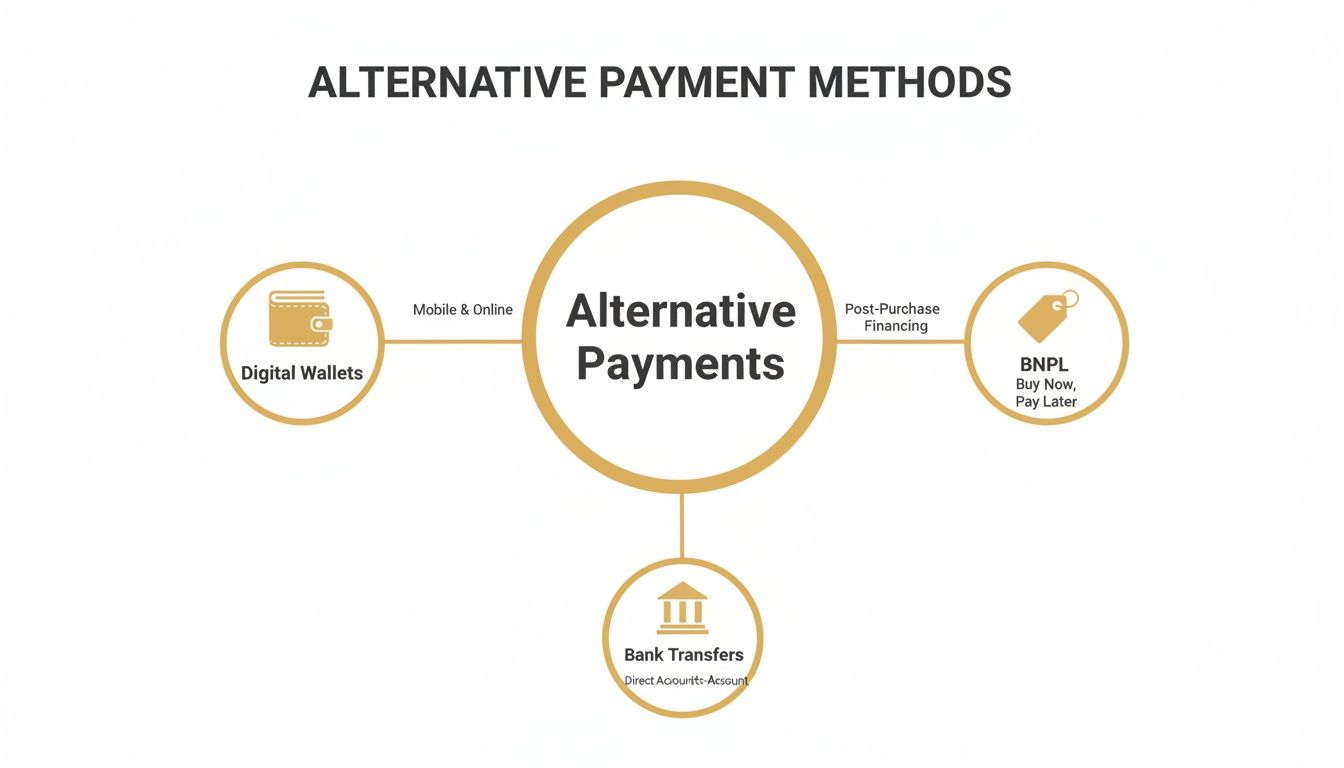

This diagram breaks down the main categories of alternative payments that smart businesses are using to keep customers happy and their operations running smoothly.

As you can see, things like digital wallets, BNPL, and direct bank transfers are the new cornerstones of a solid payment strategy, each solving a different problem for a different type of customer.

To make this even clearer, let's break down how these popular payment methods stack up against each other in a side-by-side comparison.

Alternative Payment Methods Comparison for Merchants

This table offers a quick, at-a-glance look at the most popular payment methods, comparing them across the factors that matter most to your business: fees, how quickly you get paid, and your exposure to chargebacks.

| Payment Method | Typical Merchant Fees | Settlement Speed | Chargeback Risk | Best For |

|---|---|---|---|---|

| Digital Wallets | 2.5% – 3.5% | Instant to 1-2 days | Medium (tied to underlying card) | Mobile-first businesses, boosting checkout conversion rates. |

| ACH/Bank Transfers | 0.8% or low flat fee | 3-5 business days | Low | Subscription services, B2B, and high-value transactions. |

| BNPL | 4% – 6% | Instant | Very Low (provider assumes risk) | Retailers selling high-ticket items, increasing AOV. |

| Cryptocurrency | 0.5% – 1% | Minutes to hours | None (irreversible) | Niche businesses with tech-savvy customers, international sales. |

Each option presents a unique value proposition. Digital wallets are all about a frictionless customer experience, while ACH is the clear winner for cost-conscious, recurring revenue models. BNPL and crypto, on the other hand, tackle specific challenges like affordability and fraud elimination.

Dissecting the Financials: Fees and Payouts

The most obvious difference you'll notice is the cost. Traditional credit cards are the benchmark, usually costing merchants somewhere between 2.5% to 3.5% per transaction. That fee pays for the whole network of banks and processors working behind the scenes.

On the complete opposite end of the spectrum, direct bank transfers (ACH) are the undisputed low-cost champ. Their fees are often just a small flat rate or a tiny percentage (around 0.8%), making them a fantastic deal for big-ticket sales or recurring subscriptions. The catch? You have to wait. Settlement can take 3-5 business days, which might be too slow for businesses that need cash in hand quickly.

Digital wallets like PayPal or Apple Pay typically fall right in line with credit card fees, mostly because they’re just a slick interface sitting on top of a customer’s linked card. Their real power isn’t saving you money on fees—it’s saving you sales by making checkout ridiculously easy.

Buy Now, Pay Later services are a completely different animal. Yes, their fees are higher, often in the 4% to 6% range. But that higher cost is an investment in changing how people shop, unlocking sales and boosting average order values from customers who might have walked away otherwise.

Navigating Risk: Fraud and Chargebacks

Beyond the fees, the next big question is about risk. Specifically, who eats the cost when a transaction is fraudulent or a customer files a dispute? This is where alternative payments really start to show their unique strengths.

With a standard credit card payment, the merchant is almost always on the hook for chargebacks. When a customer disputes a charge, the burden falls on you to prove it was legit—a frustrating, uphill battle that you often lose.

This is exactly where some alternative methods flip the script:

Buy Now, Pay Later: This is a game-changer. Most BNPL providers, like Klarna or Affirm, assume 100% of the fraud and chargeback risk. If a sale turns out to be fraudulent, they take the hit, not you. This protection is a huge part of why their fees are higher and a massive relief for merchants in high-risk industries.

Cryptocurrency: Crypto payments are final. Once a transaction is confirmed on the blockchain, it's irreversible. It simply cannot be charged back, which completely wipes out that specific type of fraud. The trade-off, of course, is dealing with price volatility.

Direct Bank Transfers: While it's possible for an ACH payment to be reversed in certain cases (like an unauthorized withdrawal), the rate of fraud-related chargebacks is dramatically lower than with credit cards.

Digital wallets are more of a mixed bag. They beef up security with things like tokenization and fingerprint ID, which definitely helps cut down on fraud. But at the end of the day, the chargeback rules are still tied to whatever card the customer used to fund the wallet.

Ultimately, there's no single "best" answer. The right mix depends entirely on your business model, who your customers are, and how much risk you're willing to stomach. A subscription box company might lean heavily on the low cost of ACH, while an online furniture store could see a huge ROI from a risk-free BNPL option. Getting this balance right turns your payment strategy from a simple necessity into a real competitive advantage.

Building Your Strategic Payment Mix

Picking which payment methods to offer isn't just about plastering logos on your checkout page. It's about crafting a smart strategy that actually helps you hit your business goals. A poorly chosen payment mix can kill sales and leave customers frustrated, but the right one can become a serious engine for growth.

So, where do you start? The best approach is to answer a few basic questions about your business and who you're selling to. Think of it like drawing up a blueprint before you start building. Who are your customers, really, and how do they like to pay for things? Are you selling cheap monthly subscriptions or expensive one-off products? The answers will point you in the right direction.

Aligning Payments with Your Business Model

Your business model is the most important piece of this puzzle. A payment method that’s a game-changer for one company could be a total dud for another. The trick is to match the payment method’s perks to what your business actually needs to thrive.

Let’s walk through a few real-world examples to see how this plays out:

The Fast-Growing DTC Brand: Imagine a direct-to-consumer store selling trendy clothes. Their success hinges on impulse buys and getting people to spend more per visit. For them, Buy Now, Pay Later (BNPL) is a must-have. It takes the sting out of a big purchase, turning a $200 cart into four easy $50 payments, which can do wonders for converting shoppers with bigger carts.

The Subscription Box Service: This kind of business is all about recurring revenue and keeping subscribers happy. Payment reliability is everything. Their secret weapon? ACH/direct debit. Credit cards expire and get declined all the time, causing failed payments and customer churn. ACH, on the other hand, is a stable, low-cost way to keep revenue flowing smoothly month after month.

The Global Software (SaaS) Company: A SaaS business with customers all over the world needs to be flexible. Their strategy has to include well-known digital wallets like PayPal that everyone recognizes, plus local favorites like iDEAL in the Netherlands. This simple step removes a huge point of friction for international buyers.

Understanding Your Customer Demographics

Beyond your business model, you have to know your audience inside and out. Different groups of people have completely different payment habits and expectations. If you get this wrong, you're practically inviting customers to abandon their carts.

For instance, younger shoppers—Millennials and Gen Z—are all about BNPL and mobile wallets. If that's who you're selling to, not offering those options is like trying to speak to them in a foreign language. It's also smart to think about how your pricing structure affects their choices. For service businesses, this might mean exploring various tutoring pricing models to see what clicks with clients.

Your payment options send a clear message about how well you know your customers. When you offer their favorite ways to pay, it shows you get them—and that you're making it as easy as possible to buy from you.

Simplifying Integration with Modern Gateways

The great news? Adding all these powerful payment options isn't the technical nightmare it used to be. Modern payment gateways have made the whole process incredibly simple.

Platforms like Stripe essentially act as a command center, letting you switch on new payment methods with just a few clicks in your dashboard. That means you can add Apple Pay, Klarna, or ACH transfers without needing an army of developers. These gateways handle all the messy stuff—security, compliance, and the technical backend—so you can focus on your strategy.

If you’re already on a major processor, checking out the Stripe signup process is a great way to see just how easy this has become. This plug-and-play approach lets you test, learn, and adjust your payment mix on the fly as your business and your customers evolve.

Managing Disputes in a Multi-Payment Ecosystem

Offering a rich variety of alternative forms of payment is a fantastic way to win over more customers, but it can feel like you’re juggling more risks at the same time. Each new payment method brings its own unique rules, vulnerabilities, and dispute processes into the mix. This complexity can quickly spiral out of control, turning a smart growth strategy into a major operational headache.

It's a common misconception that methods like bank transfers or crypto eliminate customer disputes entirely. While they do cut down on traditional chargebacks, they don't erase the root causes of disputes. A product might not arrive, or a service might not live up to its promises—these things are just part of doing business, no matter how a customer pays. This makes a unified, proactive defense strategy absolutely essential.

The New Landscape of Customer Disputes

In a world full of payment options, disputes are no longer a simple, one-size-fits-all problem. Each payment type follows a different path. A customer unhappy with a purchase made via a digital wallet might file a chargeback through their linked credit card. Meanwhile, a BNPL user could open a dispute directly with the financing company.

This fragmentation creates a huge challenge for merchants. Suddenly, you're trying to monitor multiple channels, each with its own timelines and evidence requirements. It's easy to miss a critical notification from one provider while you're focused on another, leading to automatic losses, dings against your merchant accounts, and lost revenue.

Think of it like this: defending against disputes is like guarding a house. In the past, you only had to watch the front door (credit card chargebacks). Now, with alternative payments, you have to monitor every window, side door, and potential entry point at once.

Chargeback Alerts: A Crucial Safety Net

This is exactly where a centralized chargeback alert system becomes your most valuable tool. Instead of trying to watch every entry point yourself, an alert platform acts as a universal security system for your business. It plugs directly into major card networks to catch disputes the moment a customer calls their bank—before they ever escalate into a formal, damaging chargeback.

This early warning is a game-changer. It gives you a 24- to 72-hour window to step in and fix the problem, usually by issuing a refund. By doing so, you solve several critical problems at once:

- You prevent the chargeback: The dispute is stopped dead in its tracks and never officially filed against you.

- You protect your dispute ratio: Keeping your chargeback numbers low is vital for maintaining good standing with payment processors and avoiding hefty penalties.

- You automate your defense: The system can handle incoming alerts in real-time based on rules you set, freeing up your team from hours of manual work.

This protection works no matter how the initial payment was made. If a customer used Apple Pay funded by a Visa card, the alert system still intercepts the Visa dispute before it hits your account. This universal coverage is what makes it an indispensable part of any modern, multi-payment strategy.

Building a Resilient Defense Strategy

A truly robust defense isn't just about reacting to fires; it’s about proactively managing risk across your entire payment portfolio. When you combine a diverse set of alternative forms of payment with a powerful alert system, you create a far more resilient financial operation. You can confidently offer the payment choices your customers demand, knowing you have a safety net ready to catch the inevitable disputes that come with growth.

This forward-thinking approach is especially critical during high-volume sales periods when dispute rates tend to spike. To make sure you’re fully prepared, it’s worth reviewing expert guidance on winning chargeback representment during Q4 and other peak seasons. Ultimately, a smart dispute management system lets you reap all the rewards of payment diversity without getting buried by the risks, ensuring your business stays protected and profitable.

Future-Proofing Your Payment Strategy

The way we pay for things is always in motion. What seems new and exciting today quickly becomes the standard tomorrow. A smart payment strategy isn’t about jumping on every new bandwagon; it's about building a system that’s flexible, puts your customers first, and is ready to adapt. You want your checkout to evolve with your customers, not box them into old habits.

Keeping an eye on what's coming next is crucial. New technologies are already starting to change what a "smooth transaction" even means, and being aware of them early gives you a real leg up.

Key Trends to Watch

Three major shifts are starting to bubble up that will likely define the future of how we buy and sell.

- Central Bank Digital Currencies (CBDCs): Picture a digital dollar, backed by the government, that combines the security of traditional money with the instant speed of electronic payments. They're still in the early days, but CBDCs could eventually create a brand new, super low-cost way to move money.

- Biometric Payments: This is the stuff of sci-fi made real—paying with a fingerprint, a quick facial scan, or even the sound of your voice. Biometrics point to a future where payments are both incredibly secure and almost invisible, getting rid of cards and phones altogether.

- Real-Time Payment Networks: Systems like FedNow are making instant, around-the-clock bank transfers the new normal. For merchants, this means money settles immediately. For customers, it means instant confirmation. It's a game-changer for cash flow.

The best payment strategies are never set in stone; they’re living, breathing parts of your business. The real key to long-term success is constantly looking at your payment mix, checking customer data, and seeing how it all impacts your costs and conversions.

Creating an Adaptable Payment Ecosystem

Future-proofing isn't about having a crystal ball. It’s about building a business that’s nimble enough to react when the future actually shows up.

This journey starts by regularly digging into your checkout analytics. Where are customers bailing? Are certain alternative forms of payment leading to bigger shopping carts? Your own data is the best map you'll ever have.

From there, make sure your operational foundation is solid. The more payment options you add, the more complex it gets to manage disputes and keep your accounts safe. Strong systems aren't just a nice-to-have; they're essential for a healthy business. It's also vital to stay current on best practices. You can explore expert insights and strategies on the Disputely blog to keep your operational knowledge sharp.

In the end, a future-proof strategy comes down to giving customers choices while protecting your revenue. By staying aware of what’s on the horizon and keeping your payment infrastructure flexible and well-managed, you’ll be ready to meet your customers’ expectations—not just today, but for years to come.

Frequently Asked Questions

Jumping into the world of alternative payments can feel a bit overwhelming, so let's clear up some of the most common questions that pop up.

Which Alternative Payment Methods Should I Prioritize?

If you're an ecommerce store, your first stop should be digital wallets. Think Apple Pay, Google Pay, and PayPal. The checkout experience is incredibly smooth—often just one click—which can dramatically boost your conversion rates, especially for shoppers on their phones.

After that, look at Buy Now, Pay Later (BNPL) options. These are a game-changer for selling higher-ticket items or just encouraging customers to add a little more to their cart. And if you run a subscription business or deal with recurring billing, ACH/direct debit is a must-have for its low cost and for cutting down on failed payments from expired cards. The perfect setup really comes down to who your customers are and what you sell.

Do These New Payment Options Eliminate Chargebacks?

Not completely, but they can change the game. Some payment methods, particularly "push" payments like bank transfers, are pretty much final and have a very low risk of disputes. Many other alternative forms of payment, however, just move the risk around.

A great example is BNPL. Most providers take on the fraud risk themselves, which is a huge weight off a merchant's shoulders. But that doesn't stop a customer from disputing a charge because they weren't happy with the product. This is exactly why having a chargeback alert service is still so important. It catches disputes at the source, regardless of how the customer paid, so you can handle them before they escalate and hurt your business.

How Difficult Is It to Add New Payment Options to My Website?

Honestly, it's probably much easier than you think. These days, payment processors like Stripe and Adyen, and ecommerce platforms like Shopify, have done the heavy lifting for you.

For many of the most popular options, adding them is as simple as flipping a switch in your settings. The real work isn't on the technical side; it's about making smart choices. You'll want to think through which methods make the most sense for your audience and get a handle on the different fees and payout schedules for each one.

Stop letting preventable chargebacks eat into your profits. Disputely connects you directly to the card networks, giving you real-time alerts on disputes. This gives you the chance to issue a refund and protect your merchant accounts from damage. See how much you can save with Disputely.