The Ultimate Guide to Alternative Payment Methods for Merchants

When you hear the term alternative payment methods (APMs), it simply means any way a customer can pay you that isn’t a traditional credit card like Visa or Mastercard. We're talking about everything from digital wallets and Buy Now, Pay Later (BNPL) services to direct bank transfers.

These aren't just fringe options anymore; they are fundamentally reshaping the checkout experience for millions of people online and in stores every day.

What Are Alternative Payment Methods and Why Do They Matter?

Think of your checkout page as a multi-lane highway. For years, the only real option was the credit card lane. It worked, but it could get congested, leading to frustrated drivers—your customers—who might just abandon their trip altogether.

Alternative payment methods are like opening up all the other lanes.

Digital wallets like Apple Pay and Google Pay are the express toll lanes—fast, one-tap payments for people in a hurry. Services like Klarna or Afterpay become the carpool lane, letting customers split the cost of their purchase into smaller, more manageable payments over time. And direct bank transfers are like a reliable local route, moving money straight from a customer’s bank to yours without ever touching the card networks.

Customers Now Expect More Choices

Today’s shoppers have come to expect this kind of flexibility. The data is crystal clear: 56% of shoppers will leave a site for good if their favorite payment method isn't available. A limited checkout is no longer a minor inconvenience; it's a direct hit to your sales and customer loyalty.

And this isn't just a fleeting trend. In many parts of the world, APMs are already the dominant way to pay.

- Digital wallets now make up 39% of all ecommerce transaction volume in North America, overtaking credit cards.

- In the Netherlands, the local bank transfer system, iDEAL, is used for a staggering 73% of online purchases.

- Brazil’s real-time payment network, Pix, was adopted by 74% of the population just two years after it launched.

Trying to sell internationally without offering local payment methods is like setting up shop in a foreign country but refusing to accept the local currency. You're telling potential customers that you don't really understand their needs or value their business.

Before we dive deeper, here's a quick look at the major APM categories you'll encounter.

Quick Overview of Popular Alternative Payment Methods

| Payment Method Category | Best For | Popular Regions |

|---|---|---|

| Digital & Mobile Wallets | Quick, mobile-friendly checkouts for everyday purchases and subscriptions | North America, Asia-Pacific, Europe |

| Buy Now, Pay Later (BNPL) | High-ticket items, younger demographics, and increasing conversion rates | North America, Europe (especially UK, Germany) |

| Bank Transfers & Debit | Large purchases, B2B transactions, and regions with low card penetration | Europe (iDEAL, Giropay), Latin America (Pix) |

| Cash-Based Vouchers | Reaching unbanked customers or those who prefer paying with cash | Latin America (Boleto), Europe (Paysafecard) |

| Cryptocurrency | Niche markets, tech-savvy customers, and cross-border transactions | Global (Varies by adoption rate) |

This table gives you a bird's-eye view, but each of these methods comes with its own set of rules, benefits, and risks that we'll explore.

It's More Than Just a Sale—It's a Strategy

Adding the right mix of payment options does more than just cut down on abandoned carts. It can be a powerful tool for growth, helping you reach new customers in markets where credit cards aren't the norm. For more tips on growing your business, check out some of the ecommerce strategies on our blog.

But this expansion also brings new challenges. Every payment method has a different risk profile, especially when it comes to disputes and fraud. While APMs can be a massive engine for growth, they require a smarter, more flexible approach to managing payment risk. This guide will walk you through both the incredible opportunities and how to keep your business protected along the way.

A Closer Look at Digital Wallets

Think of digital wallets like Apple Pay, Google Pay, and Alipay as more than just a digital copy of your physical wallet. They're a complete overhaul of how we pay, acting as secure hubs for our funds and making one-tap checkouts the new normal.

These platforms have quickly become a dominant force in the world of alternative payments, fundamentally changing how both online and in-person transactions happen. Their share of the e-commerce pie is expected to jump from 22% to a massive 65% by 2030. In that same period, their use at the physical point of sale is projected to climb from just 3% to 45%. For a deeper dive into these trends, check out McKinsey's Global Payments Report.

How Digital Wallets Boost Your Conversions

For customers, the magic of digital wallets is simple: convenience. Nobody enjoys fumbling for their credit card and punching in a 16-digit number, expiration date, and CVV. With a digital wallet, a single tap or a quick facial scan is all it takes.

This seamless experience directly impacts your bottom line. By smoothing out the biggest bumps in the checkout process, digital wallets are a powerful tool against cart abandonment. This is especially true for mobile shoppers, where a complicated checkout can easily mean a lost sale.

The Security Perks for Your Business

Beyond the slick user experience, digital wallets come packed with security features that protect everyone involved. This is a huge reason they’ve become a trusted alternative to traditional card payments.

- Tokenization: When a customer loads a card into their wallet, the service swaps the real card number for a unique, encrypted code—a token. This token is what gets used for transactions, so you never have to handle or store the customer's sensitive card info. This massively cuts down your risk of a data breach.

- Biometric Authentication: Nearly all wallet payments require a fingerprint, face ID, or a device-specific PIN to go through. This extra step confirms the user is who they say they are, stopping most unauthorized purchases in their tracks.

For merchants, these security measures aren't just abstract concepts. They lead to fewer instances of clear-cut fraud, which can improve your reputation with payment processors and save you real money.

The Hidden Wrinkle: Wallet-Related Disputes

While the benefits are clear, digital wallets bring a new layer of complexity to payment disputes. The transaction is still funded by an underlying credit or debit card, but the way a dispute unfolds can be quite different.

When a customer disputes a wallet purchase, the process might not follow the standard chargeback route. Instead of a formal chargeback hitting your account, you might get an early warning alert directly from the card networks. This gives you a very short window—often just 24 to 72 hours—to issue a refund and stop the issue from escalating into a full chargeback that harms your merchant account.

This means that old-school, manual dispute management just doesn't cut it anymore. You need a proactive, automated system to catch and handle these alerts immediately. And for those using specific wallet services, it's also smart to understand any associated costs. Tools like a Cash App fee calculator can help shed light on that.

The Power of Account-to-Account Payments

While digital wallets offer a secure layer on top of a customer's card, there's another class of payment methods that skips the card networks altogether. These are Account-to-Account (A2A) payments, and they create a direct line for money to flow from a customer's bank account right into yours.

Think of the typical card payment journey as a scenic, winding road. It has several stops along the way—the card networks, the processors, the issuing banks—and each one adds a little time and a small toll. A2A payments, on the other hand, are like a brand-new express tunnel built straight from the customer's bank to your business. This category covers everything from familiar methods like direct debit and ACH to the incredibly popular real-time systems like Pix in Brazil and UPI in India.

The Benefits of a Direct Connection

For businesses, that direct route offers some serious perks, especially if you rely on recurring revenue. Because you’re cutting out the card network middlemen, transaction fees are often much lower than what you’d pay for standard card processing. This makes a huge difference on large or recurring payments, where those percentage-based fees can really start to sting.

The other massive win is the drop in involuntary churn. Subscription companies lose customers all the time, not because people want to leave, but simply because a credit card expires or gets replaced. A2A payments are linked to a bank account—which doesn't have an expiration date—meaning fewer failed payments, better customer retention, and more predictable revenue.

- Lower Transaction Costs: By sidestepping card network fees, you can seriously cut down on your cost of getting paid.

- Reduced Involuntary Churn: Bank accounts don't expire. This makes A2A a game-changer for subscriptions and recurring billing.

- Increased Security: Payments usually require the customer to authenticate directly with their bank, adding a powerful layer of security.

A New Landscape for Dispute Management

But this direct connection completely changes the risk equation. The highly structured chargeback process you see with credit cards simply doesn't exist here. Instead, A2A disputes are sorted out directly between the banks, which can lead to sudden, irreversible bank reversals.

When a customer disputes an A2A payment, the funds can be pulled straight out of your account with almost no warning and very little chance to plead your case. There's no formal representment process, making every single dispute a much bigger threat. Too many reversals can get your business flagged as high-risk, which could even jeopardize your relationship with your payment processor.

Because A2A disputes are so direct and immediate, a proactive defense is non-negotiable. Waiting for a reversal to happen is too late; you need to know about potential issues the moment they arise.

Why Early Warnings Are Essential

This is where a solid alert system becomes your best friend. Integrating a service that gives you early warnings on disputes provides a critical heads-up before a bank reversal hits. It gives you a window to engage with the customer, solve their problem, and issue a refund if needed—all while preventing the dispute from ever becoming a black mark on your processing history.

This proactive approach is a cornerstone of modern dispute management. If you’re on a platform like Stripe, integrating with an alert system is one of the smartest moves you can make to safeguard your business.

The global shift toward A2A is happening fast. These payments are fueling real-time economies everywhere, and the numbers are staggering. Projections show that alternative payment methods, with A2A leading the charge, are on track to make up 58% of all global ecommerce transactions by 2028. You can see how these systems work in practice by checking out guides on platforms like PayNow for Business in Singapore.

This growth is backed by over 70 countries that now operate real-time payment systems. This trend is pushing cross-border volumes from an estimated $194.6 trillion in 2024 to a projected $320 trillion by 2032. As Visa’s own research highlights, we are seeing a massive rise of cardless transactions that businesses can't afford to ignore.

Digging into BNPL and Other Niche Payment Options

Once you move past the instant gratification of digital wallets and the straightforward nature of A2A payments, you’ll find a fascinating world of specialized payment methods built for specific buying habits. The undisputed star of this category is Buy Now, Pay Later (BNPL), a method that has completely reshaped how people think about bigger purchases.

Think of services like Klarna, Affirm, or Afterpay as the 21st-century version of layaway, but with a game-changing twist: your customer gets their product right away. For a business, this isn't just another way to get paid—it’s a powerful tool for boosting sales. It dismantles the mental hurdle of a hefty price tag by splitting it into a few smaller, often interest-free payments, making the purchase feel far more accessible.

This is a home run, especially with younger shoppers who often shy away from traditional credit card debt and appreciate the clear, fixed payment schedule. The data speaks for itself: businesses offering BNPL consistently see a healthy bump in their average order value (AOV) and a significant increase in sales conversions.

The flow is pretty simple, as you can see below. The BNPL provider pays you, the merchant, upfront, and then collects the installments from the customer over time.

This diagram gets to the heart of why it works so well. You get the full payment almost immediately (minus the service fees), effectively offloading the credit risk and the hassle of collections onto the BNPL company.

How Do BNPL Disputes Work?

When a customer has a problem with a BNPL purchase, things work a bit differently. Instead of a classic chargeback landing directly in your merchant account, the BNPL provider usually steps in as a mediator. They field the initial complaint from the customer, run their own investigation, and then loop you in to figure out a resolution.

This can be a bit of a mixed bag. On the one hand, it insulates you from direct chargeback hits that could damage your standing with payment processors. On the other hand, you're now playing by the BNPL provider's rules and timelines, which aren't always as clearly defined as the regulations from Visa or Mastercard.

What About Other Niche Methods?

While BNPL gets most of the attention, other niche payment methods are crucial for reaching certain customers—especially those without traditional bank accounts or who are wary of sharing financial info online.

- Cash-Based Vouchers: Think of services like Paysafecard or Brazil's popular Boleto Bancário. A customer can select this option at checkout, get a voucher or barcode, and then walk into a local convenience store or use an ATM to pay for their online order with physical cash.

- Cryptocurrencies: While still not mainstream, accepting payments in currencies like Bitcoin or Ethereum can be a big draw for a global, tech-forward audience. These transactions settle quickly and can slash the costs associated with cross-border payments.

It's important to recognize that most of these niche methods are 'push' payments. The customer is actively sending the money to you. This virtually eliminates the risk of traditional chargeback fraud because, once sent, the payment is typically final and cannot be yanked back by the customer.

The Trade-Offs to Consider

Of course, these specialized options come with their own set of pros and cons. BNPL services, for instance, charge higher transaction fees than a typical credit card payment. It's a cost you have to weigh against the very real, documented lifts in sales and AOV they can bring.

Likewise, cash vouchers and crypto can add a few extra steps to your reconciliation process. With crypto, you also have to account for volatility—the value of a payment could fluctuate between the moment of sale and when it actually settles in your account.

Ultimately, deciding to add BNPL or other niche APMs is a strategic move. It's all about knowing your audience and figuring out which options will remove friction and build the kind of trust that turns a browser into a buyer. By thoughtfully choosing the right mix, you can open up new revenue streams and connect with a wider, more diverse customer base that traditional payment methods might leave behind.

Integrating APMs and Managing Dispute Risk

Bringing alternative payment methods into your checkout is about more than just flipping a switch. It’s a strategic move that needs to balance giving customers the options they want with protecting your business from the unique risks each method brings. The real goal is to create a checkout flow that feels effortless for the shopper but gives you, the merchant, all the tools you need to safeguard your revenue.

The first step is picking a payment gateway that actually supports the APMs your customers use. A great partner won’t just give you the tech; they’ll offer real insight into which payment methods are popular in your key markets. Once you’ve made your selections, the design of the checkout page itself is critical for building trust and keeping cart abandonment rates low.

The Unique Risk Profile of Each Payment Method

While adding new payment options can open up new revenue streams, it’s important to remember that each one has its own risk profile. We’re not in the standardized world of credit card chargebacks anymore. Disputes with APMs follow different rules, different timelines, and completely different resolution paths.

Understanding these nuances is your first line of defense. A dispute from a digital wallet might come through as an early warning alert, but an issue with a Buy Now, Pay Later (BNPL) purchase is handled directly by the BNPL provider’s internal team. This fragmentation is exactly why having a single, centralized platform to manage disputes isn’t just a nice-to-have—it’s essential.

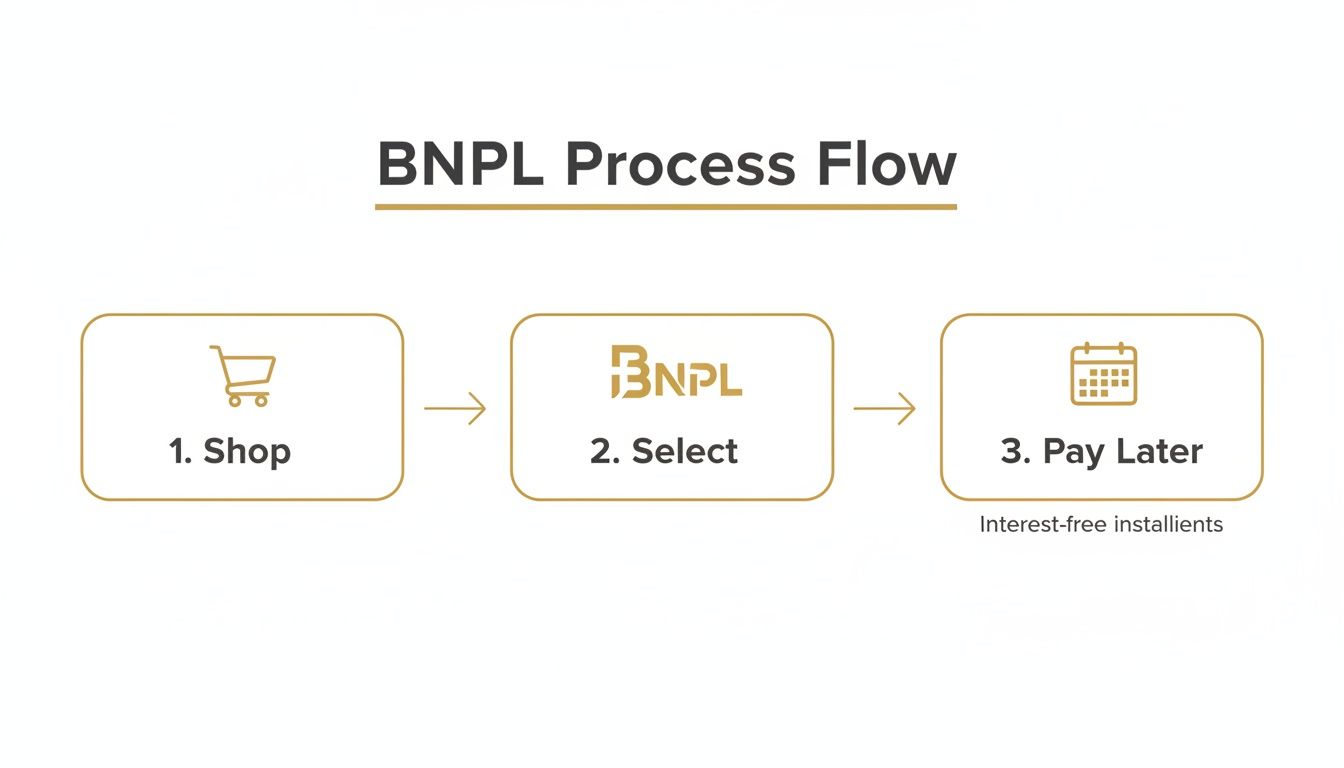

For instance, here’s the simple, three-step process a customer follows when using a BNPL service.

This flow—from shopping, to choosing the BNPL option, to paying later—is a perfect example of how risk is shifted. At the point of sale, the liability moves from you to the BNPL provider.

A Comparative Look at Dispute and Fraud Risk

To really get a handle on risk, you need to know exactly what you’re up against with each payment type. The kind of fraud you’ll see, the odds of a dispute, and the process for fighting one can be wildly different. Friendly fraud, for example, is a persistent headache with digital wallets, while account takeovers are a bigger worry for certain bank-to-bank payments.

Let's break down the risk profiles for the major APM categories to see how they stack up.

Dispute Risk Profile of Major Alternative Payment Methods

The table below offers a high-level comparison of the chargeback risks, common fraud vulnerabilities, and dispute processes you can expect from the most common APMs.

| Payment Method | Chargeback Risk Level | Common Fraud Type | Dispute Resolution Process |

|---|---|---|---|

| Digital Wallets | Medium | Friendly Fraud, Account Takeover | Often starts with early alerts (RDR, Ethoca). If missed, becomes a standard chargeback. |

| A2A / Direct Debit | Low to Medium | Unauthorized Debits, Account Takeover | Handled by banks, often resulting in direct, irreversible reversals. No formal representment. |

| Buy Now, Pay Later | Low | Synthetic ID Fraud, First-Party Misuse | Managed internally by the BNPL provider, who acts as a mediator between merchant and customer. |

| Cash-Based & Crypto | Very Low | Phishing, Social Engineering | These are "push" payments. Once sent, they are final, making traditional chargebacks nearly impossible. |

This comparison makes one thing crystal clear: a one-size-fits-all approach to managing disputes just won't cut it. Each payment method requires its own strategy, built around its unique vulnerabilities and resolution framework.

Unifying Your Defense Strategy

The sheer complexity of juggling multiple dispute channels underscores the need for automation. Trying to manually track alerts, reversals, and cases from different systems is a recipe for disaster. It's not just inefficient; it's incredibly easy to make a costly mistake. Missing a tight deadline on a digital wallet alert can instantly turn a simple refund into a damaging chargeback on your record.

This is where a unified dispute management platform becomes your most valuable player. By plugging directly into alert systems from Visa (RDR) and Mastercard (Ethoca), a solution like Disputely can intercept disputes across different payment types the second they pop up. This gives you a critical window—often just 24-72 hours—to resolve the issue with a refund, stopping the dispute from ever becoming a formal chargeback that hurts your merchant account health. For business owners dealing with account issues, understanding the reasons behind something like a Shopify Payments account hold can offer crucial perspective.

A proactive, automated system doesn't just save you from individual chargebacks. It protects your overall payment processing health, helping you avoid higher fees, processor reserves, and even the risk of account termination.

By pairing a diverse mix of payment options with an intelligent, unified dispute management system, you can confidently offer the APMs your customers love without putting your business on the line.

Common Questions About Alternative Payment Methods

Diving into the world of alternative payments can feel a bit overwhelming. As a business owner, you're probably wondering about the real-world costs, security implications, and which options will actually make a difference for your customers. Let's break down some of the most common questions that come up when merchants start exploring life beyond traditional credit cards.

Which Alternative Payment Methods Should My Store Offer?

The golden rule here is: don't offer everything. The goal isn't to clutter your checkout with dozens of logos; it's to offer the right options for your specific audience. The best place to start is with your own data.

Take a look at where your customers are coming from. If you have a growing customer base in the Netherlands, adding iDEAL isn't just a nice-to-have, it's essential. The same goes for offering Pix in Brazil. Ignoring these local favorites is like putting a barrier between you and a massive chunk of potential sales.

Demographics matter, too. If you’re selling to a younger crowd, Buy Now, Pay Later (BNPL) services like Affirm or Klarna are practically a must. They speak the language of shoppers who prefer to budget their purchases over time instead of using traditional credit. And then there are digital wallets like Apple Pay and Google Pay—at this point, they’re table stakes for almost any online store because of their sheer convenience.

The smartest move is to curate your checkout. Pick 2-3 highly relevant payment methods that align with your key customer segments. This avoids overwhelming your shoppers and shows you understand how they want to pay.

A targeted approach like this leads to a smoother experience, fewer abandoned carts, and ultimately, more sales.

Are Alternative Payment Methods More Secure Than Credit Cards?

In many cases, yes, especially at the moment the transaction happens. A lot of modern alternative payment methods have sophisticated security built right in, which is a huge step up from asking a customer to manually type in their credit card number.

Think about digital wallets. They use a couple of key technologies to protect everyone involved:

- Tokenization: Instead of transmitting the actual credit card number, the wallet sends a unique, one-time code (a "token") for that specific purchase. This means you never have to store or even see your customer's sensitive card details, which dramatically lowers your risk if you ever face a data breach.

- Biometric Authentication: Making someone use their fingerprint or Face ID to approve a purchase adds a serious layer of security. It's much harder for a fraudster to get past that than to simply use a stolen card number.

Account-to-Account (A2A) payments have a similar advantage, requiring customers to log in and approve the transaction directly with their bank. It’s a bank-grade security check right in the middle of the checkout flow.

But this doesn't mean the risk disappears entirely—it just changes. Instead of focusing on stealing card numbers, fraudsters might pivot to trying to take over a customer's entire account. On top of that, the dispute process for many APMs isn't as clear-cut as the one for Visa or Mastercard, which can create new headaches for merchants.

How Do I Handle Disputes and Refunds for APMs?

This is where things can get a bit messy, because there’s no single, universal rulebook. Every APM has its own way of handling disputes, so you need a flexible strategy to manage them.

With digital wallet transactions, a customer complaint often doesn't go straight to a chargeback. You might get an early warning through a service like Visa's RDR or an Ethoca alert. This gives you a short—but critical—window of 24 to 72 hours to issue a refund and stop the problem from escalating into a formal chargeback that dings your merchant account health.

Disputes on A2A payments, on the other hand, can be much more abrupt. Since they bypass the card networks, a customer dispute can trigger an immediate bank reversal. The money gets pulled right out of your account, often with little to no chance for you to argue your case.

BNPL providers usually step in as a middleman. They'll investigate the customer's claim and work with you on a resolution. This shields you from the direct chargeback process, but it also means you have to play by their rules and follow their specific procedures.

What Are the Costs of Accepting Alternative Payments?

The fee structures for APMs can look very different from the interchange-plus pricing you’re used to with credit cards. You’ll want to get a handle on these costs to make sure your profit margins are protected.

A2A payments, like ACH transfers, are often the cheapest route, especially for larger transactions. They usually have low, flat fees rather than taking a percentage of the sale, which can save you a ton of money over time.

Digital wallet fees typically mirror standard card-not-present rates. Because the wallet is just a secure container for a credit or debit card, the transaction still runs on those rails, and the costs reflect that.

BNPL services tend to charge a higher per-transaction percentage than credit cards. Merchants often find this is a worthwhile trade-off, however, because the cost is easily offset by the proven lift in conversion rates and the increase in average order value that BNPL is known for. Before you add any new payment button to your site, make sure you read the fine print on its fee schedule.

Protecting your business from the complex world of APM disputes requires a proactive, automated approach. Disputely provides real-time alerts for incoming disputes across all major card networks, giving you the chance to refund and prevent damaging chargebacks before they happen. Stop chargebacks and safeguard your revenue today.