Your Guide to an API for Payments and How It Works

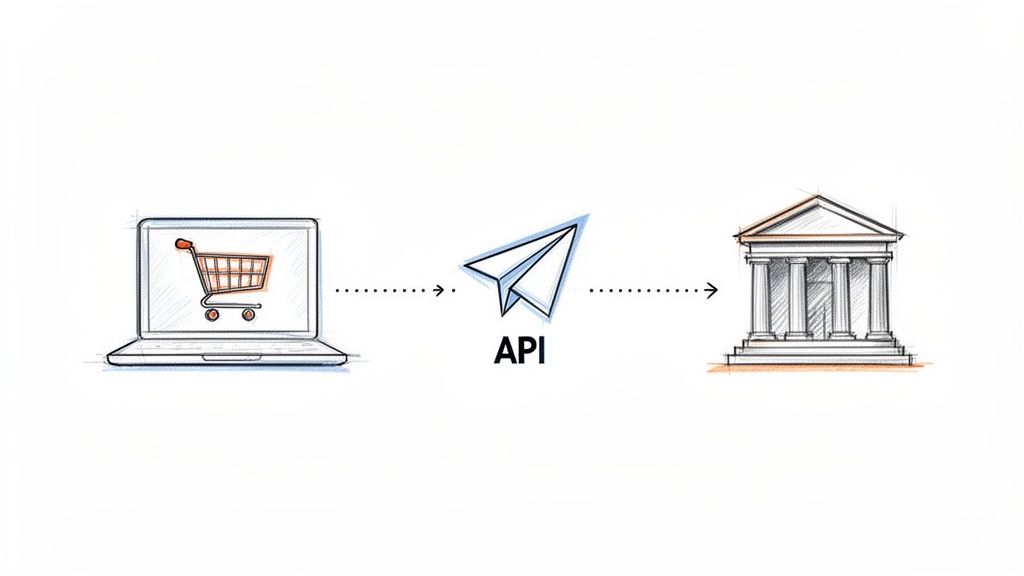

At its core, an API for payments is the digital go-between that connects your business to the vast, complex world of payment networks. It’s what lets you securely accept money from customers online.

Think of it as the ultimate translator. It allows your e-commerce store, a customer's bank, and a credit card network like Visa to all understand each other in real-time, even though they speak completely different financial languages. This bit of technology is the unsung hero powering virtually every online business.

What Is a Payment API and Why Does It Matter?

Let’s use another analogy. Imagine your checkout page is a busy restaurant kitchen. When a customer enters their card details, that's their order. The API is the waiter.

This waiter grabs the order (the payment data), runs it securely to the kitchen (the payment processor), checks that everything is correct (verifies funds), and dashes back with a confirmation (the "Payment Successful!" message). Without that waiter, the kitchen would be completely cut off from the customers. A payment API does the exact same job for your business online.

The Engine of Modern Commerce

This slick, automated communication is what makes modern e-commerce work. Every time you buy a t-shirt, sign up for a subscription box, or hail a ride, a payment API is humming away in the background. It manages the entire transaction from start to finish without anyone needing to lift a finger.

This automation is absolutely crucial for growth. You simply can't scale a business by manually processing thousands of transactions a day. An API ensures that whether you have ten customers or ten million, the payment experience is smooth, secure, and instant.

An API hides the mind-boggling complexity of the global financial system. It neatly bundles everything—fraud checks, currency conversions, multi-bank approvals—into a simple set of instructions that a developer can plug into an app.

Fueling a Growing Digital Economy

The proof is in the numbers. The global market for these payment systems is on a trajectory to hit $15.7 billion by 2033, a clear sign of the unstoppable shift to digital commerce. This isn’t just a passing trend; it's a deep, fundamental change in how we exchange value. For more details on this trend, check out the Online Payment API market report.

When it's all said and done, a good payment API is more than just a piece of code. It's a cornerstone for your business that helps you:

- Build customer trust with a checkout process that feels safe and professional.

- Boost conversion rates by removing friction and making it easy for people to pay you.

- Enable true scalability by putting your financial operations on autopilot.

2. What Are the Different Types of Payment APIs?

When you plug into a payment API, you’re not just connecting to a single service. You're tapping into a whole ecosystem of specialized players, and figuring out who does what can feel a little confusing at first.

Think of it like a restaurant's food delivery system. You have the person who takes the order, the kitchen that prepares the food, and the driver who brings it to the door. Each role is distinct but essential. Payment APIs work in a similar way, with different players handling specific parts of the transaction journey.

Let's break down the main types you'll run into.

Payment Gateways: The Secure Messengers

A payment gateway is like a digital armored truck. Its one job is to securely grab your customer's sensitive payment information from your website or app and deliver it safely to the next stop: the payment processor.

It encrypts the data—the credit card number, expiration date, and CVV—the moment it's entered, making sure it's unreadable to any prying eyes during its journey. The gateway is the front door; it starts the transaction, but it never actually touches the money itself. It's purely a secure messenger service.

- Primary Role: Securely capture and transmit payment data.

- Analogy: The pneumatic tube at a bank drive-thru. It safely transports your check to the teller, but it isn't the bank itself.

Payment Processors: The Financial Back Office

Once the gateway has delivered its package, the payment processor takes over. This is the financial "back office" where the real heavy lifting happens.

The processor communicates with the card networks (like Visa or Mastercard) and the customer’s issuing bank to get the transaction approved or declined. It checks if the customer has enough funds, coordinates the actual money transfer, and makes sure the cash eventually lands in your merchant account. They are the direct link to the complex banking networks that move money around the globe.

A processor is like the air traffic controller for your payments. It juggles communication between the customer's bank and the card networks to guide your money to a safe landing in your account, avoiding any turbulence along the way.

Payment Service Providers (PSPs): The All-in-One Solution

So, what if you don't want to deal with separate gateways and processors? That’s where a Payment Service Provider (PSP) comes in. Think of companies like Stripe or PayPal.

A PSP bundles the gateway, the processor, and often a merchant account into one seamless package. You get a single API that handles the entire transaction from start to finish—from the moment a customer clicks "buy" to the money settling in your bank. This all-in-one approach is why PSPs are so popular, especially for small businesses and startups. They take a complicated, multi-step process and make it feel simple.

Core Features Every Powerful Payment API Should Offer

A great payment API does a lot more than just move money from point A to point B. Think of it less like a simple cash register and more like the central nervous system for your entire revenue operation. Its true value isn't just in processing a payment; it's in all the features that automate tricky financial workflows, give you mission-critical data, and save your team from countless headaches.

We're moving way beyond a basic "pay now" button here. A modern, robust API gives you a whole suite of tools built for how business actually works today. These features manage the entire customer financial journey, from the very first purchase to subscriptions, refunds, and everything in between.

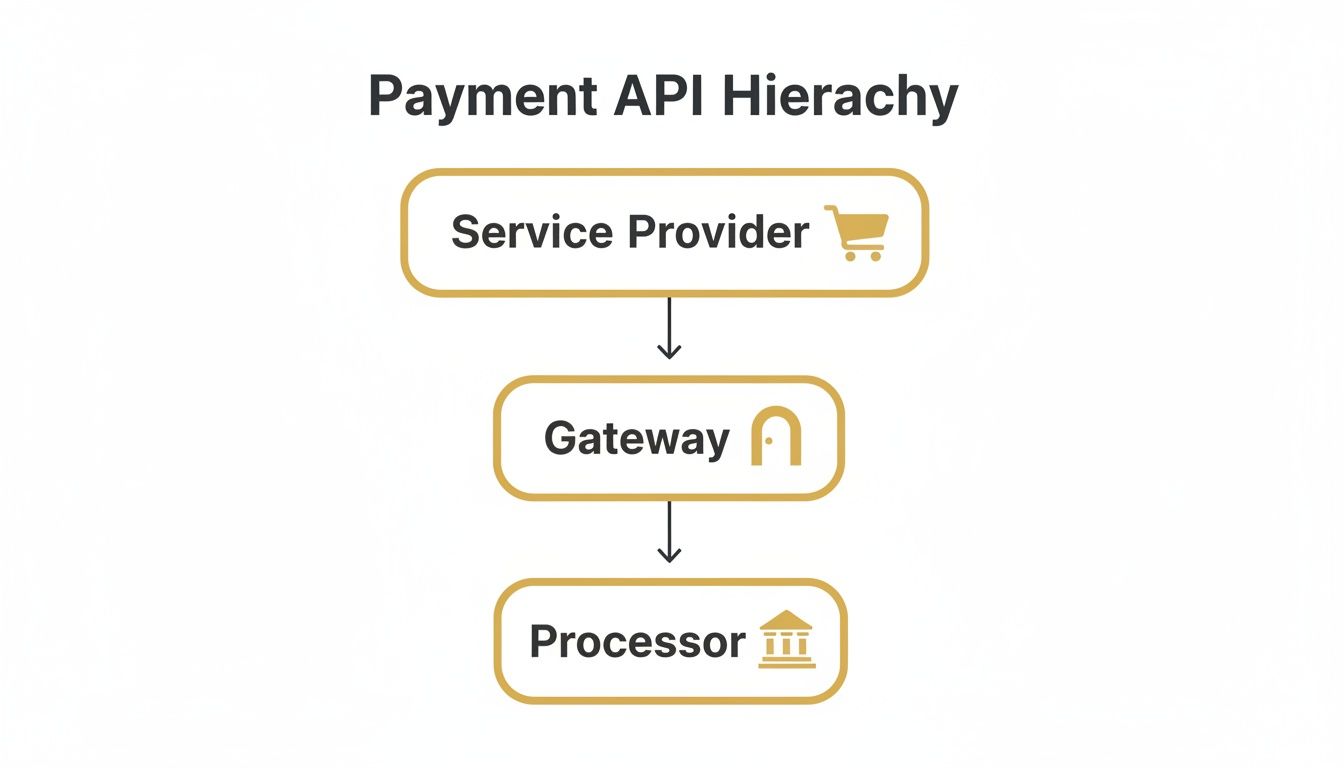

This diagram shows the basic flow of a transaction, from your business down through the layers that make it all happen.

As you can see, the API is your connection to the payment gateway, which then talks to the processor to get the final green light from the bank.

Foundational Payment and Refund Capabilities

First things first, the API has to nail the basics of payment processing. This means flawlessly authorizing a charge on a customer's card and then "capturing" the funds. But what goes in must sometimes come out, and handling that reversal process cleanly is just as critical. A solid API will offer simple endpoints for issuing full or partial refunds tied directly to the original transaction ID.

Imagine an e-commerce store. With a good API, a customer service agent can process a return with a single click in their admin dashboard. That click fires off an API call, and the refund is handled. No more clunky manual bank transfers, and everything is neatly tied to the original order, which keeps your accounting clean and error-free.

Managing Subscriptions with Recurring Billing

For any business running on a subscription model, from SaaS platforms to monthly box services, recurring billing isn't just a feature—it's the engine. A top-tier payment API provides dedicated tools to automate these complex billing cycles.

And this is about so much more than just hitting a credit card on the 1st of every month. A quality API should let you:

- Build flexible billing plans: Set up different pricing tiers, offer free trials, or even implement usage-based billing.

- Handle prorated charges: Automatically calculate the correct amount when a customer upgrades or downgrades in the middle of a billing cycle.

- Automate dunning: Intelligently retry failed payments and send out automated reminders when a customer's card is about to expire.

By automating these subscription management tasks, a payment API saves your engineers from the nightmare of building a custom billing engine from scratch. It takes a massive operational burden and turns it into a smooth, reliable process.

Real-Time Alerts with Webhooks and Events

Finally, the best APIs don't just sit around waiting for you to ask for an update. They tell you when something important happens, right as it happens. This magic is accomplished through webhooks, which are essentially automated, real-time notifications that the API sends to your application's server.

For example, when a customer's recurring payment fails, the payment API can instantly send a webhook to your system. Your application can then immediately kick off a workflow: automatically email the customer, flag their account as "past due," and schedule the payment to be retried in a few days. This kind of proactive communication is absolutely essential for keeping customer churn and revenue loss to a minimum.

How Payment APIs Handle Security and Compliance

When it comes to an api for payments, security isn't just another feature on a checklist—it’s the entire foundation. Every time a customer types in their credit card number, they’re trusting you to keep that information safe. Modern payment APIs are built specifically to shoulder this massive responsibility, taking the complex security work off your plate.

The heart of payment security is the Payment Card Industry Data Security Standard (PCI DSS). This is the non-negotiable rulebook for anyone who touches cardholder data. Trying to become PCI compliant on your own is a notoriously difficult and expensive journey, filled with endless audits and technical hurdles.

Reducing Your PCI Compliance Burden

This is where a good payment API really shines. By integrating with a provider like Stripe or Adyen, you sidestep the most painful parts of PCI compliance. The moment a customer enters their payment details, that information is sent straight from their browser to the provider’s fortified servers, never even touching your own.

Because your systems don't handle or store the raw card number, your PCI scope shrinks dramatically. Instead of facing a massive, expensive audit, you usually just have to fill out a far simpler Self-Assessment Questionnaire (SAQ). That frees up an enormous amount of time and money, letting you get back to building your business.

How Tokenization Protects Customer Data

The magic behind this security hand-off is a technology called tokenization. It’s a bit like giving a valet a special key for your car. That key can start the engine and park the vehicle, but it can’t open the trunk or glove box where your valuables are stored.

A payment token functions in a very similar way. The API grabs the customer's actual credit card number and immediately swaps it for a unique, randomly generated string of characters—that's the token.

This token is what you store and use for future transactions, like recurring subscriptions or one-click checkouts. If a hacker ever breached your system and stole the tokens, they’d be worthless. The actual card details remain securely locked away in your payment provider’s vault.

By taking charge of these critical security protocols, a payment API does more than just protect your customers; it shields your business from massive risk and liability. You can process payments with confidence, knowing you're backed by a robust, compliant infrastructure. To understand more about how data is managed, feel free to review our privacy policy. This deep commitment to security is what helps build lasting trust with your customers.

Choosing the Right Payment API for Your Business

Picking a payment API isn't just a technical task for your dev team—it’s a fundamental business decision that hits your bottom line, customer experience, and your ability to grow. The right choice works quietly in the background, a silent partner in your success. A bad one, on the other hand, can create a nightmare of lost sales, frustrated developers, and operational headaches.

So, how do you make the right call? It's about looking past the shiny transaction fees and really digging into how an API will hold up under the unique pressures of your business. You need a clear framework for evaluating its features, its reliability, and the quality of support you'll get when things inevitably go wrong.

Evaluate Global and Local Payment Methods

If you have any ambition to sell beyond your home country, your payment API needs to speak the local financial language. Simply accepting major credit cards won't cut it anymore. Customers around the world expect to use their preferred payment methods, whether that's iDEAL in the Netherlands, SEPA across Europe, or Pix in Brazil.

A top-tier API gives you a whole menu of payment options right out of the box. Prioritizing one that supports these local methods is a must for international growth. It builds trust, cuts down on checkout friction, and can give your conversion rates a serious boost in new markets. Trying to expand without this is like opening a shop abroad but refusing to take the local currency.

This all ties into a broader strategy known as payment orchestration, which lets you manage multiple payment providers through a single integration. Industry leaders are pointing to this as a major trend, highlighting its power to boost efficiency and adapt to regional preferences. For a deeper look, explore the 2026 Commerce and Payment Trends Report from Global Payments.

Scrutinize Developer Experience and Reliability

Believe me, your development team will be the first to know if you've chosen a poorly designed API. Before you sign any contracts, have them take a hard look at the provider's documentation. Is it clear, thorough, and packed with real-world code examples? Great documentation can save you hundreds of hours of developer pain during both the initial setup and ongoing maintenance.

Just as critical is the API's uptime—its reliability. If the API is down, you can't take payments. It’s that simple. For a busy online store, even a few minutes of downtime can mean thousands of dollars in lost sales. Look for providers who are transparent about their historical uptime and offer a solid Service Level Agreement (SLA).

A payment API is a utility, just like electricity. It needs to be consistently available, reliable, and something you rarely have to think about. When it goes down, everything stops.

Finally, think about the bigger picture. A strong payment solution is a key piece of your overall strategy for great ecommerce and customer service. Your API doesn't live in a vacuum; its ability to connect with your other business systems is what creates a truly seamless journey for your customers. When you’re ready to take the next step, you can review different pricing options that fit your business needs.

Integrating Your API with Proactive Chargeback Management

Your payment API is a fantastic tool for getting paid, but it doesn't do much to protect you when that money is at risk of being clawed back. This is where a second, vital API integration enters the picture. While your payment API manages the initial transaction, a proactive chargeback management system connects to your processor to defend your revenue after the sale.

Think of it this way: your payment API is the front door that lets customers and their money in. A chargeback alert platform, like Disputely, acts as the security system that prevents that same money from being unexpectedly yanked back out. It works by catching disputes the moment they start, well before they escalate into official chargebacks.

A Critical Window of Opportunity

This integration opens up a crucial 24-72 hour window that can completely change how you deal with customer disputes. The second a customer contacts their bank to question a charge, the alert system's API gets a heads-up directly from the card networks, like Visa and Mastercard.

This real-time notification gives you a chance to step in. Instead of getting hit with a formal chargeback weeks down the line with no warning, you can immediately refund the customer. This simple act of goodwill often resolves the issue on the spot, satisfying the bank and stopping the dispute from ever becoming a damaging chargeback on your record.

Integrating a chargeback alert API is like getting a smoke detector for your revenue. Instead of dealing with the aftermath of a fire (a chargeback), you get an early warning that lets you resolve the issue before any real damage is done.

This proactive strategy is a game-changer for businesses, especially those handling a lot of transactions. It isn't just about saving the money from a single dispute; it's about protecting your entire payment processing relationship. By heading off chargebacks before they happen, you can:

- Reduce chargebacks by up to 99%, protecting your bottom line.

- Avoid being placed in high-risk monitoring programs by Visa and Mastercard.

- Keep your payment processor happy, preventing them from freezing your account or dropping you altogether.

By pairing your payment API with a chargeback alert API, you build a complete system that doesn't just process payments effectively but also secures your revenue for the long run. If you’re already dealing with disputes, our guide on chargeback representment can show you how to fight back against invalid claims.

Frequently Asked Questions About Payment APIs

Diving into payment APIs often brings up a few practical questions once you start connecting the dots between theory and your actual checkout page. Let's tackle some of the most common ones that pop up.

What Is the Difference Between a Payment API and a Payment Gateway?

It's helpful to think of the relationship like this: a payment gateway is the digital equivalent of a secure armored truck. Its job is to safely carry sensitive credit card data from your customer to the bank.

The API for payments is the set of instructions you give the truck driver. It's the language you use to tell the gateway, "Hey, pick up this payment information and take it to this specific destination for approval."

So, you can't really have one without the other. The API is the communication layer—the how—that allows your app to speak to the gateway.

Do I Need to Be PCI Compliant if I Use a Payment API?

This is a huge one. Using a modern payment API from a provider like Stripe or Braintree massively simplifies your PCI compliance obligations. Why? Because their APIs are designed so that the sensitive cardholder data never even touches your servers. It goes directly from the customer's browser to their ultra-secure environment.

But—and this is important—it doesn't completely absolve you of responsibility. You still have a part to play. You'll typically need to fill out a Self-Assessment Questionnaire (SAQ) to confirm you're following best practices on your end. It’s a far cry from a full, painful PCI audit, but it’s not nothing.

Your payment provider does the heavy lifting for PCI compliance, but you're still their partner in keeping the transaction environment secure. The API makes your job infinitely easier, but it doesn't eliminate it.

Can I Use Multiple Payment APIs at the Same Time?

Absolutely. In fact, many larger businesses do just that. This strategy is often called payment orchestration, and it involves using a central system to intelligently route transactions to different payment providers based on a set of rules.

It might sound complex, but the reasons for doing it are pretty compelling:

- Cost Savings: You can send a transaction to whichever provider offers the best rate for that specific card type or country.

- Better Uptime: If one of your payment gateways goes down (and it happens), you can automatically failover to a backup. No more lost sales during an outage.

- Higher Approval Rates: Some processors just perform better in certain regions. Orchestration lets you route international payments to the processor with the best chance of success.

While it adds a layer of technical work upfront, the payoff in cost savings and reliability can be a game-changer for businesses processing a high volume of transactions.

Ready to stop chargebacks before they start? Disputely integrates directly with your payment processor to alert you to disputes in real-time, giving you the power to refund and prevent damaging chargebacks. Protect your revenue and merchant accounts by visiting https://www.disputely.com to learn more.