Your Guide to Card on File Payments for Modern Merchants

When you hear the term "card on file" (CoF), what comes to mind? It’s the magic behind one-click checkouts, effortless subscription renewals, and your Uber ride starting without you ever pulling out a wallet.

Simply put, a card on file is when a customer gives you permission to store their payment details securely for future transactions. It’s the foundation of a trusted, frictionless relationship with your repeat buyers.

Why Card on File Is the Engine of Modern Commerce

Think of CoF as a secure digital valet for your customer's payment info. Instead of forcing them to manually punch in their 16-digit card number, CVC, and expiration date every single time, this technology handles it for them. It might seem like a small thing, but that convenience is what the modern, on-demand economy is built on.

For subscription companies, this is the entire ballgame—it’s what keeps predictable, recurring revenue flowing. For direct-to-consumer (DTC) brands, it’s a killer tool for driving repeat purchases and building loyalty. By making checkout so much faster, card on file is a proven way to reduce cart abandonment.

The Foundation of Customer Convenience

At its core, a card on file strategy is all about removing friction. When a customer trusts you with their details, they're far more likely to complete an impulse buy or stick with a subscription month after month. That convenience has a direct line to higher customer lifetime value (LTV).

The market data tells the same story. The global card payment market is on track to hit USD 1,230.5 billion by the end of 2025, a massive leap from USD 910.138 billion in 2021. So much of that growth is fueled by e-commerce and subscription models that simply couldn't exist without CoF technology.

A well-managed card on file system isn't just a payment method; it's a customer relationship tool. It signals to your customers that you value their time and are committed to providing a seamless, trustworthy experience.

Benefits for Merchants and Customers Alike

Implementing a card on file system creates a powerful win-win, offering clear advantages for both your business and your customers.

Let's break down how each side benefits from this simple but effective setup.

Key Benefits of Card on File for Merchants and Customers

| Benefit | Impact on Merchants | Impact on Customers |

|---|---|---|

| Increased Revenue | Drives higher lifetime value and encourages impulse buys through frictionless checkout. | Easy to make repeat purchases without the hassle of re-entering payment info. |

| Predictable Cash Flow | Ensures reliable, automated billing for subscriptions and recurring services. | Guarantees uninterrupted service and avoids manual monthly payments. |

| Operational Efficiency | Reduces the administrative burden of chasing failed payments and streamlines accounting. | Enjoy a "set it and forget it" experience for recurring bills and subscriptions. |

| Enhanced Loyalty | Builds trust and makes it more convenient for customers to stick with your brand. | Feels like a valued, recognized customer with a personalized checkout process. |

Ultimately, a smart card on file strategy is no longer just a "nice-to-have"—it's an essential part of any business aiming for real, sustainable growth. It’s the starting point for building a loyal customer base. In the sections ahead, we’ll dive into the technical mechanics, security protocols, and dispute prevention tactics you need to master.

The Technology That Makes Card on File Secure

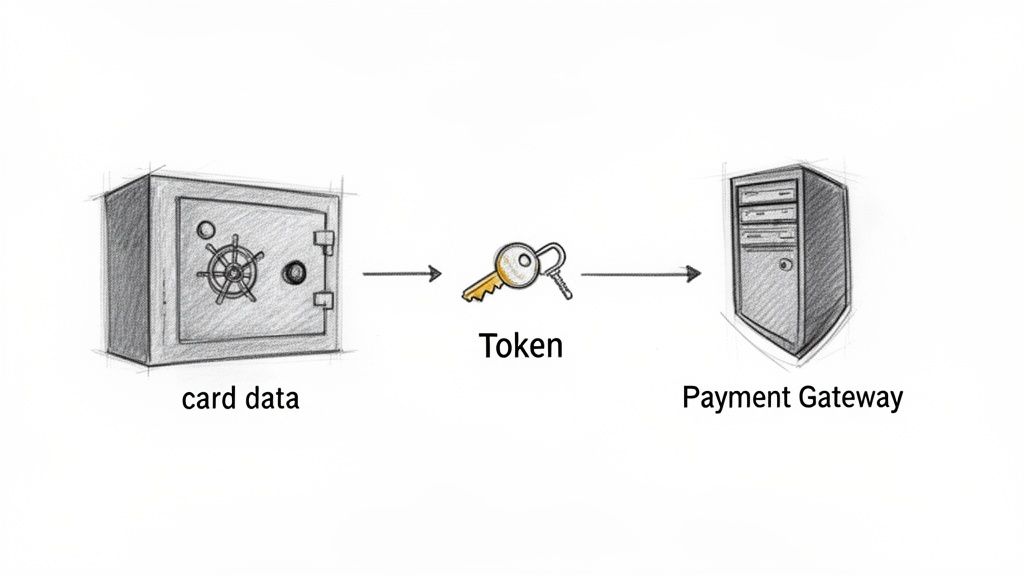

When a customer trusts you with their payment details, it’s a huge responsibility. So, how do you store their information for future use without turning your servers into a goldmine for hackers? The answer lies in a clever process that swaps real card numbers for secure, stand-in values.

This is the tech that makes card on file systems both seamless for the customer and safe for you. You get the convenience of recurring billing and one-click checkouts without the massive headache and risk of storing raw credit card data.

Let’s pull back the curtain and see how it all works.

The Magic of Payment Tokenization

Think of your customer's 16-digit credit card number as the master key to their bank account. You definitely wouldn't want to keep a copy of that key stashed in your desk drawer. What you'd want is a special, single-purpose key that only opens the lock for your business.

That’s exactly what payment tokenization accomplishes.

When a customer enters their card details for the first time, your payment gateway intercepts that sensitive info and immediately locks it away in its own highly secure, PCI-compliant vault. In its place, the gateway creates a unique, non-sensitive string of characters called a token.

This token is what you actually store on your servers. It’s essentially just a reference number—a placeholder that points to the real card without containing any of the valuable data itself.

Key Takeaway: A token is completely useless to a fraudster. If a data breach ever happened, hackers would only find a pile of meaningless tokens, not actual credit card numbers they could use. This dramatically reduces your security burden.

This entire process ensures that you never have to "touch" or store the customer's primary account number (PAN). From that point on, you initiate all future charges using the token, and your payment gateway handles the rest.

Understanding PCI DSS Compliance

Any business that accepts credit cards has to play by the rules of the Payment Card Industry Data Security Standard (PCI DSS). This is a strict set of security protocols designed to protect cardholder data from theft and fraud.

Let’s be honest: achieving and maintaining PCI compliance on your own is a nightmare. It’s complex, expensive, and involves everything from network security scans to physical access controls.

This is where tokenization becomes a merchant’s best friend. By using a PCI-compliant payment gateway to handle tokenization, you’re effectively outsourcing the hardest parts of compliance. Your PCI scope—the parts of your business subject to these rigid rules—shrinks dramatically because you're not the one storing the sensitive data.

You can learn more about how gateways fit into this process by exploring what's involved when you set up a Stripe account.

Why Transaction Indicators Matter

Behind the scenes of every card on file transaction, special data flags are sent to the customer’s bank. These are known as Cardholder-Initiated Transactions (CIT) and Merchant-Initiated Transactions (MIT), and they play a massive role in whether a payment gets approved or declined.

Here’s the simple difference:

- Cardholder-Initiated Transaction (CIT): This is the first transaction, when the customer is physically present (digitally speaking) and actively enters their card info. Think of them signing up for a subscription and checking the "Save my card" box.

- Merchant-Initiated Transaction (MIT): These are all the follow-up payments you charge to the stored card without the customer being there. A monthly subscription renewal is a perfect example.

These little flags are absolutely critical. They give the issuing bank context. An MIT flag essentially says, "Hey, don't be alarmed. This charge is part of an ongoing agreement the cardholder already approved." This small piece of information helps the bank distinguish legitimate recurring payments from potentially fraudulent ones, significantly reducing false declines.

Without these indicators, your recurring charges would look suspicious, leading to a spike in failed transactions and frustrated customers.

How to Manage Your Card-on-File System Like a Pro

A stored card isn't something you can just set and forget. To get the most out of it, you need a proactive plan to keep the information valuable, stay compliant, and make sure your customers are happy. Think of it as a living database that needs regular care to prevent lost sales and maintain customer trust.

Building a solid strategy goes way beyond just storing a token securely. It's about creating a transparent and easy experience for your customer throughout the entire time their card is on file, from the moment they agree to save it until the day it inevitably expires.

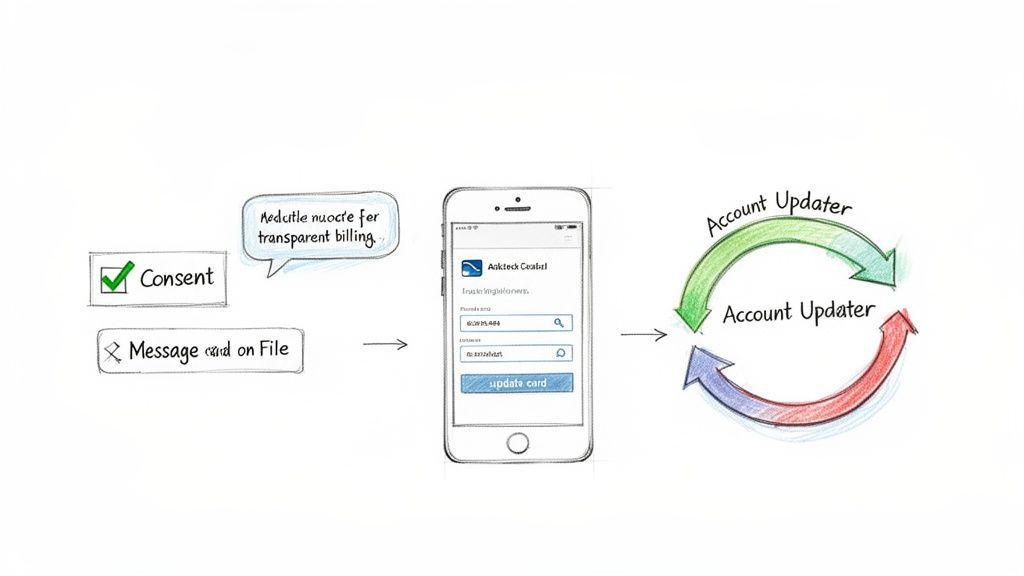

Nail the Consent and Communication

The bedrock of any good card-on-file relationship is crystal-clear consent. Customers need to know exactly what they're signing up for when they save their card. This isn't just about ticking a legal box; it's a foundational moment for building trust that will pay you back in spades through customer loyalty.

Your checkout or signup flow has to be completely unambiguous. Stay away from pre-checked boxes or confusing jargon. Just state plainly that you're saving their card for future purchases or for a recurring subscription.

Just as important is what happens after they've signed up. Nobody likes a surprise charge. Here are a few must-dos:

- Send Pre-Billing Notifications: A quick email a few days before a recurring charge hits is a game-changer. It reminds the customer about the payment and gives them a heads-up to update their card if needed.

- Use Clear Billing Descriptors: Make sure the name that shows up on their credit card statement is instantly recognizable. A cryptic descriptor like "SP*XYZ-SERVICES" is a one-way ticket to a chargeback.

- Provide Easy-to-Access Receipts: Fire off a detailed receipt by email immediately after every successful transaction.

Make Self-Service a Breeze

Customers need to feel like they're in the driver's seat with their payment info. If you bury the "manage my card" page deep in your website, you're just asking for frustrated customers who might file a chargeback simply because they can't figure out how to cancel. Make it ridiculously easy for them to update their card details.

A frictionless self-service portal is a powerful retention tool. When a customer can update their expired card in seconds, you prevent the passive churn that erodes subscription revenue. It turns a potential cancellation point into a simple, positive interaction.

Your customer account dashboard should have a prominent section where users can:

- View the current card on file (only showing the last four digits, of course).

- Add a new primary payment method.

- Delete old or unused cards.

This level of transparency builds confidence and cuts down on the number of support tickets your team has to handle. For any questions that do come up, make sure you offer clear instructions and responsive help. You can find more tips on creating a fantastic customer experience in our support guide.

Automate Card Updates to Stop Churn in its Tracks

Let's face it: cards expire. They get lost, stolen, and reissued all the time. If your entire strategy relies on customers remembering to update this information manually, you're guaranteed to lose revenue. This is exactly where an Account Updater service becomes a non-negotiable tool.

An Account Updater is an automated service, usually offered by your payment gateway, that talks directly with card networks like Visa and Mastercard. It proactively scans your stored cards to check for any changes.

When a customer gets a new card with a new number or expiration date, the service automatically updates the tokenized record in your system. This all happens seamlessly behind the scenes, ensuring recurring payments go through without a hitch. Putting this on autopilot can recover up to 20% of revenue that would otherwise disappear due to involuntary churn from failed payments. It’s one of the highest-impact, lowest-effort ways to protect your recurring revenue.

How Your "Card on File" System Can Accidentally Invite Chargebacks

There’s no denying it: keeping a customer’s card on file is fantastic for smooth, predictable revenue. It’s the engine behind every successful subscription business. But here’s the catch—that same convenience can quietly open the floodgates to a higher risk of chargebacks.

The very automation that makes recurring billing so powerful is also its biggest vulnerability. When charges happen without the customer having to pull out their wallet each time, it creates a unique set of problems. A happy subscriber one day can turn into a costly dispute the next, often without any ill intent.

Why Do Recurring Payments Get So Many Disputes?

Think about it from the customer's perspective. The friction you work so hard to remove during checkout can easily resurface months later as pure confusion. Someone who eagerly signed up for your service might completely forget about it. When that charge pops up on their bank statement, their first reaction isn't to track down your support email—it's to call their bank and say, "I don't recognize this."

This leads to a few classic chargeback scenarios that are all too common in the card-on-file world:

- The Forgotten Trial: A customer signs up for a free trial, forgets to cancel, and disputes the very first real charge. This is probably the number one headache for subscription merchants.

- The Mystery Charge: If your company name is “Awesome Products Inc.” but your billing descriptor shows up as “API*SALES-TX,” you’re practically inviting a dispute. Customers don’t recognize it and assume it’s fraud.

- The Family Purchase: A spouse or kid uses the saved card to buy something or sign up for a service. When the main cardholder reviews their statement, they see a charge they personally didn't make and immediately flag it.

These situations often result in something called friendly fraud. It’s not a malicious attack; it’s a legitimate customer disputing a legitimate charge because of a simple misunderstanding.

Friendly fraud feels anything but friendly. The customer isn't trying to steal from you, but the outcome is the same: you lose the revenue, get hit with a hefty fee, and take a hit to your merchant account's health.

This Isn't a Small Problem—It's a Massive One

The risk has gotten bigger simply because more people are paying with cards for everything. We hit a major tipping point in 2026, when for the first time ever, card credentials were used for half of all global consumer payments. From a morning latte to a monthly SaaS subscription, cards are the default. You can see more on these trends in Visa's 2026 predictions and insights.

What does that mean for you? It means the number of stored cards has exploded. For every merchant using a card-on-file model, the potential for disputes has grown right alongside it. More stored cards simply create more opportunities for forgotten subscriptions and unrecognized charges, making a solid chargeback defense non-negotiable.

The Real Cost of a Card-on-File Chargeback

A chargeback is so much more than just giving a refund. Each one sets off a chain reaction of costs and headaches that can seriously stunt your business's growth.

Let’s break down the true damage of a single dispute:

- Lost Revenue: The original sale amount is gone. Poof.

- Punitive Fees: Your processor slaps you with a non-refundable chargeback fee, usually somewhere between $20 and $100.

- Wasted Time: Your team has to drop what they're doing to dig up evidence and fight the dispute, which is time they could have spent on growing the business.

- Processor Problems: A high dispute rate makes you look risky to your payment processor. This can lead to them holding your funds, charging you higher fees, or even shutting down your account entirely.

This is the central challenge every recurring revenue business has to solve. The card on file system that fuels your growth also creates the perfect environment for disputes that slowly drain your profits. The answer isn't to get rid of this powerful model, but to build a system that gets out in front of these problems before they turn into expensive chargebacks.

How Chargeback Alerts Prevent CoF Disputes

Dealing with a wave of chargebacks from your card-on-file customers can feel like an impossible game of whack-a-mole. For every dispute you fight, another one pops up. The good news? You don't have to wait for the damage to hit your bottom line. You can get ahead of these disputes with a proactive early warning system.

Instead of just reacting after a chargeback has already stained your record, you can intercept a customer's complaint the moment it starts. This is all possible thanks to alert networks built by the major card brands themselves, giving merchants a critical window of opportunity to make things right.

The Power of an Early Warning System

Think of a chargeback alert as a smoke detector for your merchant account. It picks up on the very first sign of trouble—a customer calling their bank to question a charge—and sounds the alarm before it erupts into a full-blown fire (a costly chargeback).

Two of the most important networks are Visa's Rapid Dispute Resolution (RDR) and Mastercard's CDRN. When a cardholder initiates a dispute with their bank, these networks send a real-time notification to integrated platforms like Disputely.

This alert gives you a brief but priceless timeframe—usually just 24 to 72 hours—to resolve the issue directly by issuing a refund. If you do, the dispute is stopped dead in its tracks. It never becomes a formal, damaging chargeback.

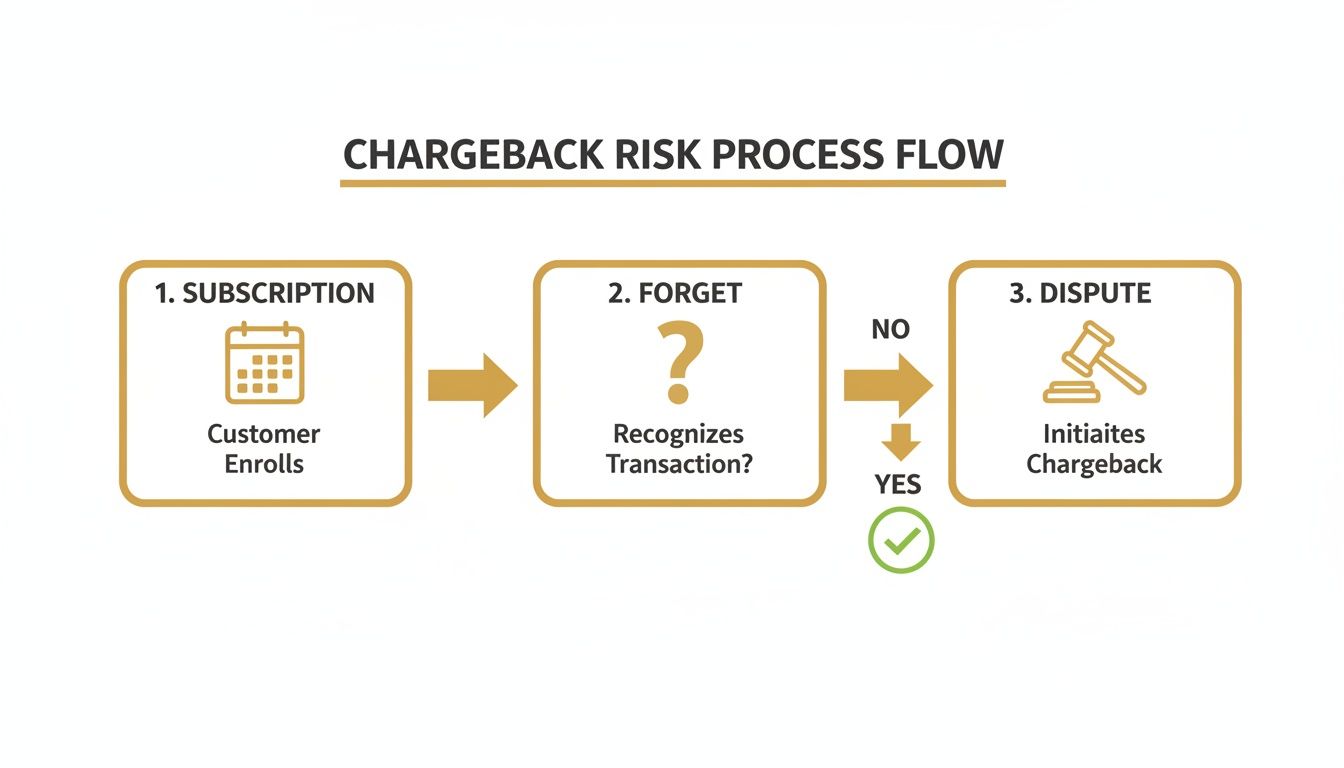

The flowchart below shows just how easily a simple recurring payment can turn into a messy dispute, highlighting where communication breaks down.

As you can see, a forgotten subscription is one of the most common paths to a dispute. This is exactly why you need a system that can step in before that complaint becomes official.

Automating Your Defense

Let's be realistic: that 24-hour window is far too short to handle manually, especially if you're processing a high volume of transactions. This is where automation isn't just a nice-to-have; it's a necessity. An intelligent alert platform can be set up with rules to automatically handle incoming alerts based on your business logic.

For example, you could set rules to:

- Automatically refund any dispute under a certain amount, like $25.

- Always refund disputes from first-time customers to save a new relationship.

- Flag high-value disputes for your team to review, giving you the choice to refund or prepare to fight.

This kind of automated approach means you never miss that short window to prevent a chargeback. The system works around the clock to protect your accounts, turning a potential crisis into a simple, automated refund. By proactively resolving the issue, you dodge hefty fees, protect your critical dispute ratio, and keep your payment processors happy. To learn more, check out these chargeback representment strategies for different scenarios.

By converting a brewing chargeback into a simple refund, you not only avoid the $20-$100 fee but also safeguard your merchant account's standing. It’s the single most effective way to manage the inherent risks of a card-on-file business model.

Staying Ahead in a Changing Payment World

The payments world is always in motion, with new technologies creating both opportunities and headaches. Take virtual cards, for instance. This market is exploding, projected to hit USD 129.19 billion by 2032 with an impressive 18.3% annual growth rate.

While these cards boost security, they also add another layer of complexity for businesses that rely on card-on-file billing. This trend just reinforces the need for a fast, automated dispute resolution process that can adapt to whatever payment method your customers prefer. Chargeback alerts provide that critical, real-time layer of defense.

Common Questions About Card on File

You've got the basics down, but when you're in the trenches managing customer payments, specific questions always pop up. It's one thing to understand the theory, and another to apply it when revenue is on the line. Let's tackle some of the most common questions merchants ask about using card on file.

Think of this as your go-to reference for handling those tricky legal, technical, and strategic gray areas with confidence.

Is It Safe and Legal to Store Customer Card Information?

Yes, but with a huge caveat: you can only do it the right way. That way is called tokenization. Storing raw, unencrypted credit card numbers yourself—whether on a server or in a spreadsheet—is not just unsafe, it's a direct violation of PCI DSS rules. Don't even think about it.

Here’s how it works in practice: a compliant payment gateway (like Stripe or Braintree) acts like a secure vault for you. When a customer enters their card details, the gateway snatches them, locks them away, and hands you back a "token"—a unique, meaningless string of characters. You store that token. If a hacker ever breaches your system, all they get is a pile of useless tokens.

By using tokenization, you're essentially offloading the massive security and compliance headache to a company built to handle it. Just remember, you still need to get clear, explicit consent from the customer to store their card for future use. The card networks demand it.

This is how you get all the benefits of recurring billing and one-click checkouts without taking on the immense risk of guarding raw payment data.

How Do I Handle Expired Cards for Subscription Customers?

Expired cards are the silent killer of subscription revenue. If you're not proactive, you'll see customers churn without even realizing it. The best tool for this job is an Account Updater service, which your payment gateway should offer.

This service is a lifesaver. It automatically pings the card networks (Visa, Mastercard, etc.) behind the scenes to check if your customers' stored card details have changed. If a card has a new expiration date or a whole new number, the service updates your records instantly.

The beauty of this is that the customer’s recurring payments just keep working. No interruption, no failed payment email, no action required on their part. For any cards the updater can't fix, a smart dunning process is your fallback plan.

- Automated Emails: Set up a friendly email sequence that starts before the card expires, gently reminding the customer to update their info.

- In-App Notifications: If they log into their account, show a clear, simple banner asking them to update their payment method.

- Secure Update Page: Make it dead simple. Give them a secure link that takes them directly to a page where they can pop in the new details in a few clicks.

What Is the Difference Between a Refund and a Chargeback?

This is a critical distinction. While both involve money going back to the customer, they are worlds apart in their impact on your business.

A refund is a conversation between you and your customer. You agree to return their money to resolve an issue. It’s a normal cost of doing business, and while you lose the sale, the damage stops there.

A chargeback, on the other hand, is a forced reversal initiated by the customer's bank. When a cardholder disputes a charge, the bank yanks the money from your account. This isn't a conversation; it's a penalty.

Here’s why chargebacks are so toxic for merchants:

- Hefty Fees: You get slapped with a non-refundable fee, usually between $20 and $100, for every single dispute—win or lose.

- Reputation Damage: A high chargeback rate flags your business as risky to payment processors. This can lead to higher processing fees or even getting your merchant account shut down.

- Wasted Resources: Your team has to drop everything to gather evidence and fight the dispute, a time-consuming battle that merchants often lose.

This is exactly where chargeback alerts come in. They give you a heads-up, letting you turn a potential chargeback back into a simple refund by resolving the issue directly with the customer.

Can I Still Fight a Dispute If I Use Chargeback Alerts?

Absolutely. Using a chargeback alert platform doesn't mean you're waving a white flag and refunding every claim that comes your way. A good system puts you in the driver's seat.

You can set up rules that fit your business. For instance, you might decide to automatically refund any dispute under $30, or maybe any claim from a first-time customer. It's often not worth the fight, and it keeps your chargeback ratio clean.

But what about a high-value order where you have ironclad proof of delivery and customer interaction? For that, you can choose not to refund the alert. The dispute will then proceed to a formal chargeback, and you can come out swinging with your evidence in the representment process. This flexibility is key—it lets you avoid unnecessary refunds for disputes you know you can win.

Protecting your revenue from the risks of a card-on-file model requires a proactive defense. With Disputely, you can stop up to 99% of chargebacks before they happen by resolving customer disputes in real-time. Learn how Disputely can safeguard your merchant account and save you thousands in fees.