A Merchant's Guide to Winning Cash App Chargebacks

It's a common and dangerous myth: peer-to-peer payment apps like Cash App are supposedly a chargeback-free zone. The reality? That couldn't be further from the truth.

Any Cash App payment funded by a customer's credit or debit card can be disputed right at the source—their bank. This creates a hidden doorway for traditional chargebacks, leaving unsuspecting merchants exposed to serious financial risk.

The Hidden Threat of Cash App Chargebacks for Merchants

For many businesses, accepting Cash App feels like a smart, modern move. It’s fast, popular, and seems to offer direct, final transactions. But that’s a dangerously simple view of how it all works. A critical blind spot exists that can lead to lost revenue, surprise fees, and even account termination.

The vulnerability isn't with Cash App itself, but with how customers fund their payments. If a customer pays you from their existing Cash App balance, the transaction is pretty much set in stone. The game changes completely, however, when they use a linked credit or debit card to complete the purchase. The moment they do that, the entire transaction is governed by the rules of card networks like Visa and Mastercard.

A Back Door for Traditional Disputes

Think of your payment options like doors to your store. Payments from a Cash App balance are like customers walking through the front door—secure and straightforward. But card-funded payments are like an unlocked back door.

Through this "back door," a customer can completely bypass Cash App, go straight to their bank, and file a dispute for all the usual reasons—unauthorized transaction, product not as described, you name it.

The dispute doesn't even touch Cash App's system. It travels from the customer’s bank, through the card network, and lands squarely with your payment processor, whether that’s Stripe or Shopify Payments. All of a sudden, you're hit with a formal chargeback from a payment you thought was safe.

This is the fundamental risk businesses face. A Cash App chargeback carries the exact same weight as any other card dispute, directly damaging your merchant account health and your bottom line.

The Ripple Effect of Unseen Chargebacks

The consequences of these "hidden" chargebacks are no joke and can quickly snowball. Each dispute triggers a chain reaction of negative impacts that extend far beyond just losing the sale.

Here’s a breakdown of what’s at stake:

- Lost Revenue: The disputed amount is immediately yanked from your account.

- Chargeback Fees: Your processor slams you with a non-refundable fee, usually between $15 and $100 per dispute.

- Monitoring Programs: Too many disputes can land you in costly card network monitoring programs, which come with thousands in monthly fines.

- Account Termination: The worst-case scenario? Your processor freezes your funds or shuts down your merchant account entirely, paralyzing your business.

Recognizing this threat is the first step. You can no longer afford to be reactive. In today's interconnected payment world, proactive dispute management is essential for survival. This guide will walk you through exactly how to protect your business.

How a Cash App Chargeback Really Works

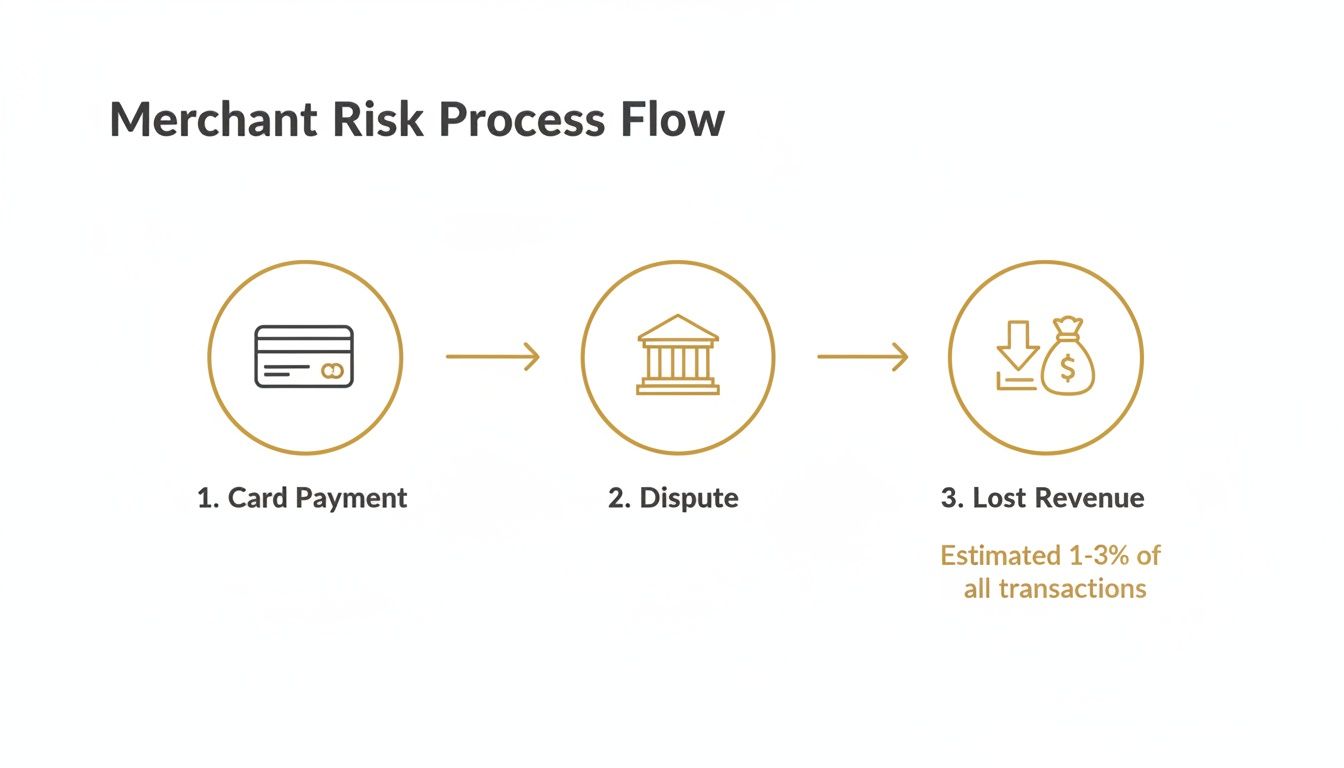

If you're going to manage a Cash App chargeback, you first need to understand its journey. It’s not just a simple button-click inside the app. It's often a complex chain reaction involving multiple banks that can leave you completely in the dark until it’s far too late.

Many businesses make the critical mistake of thinking an in-app refund request is the same as a formal chargeback. It’s not. A customer asking for money back through the app is a customer service conversation; a chargeback is a forced reversal kicked off by their bank, and it comes with much bigger headaches.

Refund Request vs. Bank Chargeback

Think of an in-app refund as a direct chat between you and the customer. It's your chance to fix a problem before things get out of hand. A bank-initiated chargeback, on the other hand, completely removes you from that conversation. The customer's bank takes over as the judge, and you're instantly playing defense.

This flowchart shows just how quickly a simple card-funded payment can go sideways, bypassing you entirely and heading straight toward lost revenue.

As you can see, what starts as a routine sale can morph into a costly dispute without you even getting a heads-up.

To make this crystal clear, let's break down the key differences between a customer asking for a refund within the app versus going to their bank for a chargeback.

Cash App Refund vs Bank Chargeback A Quick Comparison

| Attribute | In-App Refund Request | Bank-Initiated Chargeback |

|---|---|---|

| Who Initiates? | The customer, directly through Cash App. | The customer, by contacting their card-issuing bank. |

| Your Role | You communicate directly and decide to approve or deny the refund. | You're notified after the fact and must defend the sale with evidence. |

| Financial Impact | You lose the sale amount if you issue the refund. | You lose the sale amount plus a separate chargeback fee ($15–$100). |

| Consequences | A simple customer service interaction. | Negative impact on your merchant account health and standing. |

Essentially, one is a conversation, and the other is a formal, bank-led lawsuit in miniature. Knowing the difference is the first step in protecting your business.

The Chargeback Lifecycle, Unpacked

When a customer disputes a payment they made through Cash App using their debit or credit card, they aren't complaining to Cash App—they're calling their bank. This single phone call triggers a formal process governed by rigid card network rules (think Visa or Mastercard), not Cash App's policies. To really get a handle on this, it helps to understand the basics of integrating payment gateways and how they connect all these players.

Here’s how a typical dispute unfolds:

- The Customer Kicks It Off: The cardholder calls their bank (like Chase or Bank of America) and claims a charge was unauthorized, fraudulent, or the goods never arrived.

- The Bank Investigates: The issuing bank gives the claim a quick review. If it looks plausible, they file a formal chargeback through the card network.

- The Network Relays the Message: The card network routes the chargeback down the chain to your payment processor (like Stripe or Shopify Payments). This is usually the very first time you hear about any trouble.

- The Money Is Pulled: Your processor immediately yanks the disputed amount from your merchant account, along with a non-refundable chargeback fee.

The whole messy process can drag on for weeks, with the typical resolution timeline ranging from 45 to 90 days. All the while, those funds are frozen, creating a hole in your cash flow.

The core problem for merchants is the information gap. You are the last to know about a dispute that directly concerns your business, leaving you with little time to react effectively.

This is the hidden danger for any merchant who assumes P2P apps are a safe haven. As soon as a payment is funded by a card, the customer gains the power to go around Cash App's systems and file a chargeback with their bank. This loophole exposes you to the exact same risks as any traditional card-not-present transaction, complete with all the fees and administrative burdens.

Don't just take my word for it. A CFPB action against Block, Inc., revealed Cash App's dispute 'win rate' was a startlingly low 25-36% between 2019-2022, proving just how tough it is for merchants to win these fights.

Because you're blindsided by a long, complicated process, trying to fight chargebacks after they’ve already hit your account is an uphill battle. By the time you get the notification, the momentum is squarely against you. This reality makes it painfully clear: you need a proactive strategy to stop these disputes before they ever get started.

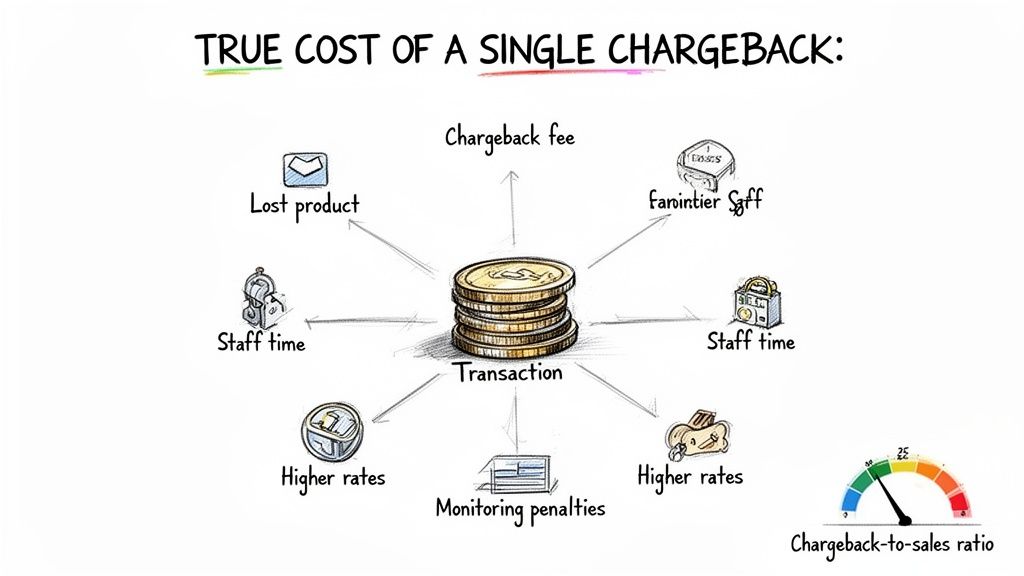

Calculating the True Cost of a Single Dispute

When a Cash App chargeback hits your account, it’s tempting to just look at the initial dollar amount you've lost. A customer disputes a $50 sale, so you think, "Okay, I'm out $50." But that’s a dangerous oversimplification. In reality, that initial loss is just the tip of a very expensive iceberg.

Think of it like an unexpected car repair. The mechanic might quote you for one part, but pretty soon you're also paying for labor, shop fees, and a handful of other "while we're in there" fixes. A chargeback works the same way. It piles on hidden costs that create a nasty financial ripple effect across your business.

The Anatomy of Chargeback Costs

To really get a handle on the damage, you have to break down every single component. The cost isn't one big hit; it's a series of smaller financial blows that silently eat away at your profit margins.

Here’s a look at what you’re actually paying for:

- Lost Product or Service Revenue: This is the most obvious one. The money from the sale is gone. But you’ve also lost the physical product you shipped or the valuable time you spent providing a service.

- Non-Refundable Chargeback Fee: Your payment processor hits you with a fee for every single dispute filed against you. This usually runs anywhere from $15 to $100, and you have to pay it whether you win the fight or not.

- Operational Costs: Time is money, right? Your team has to drop what they're doing to dig up evidence, write a compelling rebuttal, and navigate the whole dispute process. That lost productivity is a very real, very tangible cost.

The damage goes far beyond the immediate transaction. To properly manage these kinds of financial drains and protect your bottom line, many businesses find that dedicated CFO services for small business can be crucial for creating strategies to prevent this kind of profit erosion.

The Chargeback Ratio Threat

But the hidden costs don't even stop there. Card networks like Visa and Mastercard are always watching your chargeback-to-sales ratio. This is a critical health metric for your business, comparing the number of disputes you get to your total number of sales. If that ratio climbs too high, you’re in for a world of hurt.

Think of this ratio as your reputation score with the card networks. If you cross their thresholds—which can be as low as 0.9% of your total transactions—they’ll label your business as high-risk, and the consequences are severe.

Once you’re flagged, you can be forced into a costly monitoring program. These programs come with steep monthly fines and much closer scrutiny of your business, making it tougher to operate. In a worst-case scenario, your payment processor could freeze your funds or just shut down your merchant account entirely, bringing your sales to a screeching halt.

With chargebacks on the rise globally, merchants using Cash App are more vulnerable than ever. Industry data shows that the average eCommerce chargeback costs a staggering $110 per incident. Worse, 13% of merchants are already in breach of the monitoring thresholds. The risk has never been greater.

This is exactly why platforms like Disputely exist. We help you prevent these disputes from ever hitting your record in the first place, letting you sidestep the penalties and protect your hard-earned revenue. See our plans here: https://disputely.com/pricing

Why Do Most Cash App Chargebacks Happen Anyway?

If you want to stop Cash App chargebacks, you have to get to the root of the problem. It’s tempting to think every dispute is a scam, but the reality is a lot more complicated. Most chargebacks aren’t started by hardened criminals but by regular customers dealing with everyday situations.

Think of it like this: chargebacks come in three main flavors—criminal fraud, merchant error, and the biggest one of all, friendly fraud. Each has its own story and requires a completely different approach to fix. Getting a handle on these causes is the first real step toward building a defense that actually protects your business.

The Three Faces of Chargebacks

Not all disputes are cut from the same cloth. Some are straight-up theft, while others are just honest mistakes—either on your end or the customer's.

Here’s a quick rundown of what you’re up against:

- Criminal Fraud: This is the one everyone thinks of first. A thief gets their hands on stolen card details and uses them to buy something through Cash App. While it's a serious crime, it’s not nearly as common as most merchants believe.

- Merchant Error: Let's be honest—sometimes, we’re the problem. Things like confusing billing descriptors, shipping delays, a product that doesn't live up to its description, or a hard-to-find refund policy can all lead to frustrated customers filing a dispute. These are preventable slip-ups.

- Friendly Fraud: This is the silent killer of your profit margins. A real customer buys something, gets exactly what they paid for, and then disputes the charge anyway. It’s not usually malicious; it’s often just confusion, forgetfulness, or a classic case of buyer's remorse.

While all three cause headaches, friendly fraud is by far the most common and frustrating. Why? Because the customer isn't trying to be a bad guy.

Why Friendly Fraud Is Such a Big Deal

When it comes to chargebacks, friendly fraud is the undisputed heavyweight champion. It’s what happens when good customers do something that creates a bad outcome for you, often without even realizing the damage they’re causing. They aren't trying to rip you off; they're just trying to solve a problem the quickest way they know how: by calling their bank.

This is the engine driving the vast majority of Cash App chargebacks, turning perfectly happy customers into accidental problems for your business. The numbers are pretty shocking. Studies show that friendly fraud is behind roughly 75% of all chargeback cases worldwide, and Cash App is no exception. In fact, a staggering 72% of merchants say they've seen a major spike in these so-called "friendly" disputes. You can dig deeper into the data by checking out the latest eCommerce chargeback statistics and trends.

Friendly fraud is usually born from a simple misunderstanding. The customer doesn’t recognize your business name on their statement, forgot they signed up for a subscription, or their kid used their card without permission. The end result is always the same: a costly, time-consuming dispute for you.

Just think about these common, real-world examples:

- Subscription Amnesia: A customer signs up for a free trial and completely forgets to cancel. A month later, a charge from a company they don't recognize hits their account, so they immediately file a dispute.

- The Family Purchase: A teenager grabs their parent's phone and buys some in-game currency using the connected Cash App account. The parent sees the charge, assumes it's fraud, and disputes it.

- Impulse Regret: Someone makes a late-night purchase and wakes up with a case of buyer's remorse. Instead of going through the hassle of a return, they take the easy way out and call their bank to reverse the charge.

In every one of these situations, the customer got exactly what they paid for. But a simple moment of confusion or regret kicks off a formal chargeback process that costs you money, eats up your time, and hurts your reputation with payment processors. This is precisely why you need a way to get ahead of these misunderstandings before they turn into full-blown disputes.

How to Proactively Stop Chargebacks Before They Start

Fighting a Cash App chargeback after it hits your account is like trying to put out a fire that’s already raging. You’re playing defense, scrambling for evidence, and often facing an uphill battle you’re practically guaranteed to lose. But what if you could get an alert the moment a customer even thinks about lighting the match?

This is where a proactive strategy completely changes the game. Instead of reacting to damage that’s already been done, you can get ahead of disputes and stop them from ever becoming a formal chargeback. It’s the difference between damage control and total prevention.

The Power of an Early Warning System

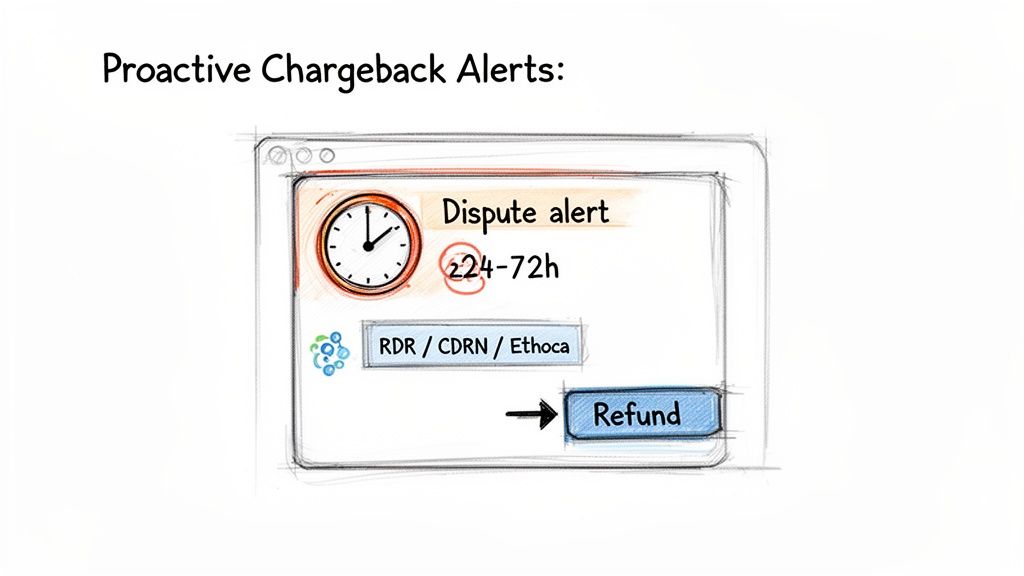

Picture this: a customer is confused about a charge on their statement. Instead of you finding out weeks later through a formal dispute notification, a system instantly alerts you the second they call their bank. This is precisely what chargeback alert networks do.

Services from the major card brands—Visa’s Rapid Dispute Resolution (RDR) and Mastercard’s Chargeback Dispute Resolution Network (CDRN), along with alerts from Ethoca—act as a powerful early warning system. They create a direct line of communication between the customer’s bank and you, the merchant.

This gives you a critical, albeit brief, window of opportunity.

A chargeback alert gives you 24 to 72 hours to resolve a customer’s issue directly by issuing a refund. If you act within this timeframe, the bank stops the dispute process, and a formal chargeback is never filed.

This single capability transforms your entire approach. You move from a defensive, reactive position to an offensive one, taking control of the situation before it can actually harm your business.

How Alert Networks Stop a Cash App Chargeback

When a customer disputes a Cash App payment funded by their card, that dispute enters the Visa or Mastercard network. Platforms like Disputely integrate directly into these networks, acting as your digital lookout.

Here’s how it works, step-by-step:

- Customer Initiates a Dispute: A customer contacts their bank to question a charge from your business.

- The Bank Triggers an Alert: Before filing a formal chargeback, the bank sends an inquiry through the RDR or CDRN network.

- Disputely Intercepts the Alert: Our platform catches this alert in real-time, 24/7.

- You Issue an Automatic Refund: Based on rules you set, Disputely can automatically refund the transaction through your payment processor (like Stripe or Shopify Payments).

- The Chargeback Is Prevented: The bank is notified of the refund and closes the inquiry. The dispute never escalates into a damaging chargeback on your record.

This automated process shields your business from the most severe consequences of disputes. You avoid the non-refundable chargeback fees, protect your crucial chargeback-to-sales ratio, and free up your team from the administrative headache of fighting lost causes. You can learn more about how this protects merchants from painful consequences like a Shopify payment hold, which is often triggered by high dispute rates.

This screenshot from Disputely shows how you can track and manage these alerts to stop chargebacks before they happen.

The key insight here is visibility. Instead of being blindsided, you get a real-time overview of potential disputes, empowering you to take immediate, preventative action.

The Strategic Choice to Refund

At first glance, the idea of refunding every alerted dispute might seem backward. Why give money back without a fight? The answer lies in simple math and smart risk management.

Think about the true cost of a single chargeback: the lost revenue, the $15-$100 fee, the operational overhead, and the risk to your merchant account. When you refund through an alert, you only lose the transaction amount. You completely sidestep all the additional penalties.

For the vast majority of disputes, especially those driven by friendly fraud, refunding is simply the smarter financial decision. It’s a small, controlled loss that prevents a much larger, more unpredictable one. By adopting a proactive alert system, you’re not just stopping chargebacks—you’re protecting your ability to process payments for the long haul.

Building a Winning Defense for Unavoidable Disputes

While being proactive is always your best bet, some disputes are just going to happen. You might run into a clear-cut case of "friendly fraud" where you have all the proof you need, or maybe the disputed amount is simply too big to ignore. When that happens, you have to switch gears from prevention to building an airtight defense.

Fighting a Cash App chargeback isn't about just sending a bunch of random documents to your payment processor and crossing your fingers. It’s about building a logical, evidence-backed argument that directly picks apart the customer’s claim. Winning here comes down to being organized, acting fast, and thinking strategically.

Your Essential Evidence Checklist

The moment a dispute hits your account, the clock starts ticking. Your processor will give you a hard deadline—usually somewhere between 20 and 45 days—to get your response in. The very first thing you should do is gather every piece of evidence related to the specific reason for the dispute.

Think like a detective building a case. Your evidence needs to tell a compelling story that proves the transaction was totally legitimate.

- Proof of Delivery: This is the big one for physical products. You absolutely need a tracking number from a reliable carrier showing the item was successfully delivered to the customer's address. A "shipped" status won't cut it; it has to say "delivered."

- Customer Communications: Pull together every email, chat log, or support ticket you have with the customer. This can show that you tried to resolve their issues, offered support, or that they even confirmed they received the product.

- Service Usage Data: If you sell digital goods or services, this is your version of a tracking number. Show logs that prove the customer logged in, downloaded the file, or used your service after they paid.

- Order and Transaction Details: Make sure you have the invoices, receipts, and order confirmations that line up with the charge. It's also smart to highlight how your business name appears on their statement to counter any "unrecognized transaction" claims.

Assembling Your Rebuttal

Once you have all your evidence, the next step is to present it in a way that’s clean and easy to follow. A messy, disorganized submission will just confuse the bank that's reviewing the case. Your job is to make it dead simple for them to understand your side.

A strong rebuttal is a direct response to the cardholder's claim. Don't just submit a pile of documents; write a brief, professional summary that explains what each piece of evidence proves and how it refutes the customer's specific reason for the chargeback.

For instance, if the dispute reason is "Product Not Received," your delivery confirmation should be front and center. If it’s "Transaction Not Recognized," lead with the order confirmation and maybe a screenshot of your checkout page. Always lead with your strongest proof.

Fighting disputes takes a lot of effort, and honestly, the win rates can be tough—often sitting around 25-35% for merchants. But for big-ticket orders or obvious cases of fraud, putting together a solid defense is definitely worth your time. To learn more about improving your odds during busy times, check out our guide on Q4 representment strategies. By being methodical and letting the evidence do the talking, you give yourself the best possible shot at winning the fights you choose to take on.

A Few Lingering Questions About Cash App Chargebacks

Even with a solid understanding of the basics, a few practical questions always seem to pop up when merchants face a Cash App dispute. Let's tackle some of the most common ones I hear.

Is It Better To Just Stop Accepting Cash App Payments?

I get this question a lot. While technically you could refuse Cash App payments, you’d be turning away a growing number of customers and leaving money on the table. The real issue isn’t Cash App itself—it’s the underlying card used to fund the transaction.

A far smarter approach is to keep serving those customers but get ahead of the risk. By using a chargeback alert system, you can safely accept more payment types without exposing your business to the financial hit and hassle of disputes.

How Much Time Do I Really Have To Respond To A Chargeback?

Your processor will give you an official deadline, usually somewhere between 20 and 45 days. But treating that as your true timeframe is a huge mistake. Think of it as the absolute final, last-minute cutoff.

With a prevention tool like Disputely, you get a much more valuable heads-up—a 24 to 72-hour window to simply refund the customer and stop the chargeback before it even starts. If you decide to fight it, getting your evidence in right away dramatically increases your odds of winning.

Waiting until the last minute is one of the easiest ways to lose a dispute. Whether you plan to refund or fight, speed is your biggest advantage.

Does Disputely Work With The Cash App Card?

Yes, it does, and this is a key point. The Cash App Card is a standard Visa or Mastercard debit card. When a cardholder disputes a transaction made with it, that dispute follows the exact same path through the card network as any other.

Because Disputely plugs directly into Visa's RDR and Mastercard's CDRN alert networks, we see these disputes the moment they are filed. This gives you the chance to issue an immediate refund, preventing the formal chargeback from ever damaging your merchant account.

Stop letting preventable disputes drain your revenue. Disputely connects with your payment processor in minutes to stop Cash App chargebacks before they cost you. See how much you can save and protect your business today at https://www.disputely.com.