The Ultimate Guide to a Chargeback for Debit Card Transactions

Think of a debit card chargeback as your bank's secret weapon. It’s a powerful process that lets them go in and reverse a transaction, pulling money directly out of a merchant’s bank account and putting it back into yours. This isn't like a credit card dispute that involves the bank's line of credit; a debit card chargeback is about reclaiming your own hard-earned cash that's already left your checking account.

What Is a Debit Card Chargeback and Why It Matters

When you swipe your debit card, money flows from your account to the merchant's almost instantly. But what happens when that transaction is a mistake? Maybe you were charged for an order that never showed up, or worse, a fraudster got ahold of your card details. That’s where the chargeback comes in.

It acts as an "undo" button, giving your bank the authority to step in, investigate what happened, and, if your claim is valid, forcibly take back your money. This isn't just a courtesy; it's a fundamental consumer right backed by laws like the Electronic Fund Transfer Act (EFTA) and the rules set by card networks like Visa and Mastercard. Without it, the trust we place in electronic payments would crumble.

The Core Difference From Credit Card Disputes

People often use the term "chargeback" for both debit and credit cards, but there's a crucial difference under the hood: where the money comes from.

When you dispute a credit card charge, you're dealing with the bank's money—a line of credit they extended to you. The bank is fighting to get its funds back. With a debit card chargeback, it's your cash on the line. The money has already left your checking account, which makes the whole situation feel much more personal and urgent.

Key Takeaway: A debit card chargeback reclaims your own funds from your checking account. A credit card chargeback reverses a charge against your line of credit. This fundamental difference shapes the rules, timelines, and protections for each.

Let's quickly break down the key distinctions.

Debit Card Chargeback vs Credit Card Chargeback at a Glance

| Feature | Debit Card Chargeback | Credit Card Chargeback |

|---|---|---|

| Source of Funds | Your actual cash from your checking account. | A line of credit extended by the card issuer. |

| Governing Law | Primarily the Electronic Fund Transfer Act (EFTA). | Primarily the Fair Credit Billing Act (FCBA). |

| Typical Process | Involves direct reversal of settled funds. | Involves withholding payment from the merchant. |

| Consumer Urgency | High, as your own money is gone. | Lower, as it's the bank's money at risk. |

As you can see, while the goal is the same—getting your money back—the mechanics and legal frameworks are quite different.

Common Scenarios for Initiating a Chargeback

It’s important to know when a chargeback is the right tool for the job. It’s not meant for a simple case of "buyer's remorse." Instead, it’s reserved for legitimate disputes where you can't get a resolution directly from the merchant.

Here are the most common reasons you'd file a chargeback for a debit card purchase:

- Fraudulent Transactions: This is the big one. If a thief gets your card info and goes on a shopping spree, a chargeback is your first line of defense to recover the stolen money.

- Product Not Received: You ordered something online, weeks have gone by, and there’s no sign of your package. The merchant isn’t responding, and the tracking is dead.

- Services Not Rendered: You paid a deposit for a service that was never completed or pre-paid for an event that was canceled without a refund.

- Product Significantly Not as Described: You ordered a genuine leather jacket and received a cheap plastic knock-off. Or, the gadget you bought arrived broken and is clearly not the "new" item you paid for.

- Technical Errors: Glitches happen. You might have been accidentally charged twice for one meal (duplicate transaction) or billed the wrong amount at the checkout.

Understanding these valid reasons helps you know exactly when to pull the trigger on a chargeback, turning a frustrating financial problem into a solvable one.

How Cardholders Can Navigate the Chargeback Process

Finding a weird charge on your debit card statement is always a sinking feeling. But don't panic—there's a well-defined process to get your money back. The key is to be methodical and start preparing long before you even think about calling your bank.

Your first move, and honestly the most important one, should always be to contact the merchant directly. You'd be surprised how often this works. A quick phone call or email can resolve the entire problem in a few days, saving you from the weeks (or even months) a formal dispute can take. It's faster, cleaner, and keeps things from getting unnecessarily complicated.

Step 1: Contact the Merchant First

Before you jump to filing a chargeback for a debit card, give the business a chance to make it right. Reach out to their customer service team and clearly explain what's wrong. Is it a double charge? A package that never showed up? Or maybe the item you received looks nothing like what you ordered?

Have your details ready: the date of the transaction, the exact amount, and any order numbers you have. Many times, these issues are just simple mistakes or shipping errors that the merchant is more than willing to fix with a quick refund.

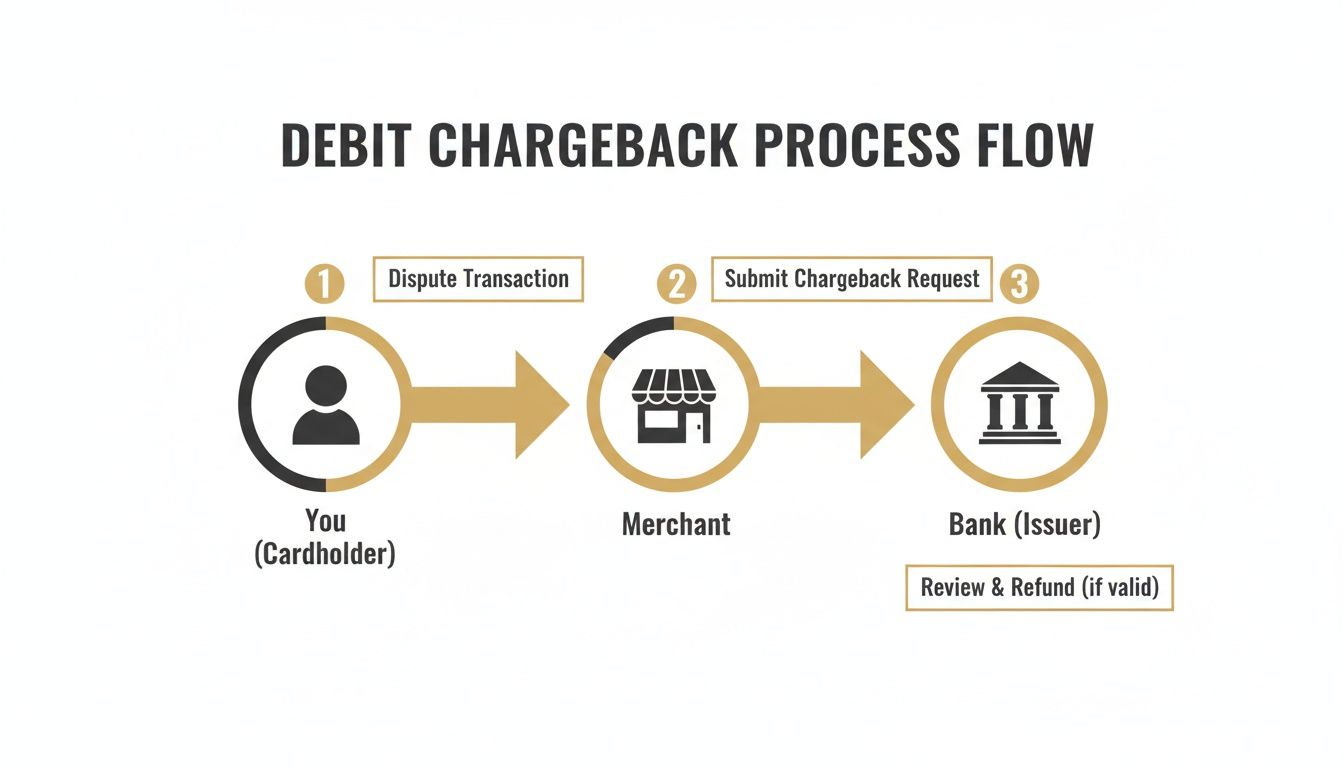

This flowchart breaks down the typical process. As you can see, it all starts with a conversation between you and the merchant. The banks only get involved if that first step fails.

Think of the bank as your backup, not your first line of defense.

Step 2: Gather Your Evidence

Okay, so what if the merchant ignores you or flat-out refuses to help? Now it's time to build your case. Your bank isn’t just going to take your word for it; they need proof. Treat this like you're a detective gathering all the clues you can find to prove your side of the story.

Your evidence file should be airtight. Make sure you have:

- Proof of Purchase: Receipts, order confirmation emails, packing slips—anything that proves you bought it.

- Merchant Communication: This is huge. Save every email, screenshot any chat logs, and jot down notes from phone calls (who you talked to, when, and what was said). This shows you tried to resolve it yourself.

- Visual Proof: If a product is damaged, counterfeit, or just plain wrong, pictures and videos are your best friends.

- Supporting Documents: Did you get a tracking number that shows the package went to the wrong state? Or a cancellation confirmation for a service you were still charged for? Include it.

The more organized and detailed your evidence is, the stronger your case will be.

Step 3: Initiate the Dispute with Your Bank

With all your evidence in a neat little pile, you’re ready to file the dispute. Most banks let you do this right from your online account, but you can also call them or walk into a branch. You'll need to give them the specifics: merchant name, transaction date, and the exact dollar amount.

You’ll have to clearly explain why you're disputing the charge and point to the evidence you've collected. Be sure to use the bank's official dispute forms and submit everything they ask for right away to keep things from getting held up.

Once you file, the bank starts its review. They’ll often give you a provisional credit for the disputed amount while they investigate. Just remember, this credit is temporary. If the merchant successfully fights the chargeback, the bank will take that money right back out of your account.

Interestingly, debit cards have a much lower chargeback rate than credit cards. Recent data shows the debit card chargeback ratio is only 5.93%, compared to 7.19% for credit cards. It seems people are a bit more careful when the money comes directly out of their bank account.

The bank’s investigation can take a while—often up to 90 days—as they go back and forth between you and the merchant. If they ask you for more information during this time, get back to them ASAP. The faster you respond, the smoother the process will be. For more help navigating these situations, feel free to check out our dedicated support resources.

How Merchants Can Prevent and Respond to Disputes

For any merchant, a chargeback for a debit card purchase isn't just a lost sale. It's a direct hit to your bottom line and can even jeopardize your relationship with payment processors. The key to handling this risk is a two-pronged approach: get ahead of disputes before they even happen, and know how to fight back effectively when they do.

Winning the chargeback game often starts long before a customer clicks "dispute." Proactive prevention is your single most powerful weapon. Simple, thoughtful tweaks to how you run your business can stamp out the root causes of many disputes, especially those that pop up from simple confusion or miscommunication.

This strategy doesn't just save you the sale amount. It helps you dodge extra fees and, most importantly, protects your chargeback ratio—a metric that payment processors watch like a hawk.

Proactive Prevention Best Practices

The old saying holds true: the best defense is a good offense. By making your business transparent, clear, and customer-friendly, you can stop a huge number of disputes in their tracks. A few small adjustments can make a world of difference.

Here are the most effective strategies to put into practice:

- Crystal-Clear Billing Descriptors: Make sure the name that shows up on a customer's bank statement is one they'll actually recognize. A cryptic descriptor like "SRVCS-WEB" is a classic trigger for "I don't recognize this charge" disputes. Always use your business name or website.

- Transparent Policies: Don't hide your refund, return, and cancellation policies. They need to be front-and-center and written in plain English. Any gray area can lead to customer frustration, turning a minor issue into a formal dispute.

- Stellar Customer Service: Give customers an easy way to reach you. A quick, helpful response from your support team can solve a problem with a simple refund, which is always better than a damaging chargeback.

Nailing these three areas helps you tackle the main drivers of so-called "friendly fraud" and customer-error chargebacks.

Responding to a Dispute with Compelling Evidence

Even with the best preventative measures, some chargebacks are simply unavoidable. When a dispute comes in, the clock starts ticking. You have a short window to submit your rebuttal—your one chance to present evidence proving the transaction was legitimate and that you held up your end of the bargain.

A strong rebuttal package is organized and directly tackles the customer's claim. You'll need to tailor your evidence to the specific reason code provided with the dispute. For any online business, choosing the right payment processor is a foundational step in managing these kinds of risks. To see what's out there, you might want to look into some of the Top Payment Gateways for Ecommerce.

Here’s the essential evidence you should gather:

- Proof of Authorization: This includes AVS (Address Verification System) and CVV match results.

- Order and Shipping Details: Think invoices, packing slips, and especially delivery confirmation showing the package arrived at the customer's address.

- Customer Communication: Pull any emails, chat logs, or call notes that show you tried to resolve the problem directly with the customer.

Your goal is to tell a clear, evidence-backed story to the issuing bank. A well-documented response proves you acted in good faith and significantly increases your chances of winning the dispute.

The Power of Automation and Chargeback Alerts

Trying to fight every chargeback by hand is a drain on your time and resources, especially if you're dealing with a high volume of orders. Thankfully, modern tools offer a much smarter way to handle this through automation and real-time alerts.

Chargeback alert services plug directly into your payment processor (like Shopify, Stripe, or PayPal) and send you a notification the moment a customer starts a dispute with their bank. Crucially, this alert arrives before the formal chargeback is filed. This heads-up gives you a critical 24-72 hour window to react. You can jump in and issue a refund immediately, which makes the customer happy and stops the dispute from ever hitting your record as an official chargeback.

This automated refund process is a total game-changer. It protects your chargeback ratio, helps you steer clear of high-risk monitoring programs, and stops processors from putting a freeze on your funds. For merchants on Shopify, avoiding these headaches is vital, and you can learn more in our guide on how to resolve a https://disputely.com/shopify-hold.

This technology has become more critical than ever. The global number of chargebacks is exploding, projected to jump from 238 million cases in 2023 to 337 million by 2026—that’s a massive 41% increase in just three years. This trend is fueled by the boom in card-not-present (CNP) transactions, which now represent 63% of all merchant sales worldwide. For any business with recurring billing or high sales volume, automated prevention isn’t a luxury anymore; it's a must-have for survival.

Decoding Chargeback Reason Codes for Merchants

If you want to successfully fight a debit card chargeback, you first have to learn to speak the bank's language. Every single dispute comes tagged with an alphanumeric "reason code," which is basically the card network's shorthand for why the customer is upset.

Think of it as a case file number that also reveals the core of the complaint. Ignoring this code is like showing up to court without knowing the charges. By understanding what it means, you can stop guessing and start building a rebuttal with the right evidence to directly counter the customer's specific claim. It’s the key to turning your response from a shot in the dark into a strategic defense.

The Four Main Flavors of Disputes

While there are dozens of individual codes, they nearly all fall into four main categories. Each one points to a different kind of problem and, critically, requires a completely different type of evidence from you to win.

- Fraud: This is the most clear-cut category. The cardholder is flat-out claiming they didn't authorize or participate in the transaction. This is your classic stolen card number scenario.

- Authorization: These codes flag a technical hiccup during the payment approval step. Maybe the transaction was declined but your system processed it anyway, or perhaps you didn’t follow the correct authorization procedures.

- Processing Errors: This bucket is for clerical mistakes. This is where you see claims for being billed the wrong amount, getting charged twice for one item (duplicate processing), or a promised refund that never showed up on their statement.

- Consumer Disputes: This is the biggest, messiest, and most complicated category, often where "friendly fraud" lives. In these cases, the customer fully admits to making the purchase. The problem is they're now unhappy, claiming the product never arrived, was broken, or simply wasn't what they expected.

Just knowing which of these four buckets a dispute falls into is the essential first step. A fraud claim demands proof that the legitimate cardholder was involved, whereas a consumer dispute needs you to prove you held up your end of the bargain.

Connecting Evidence to Common Reason Codes

Okay, let's get practical. The reason code tells you exactly what kind of proof the bank needs to see to even consider reversing the chargeback. Sending a mountain of paperwork is useless if it's not the right paperwork. Your evidence must directly disprove the specific claim.

A "Transaction Not Recognized" claim requires a totally different defense than a "Product Not Received" claim. To help you connect the dots, here’s a breakdown of common chargeback scenarios.

Common Debit Card Chargeback Reason Codes and Required Evidence

The table below breaks down some of the most frequent reason codes you'll encounter. Think of it as your cheat sheet for knowing what the bank wants to see when you represent your case.

| Reason Code Category | Example Code (Visa/Mastercard) | Meaning | Required Compelling Evidence |

|---|---|---|---|

| Fraud | 10.4 (Visa), 4837 (Mastercard) | The cardholder claims they don't recognize the transaction and it's likely fraudulent. | AVS/CVV match results; IP address matching the billing address; delivery confirmation to the cardholder's address; proof of prior undisputed transactions from the same customer. |

| Consumer Dispute | 13.1 (Visa), 4853 (Mastercard) | The customer says the product or service was never delivered or provided. | Dated proof of shipping (tracking number showing "delivered"); a signed receipt or photo of the delivery; for digital goods, server/activity logs showing the customer accessed or downloaded the product. |

| Consumer Dispute | 13.3 (Visa), 4853 (Mastercard) | The item arrived but was defective, damaged, or significantly different from the product description. | A copy of the original product description and photos from your website; any communication with the customer trying to resolve the issue (e.g., emails offering a return or replacement); proof that your return policy was clearly visible. |

| Processing Error | 12.6 (Visa), 4834 (Mastercard) | The customer was charged twice or more for a single transaction. | Transaction records showing only a single charge was processed. If a duplicate was processed and refunded, provide documentation of the credit to the customer's account. |

Winning a chargeback is all about the quality and relevance of your evidence. A signed delivery confirmation for a "Product Not Received" claim is often an instant win, while vague transaction logs won't be nearly as convincing.

A signed delivery receipt or a clear photo of the package on the customer's doorstep is often the silver bullet for "not received" claims. Without it, the bank will almost always side with the cardholder.

The True Financial Impact of Chargebacks on Your Business

Think a chargeback just means you lose a sale? Think again. A chargeback is less like a simple refund and more like a financial grenade tossed into your operations. The lost transaction is just the initial sting; beneath the surface, a whole slew of hidden costs and operational headaches can seriously wreck your profitability.

Each dispute isn't just a deduction—it's a multiplier of loss. The real cost of a single chargeback can easily be more than double the original sale price. Once you grasp this, it becomes crystal clear why a solid prevention strategy isn't just a nice-to-have. It’s essential for survival.

Beyond the Lost Sale: The Direct Financial Penalties

The moment a customer files a chargeback for a debit card purchase, the financial damage starts piling up. It’s not just about giving the money back; it’s about the extra penalties the payment ecosystem slaps on you for the trouble.

Here’s a breakdown of the immediate hit you'll take:

- The Original Transaction Amount: The full sale amount gets yanked from your merchant account and handed back to the customer as a temporary credit. You lose 100% of the revenue from that sale, right off the bat.

- Non-Refundable Processing Fees: Those credit card processing fees you paid to make the sale happen? You don’t get those back. They’re gone for good, usually costing you 2% to 3% of the transaction.

- Chargeback Fees: This is the big one. Your bank will hit you with a separate, non-refundable penalty for every single dispute. These fees range anywhere from $20 to over $100 per incident, and you have to pay them whether you win or lose.

Put it all together, and the picture gets ugly fast. A simple $50 sale that becomes a chargeback can easily cost your business over $175 once you add up the lost revenue, sunk processing fees, and a steep bank penalty. For businesses handling hundreds of transactions daily, these costs can become staggering.

The Hidden Operational Costs and Long-Term Damage

But the bleeding doesn't stop with the direct fees. The secondary costs, while tougher to pin down on a spreadsheet, can be even more destructive over time. These are the operational burdens that drain your two most precious resources: your team's time and focus.

Think about the hours someone on your team has to spend just to deal with one dispute. They have to drop what they're doing to hunt through records, gather proof, write a compelling rebuttal letter, and get it all submitted before a tight deadline. That’s time they could have spent growing the business, not just defending it.

The total cost of a chargeback, factoring in fees, operational expenses, and lost overhead, can reach up to 250% of the original disputed purchase amount. This makes every dispute a significant financial event that requires careful attention.

Beyond the immediate scramble, there's a more serious threat looming: your relationship with payment processors. Every chargeback nudges your chargeback ratio—the percentage of your transactions that end in a dispute—a little higher. If that ratio climbs too high (the industry red flag is typically over 0.9%), you set off alarms with card networks like Visa and Mastercard.

This can trigger some pretty severe consequences:

- High-Risk Monitoring Programs: You could be forced into a monitoring program, which brings its own monthly fines and intense scrutiny.

- Account Termination: The absolute worst-case scenario is having your merchant account shut down. Suddenly, you can't accept card payments, which for most businesses, is a death sentence.

To truly understand the risks, a modern risk analysis for businesses is a critical step for protecting your long-term viability.

A Real-World Example of Spiraling Costs

Let’s see how this plays out for a small e-commerce store that sells a $100 product. If they get just 10 chargebacks in one month, the math is sobering.

- Lost Revenue: 10 sales x $100 = $1,000

- Lost Processing Fees (at 2.5%): 10 x $2.50 = $25

- Chargeback Fees (at $50/incident): 10 x $50 = $500

The immediate, direct loss is $1,525—more than 1.5 times the value of the products they sold. And that’s before you even factor in the cost of paying an employee to fight these disputes.

This simple example makes it painfully clear: treating chargebacks as just "a cost of doing business" is a recipe for disaster. Prevention, combined with smart automation for responding to disputes, is the only way forward. Platforms that help manage this process are invaluable; you can even see your potential savings with a chargeback pricing calculator.

A Few Common Questions About Debit Card Chargebacks

Even with a good map, the world of debit card chargebacks can feel like it's full of confusing twists and turns. Here are some quick, straight-to-the-point answers to the questions I hear most often from both shoppers and business owners.

How Long Do I Have to File a Chargeback?

The countdown begins the second a transaction happens, but how long you have to act really depends on why you're disputing the charge. My best advice? Don't wait.

For straight-up fraud or unauthorized charges, U.S. federal law (Regulation E) is pretty strict: you have 60 days from the day your bank statement was sent to report it. If the issue is something else—maybe the product never showed up, or it was completely broken—the card network rules from Visa or Mastercard are usually a bit more forgiving, often giving you up to 120 days from the transaction date.

The Bottom Line: You might have up to 120 days for service issues, but you absolutely must report fraud within 60 days of your statement date. It’s always smart to double-check your own bank’s policy, as some have slightly different timelines.

Can a Merchant Just Refuse a Debit Card Chargeback?

Nope. A merchant can't simply say "no" or ignore a chargeback. The moment you file a dispute with your bank, a formal process kicks off, and the merchant is legally required to respond.

Their one and only move is to fight the claim, a process known as representment. This is their chance to present solid proof to the bank that the charge was legitimate and they held up their end of the bargain. If they miss their deadline or their evidence doesn't hold up, they lose by default.

What Happens if I Lose the Dispute?

If you file a chargeback for a debit card and the bank sides with the merchant, what happens next is pretty simple. That temporary credit your bank gave you at the start of the investigation gets taken back.

Your bank will send you a final notice explaining the decision. From there, your options are pretty slim. Some banks might let you appeal it (this is sometimes called a second chargeback or pre-arbitration), but for the most part, a lost dispute means the charge stands.

Is a Debit Card Chargeback the Same Thing as a Refund?

Not at all—they're two completely different animals.

A refund is a friendly, direct conversation between you and the merchant. You ask for your money back, they say okay, and the funds are returned. It's a cooperative and simple resolution.

A chargeback, on the other hand, is a forced reversal. It's a formal consumer protection tool you use as a last resort when a merchant won't work with you. It brings your bank and their bank into the ring to settle things. From a merchant’s perspective, refunds are always the better option, since chargebacks come with steep fees and can seriously harm their relationship with payment processors.

Stop letting preventable disputes drain your revenue. Disputely connects directly with card networks to give you real-time alerts on new chargebacks. This gives you a critical window to issue a refund and protect your merchant account before the damage is done. See how much you can save and get started today at Disputely.