Your Guide to Fighting and Winning a Chargeback for Fraud

When you hear "chargeback for fraud," you probably picture a scene straight out of a movie: a shadowy figure using a stolen credit card to buy things online. While that kind of criminal fraud still happens, it’s not the biggest headache for businesses anymore. The real, growing crisis is something much more subtle and, frankly, more frustrating.

The Real Story Behind Today's Fraud Chargebacks

Think of it like this: your store's return counter is suddenly flooded with people demanding their money back, after they’ve already used and kept the product. That’s what the modern chargeback landscape feels like for countless online merchants.

The issue isn't just about thieves with stolen card numbers. The far more common problem today is what’s known as "friendly fraud" or first-party misuse. This is when the legitimate cardholder—your actual customer—makes a purchase and then turns around and disputes the charge with their bank.

The Rise of First-Party Misuse

This isn't always done with bad intentions. Sometimes a customer genuinely doesn't recognize your business name on their bank statement. Or maybe they simply forgot they subscribed to your service.

But often, it's deliberate. It's a way to get a product for free, a tactic some call "cyber shoplifting." Whether it's accidental or intentional, the outcome for your business is identical: a lost sale, a lost product, and a hefty chargeback fee.

The global chargeback landscape has undergone a dramatic transformation. What makes this crisis particularly urgent for merchants is that the underlying problem isn't primarily sophisticated cybercriminals—it's first-party misuse.

The numbers are staggering. A Mastercard-backed study from Datos Insights predicts that fraudulent chargebacks will drain $15 billion from businesses worldwide by 2025. Even more telling is that first-party fraud is now the single biggest reason for disputes, making up a massive 45% of all chargebacks globally. You can dig into the full research about these chargeback trends to see just how big this problem has become.

Why This Hurts Your Business

A chargeback for fraud is much more than just a simple refund. It's a direct hit to your bottom line and triggers a painful chain reaction:

- Financial Loss: The revenue from the sale is yanked back.

- Inventory Loss: You're out the product or service you already delivered.

- Penalty Fees: Your bank slaps you with a non-refundable fee for every single dispute.

Fighting this constant battle against both real fraud and false claims doesn't just cost you money; it puts your relationship with your payment processor in jeopardy. That’s why getting ahead of these disputes is more critical than ever.

The Hidden Costs of a Single Fraud Chargeback

It’s easy to think of a fraud chargeback as just a reversed sale, but that’s a dangerous oversimplification. The lost revenue from the original transaction is only the tip of the iceberg. Underneath the surface, a whole mess of hidden costs pile up, turning what seems like a minor annoyance into a serious threat to your business.

The moment a customer files a dispute, your payment processor yanks the full transaction amount from your account. But they don't stop there. They also slap you with a non-refundable chargeback fee, usually somewhere between $20 and $100. You get hit with this fee whether you win or lose the fight, meaning every single claim starts as a net loss.

More Than Just Money

Beyond the immediate hit to your wallet, a chargeback for fraud sets off a chain reaction of operational headaches. Your team has to drop everything they’re doing—the stuff that actually grows your business—to dig into the claim, pull together evidence, and write a compelling rebuttal. This lost productivity is a silent killer of your bottom line.

Think about how quickly it all adds up. You’re already out the money for the product itself and the shipping costs, neither of which you'll ever see again. When you combine the lost sale, the penalty fee, and the internal time spent, the total cost can easily be double or triple the original purchase price. For businesses running on tight margins, these losses can be absolutely devastating.

The Real Danger: Your Merchant Account Ratio

The scariest part of fraud chargebacks isn't the cost of one dispute; it's the long-term damage they do to your standing with payment networks. Card brands like Visa and Mastercard are constantly watching your chargeback ratio—a simple calculation of your chargebacks versus your total transactions.

If that ratio creeps over their thresholds (which is often around 0.9%), you get flagged and can be forced into a monitoring program. That means higher processing fees, monthly fines, and, in the worst-case scenario, having your merchant account shut down completely. For an online business, losing the ability to accept credit cards is a death sentence. It’s also a key reason you might find yourself dealing with a Shopify Payments hold or payout reserve.

When you sit down and calculate the true cost of a chargeback, the numbers become genuinely staggering. For small and midsize businesses, this accumulated cost can be catastrophic.

The real-world fallout is no joke. Research highlighted by Mastercard reveals that while the average chargeback in the U.S. is $110, the actual cost to merchants climbs past $120 after accounting for all the fees and lost revenue. In fact, the report found that nearly 1 in 5 small businesses severely impacted by chargeback fraud had to file for bankruptcy. This is why managing your dispute rate isn't just about winning a few cases—it's about basic business survival.

Diving Into the Chargeback Dispute Lifecycle

When a chargeback for fraud lands on your plate, it’s not just another customer service ticket. It’s the start of a formal, rule-bound process that can feel incredibly rigid and intimidating. The best way to think about it is less like a negotiation and more like a mini-court case, complete with strict deadlines and a need for solid proof. Getting a handle on this journey is your first real step toward protecting your hard-earned revenue.

The whole thing kicks off the moment a customer calls their bank—what we call the issuing bank—to dispute a charge on their statement. They might say they never made the purchase, which triggers the bank to file a chargeback on their behalf. Almost instantly, the disputed funds are yanked from your merchant account and handed back to the customer on a temporary basis.

Who's Who in the Chargeback World

This isn't a simple two-way street between you and the customer. Several key players get involved, each with a specific job to do in determining the final outcome.

- The Cardholder: This is the customer, the person who owns the credit card and is flagging the transaction.

- The Issuing Bank: Think Chase, Bank of America, or Capital One. It's the cardholder's bank, and its first job is to advocate for its customer.

- The Acquiring Bank: This is your bank or payment processor—the Stripe, PayPal, or Shopify Payments of the world. They represent you in the process.

- The Card Network: Visa, Mastercard, and American Express act as the referees. They don't pick sides, but they set the rules everyone has to follow.

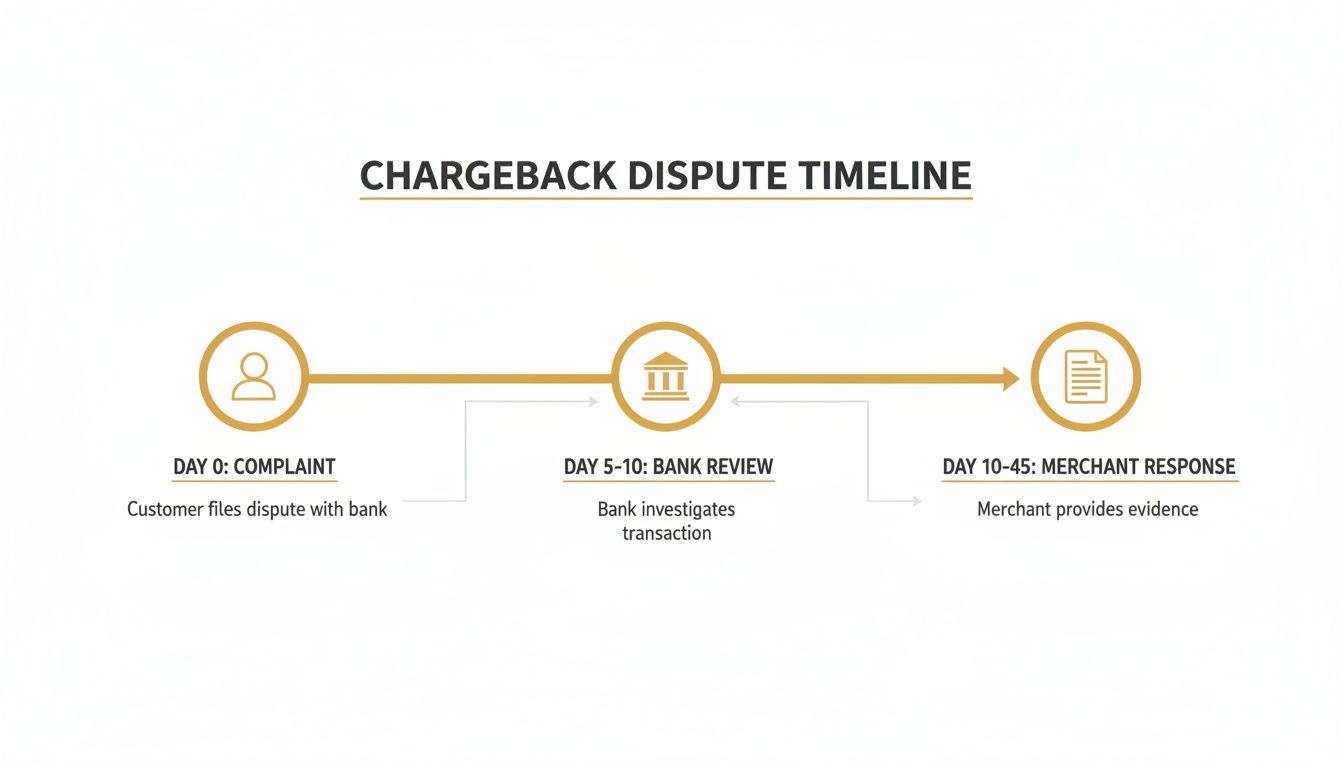

Once the issuing bank files the chargeback, the notification snakes its way through the card network to your acquiring bank, which then passes the bad news on to you. This is where the clock starts ticking, and it’s an unforgiving one. You’ll generally have somewhere between 20 and 45 days to gather your evidence and prove the transaction was legitimate.

The dispute lifecycle is a structured, evidence-based process. Missing a deadline or submitting weak evidence almost guarantees you will lose the dispute, along with the revenue and associated fees.

The Typical Stages of a Dispute

A fraud chargeback follows a predictable path, from the initial claim all the way to a final verdict. For merchants selling online, disputes can come from all corners; understanding the common hurdles faced by sellers dealing with an Amazon suspension or chargeback dispute can give you a good idea of how this plays out in the real world.

Let's walk through the timeline of a typical fraud dispute. This table breaks down what happens, when it happens, and who’s responsible at each step.

The Chargeback for Fraud Dispute Timeline

This table outlines the key stages, typical timeframe, and the responsible party during a fraud chargeback dispute.

| Stage | Typical Timeframe | Key Action and Responsibility |

|---|---|---|

| Chargeback Initiation | Day 0 | The cardholder contacts their issuing bank to dispute the charge. |

| Merchant Notification | Days 1-3 | Your acquiring bank receives the chargeback and notifies you. The clock starts. |

| Evidence Collection | Days 3-20 | The merchant (you) gathers all compelling evidence to prove the transaction's legitimacy. |

| Representment | Days 20-45 | The merchant submits the evidence packet to the acquiring bank, which then forwards it to the issuing bank. |

| Final Decision | Days 45-90 | The issuing bank reviews the evidence and decides whether to reverse the chargeback or let it stand. |

As you can see, the process isn't instant. The period where you can act is fairly short, but the final decision can take months.

Here’s a simpler way to think about the core stages you’ll be directly involved in:

- First Chargeback (or Retrieval): This is the initial alert. The dispute has been filed, and you’ve been notified. This is your one and only shot to present your case—a process we call "representment."

- Representment: You’ve built your case. Now, you submit your evidence packet back to your acquiring bank. They act as the courier, passing it along to the issuing bank for the final review.

- Bank Decision: The issuing bank plays judge and jury. If they agree with your evidence, the chargeback gets reversed, and the money comes back to you. If not, the chargeback is upheld, and the money stays with the customer.

Sure, if you lose, there are later stages like arbitration, but they’re expensive, time-consuming, and rarely worth the fight for a single transaction. That’s exactly why your first response has to be as strong and convincing as possible.

Building a Winning Case Against a Fraud Chargeback

Getting that notification for a chargeback for fraud can feel like a punch to the gut. It’s tempting to just write it off as a loss, but that’s a mistake. This is your chance to fight back and prove the transaction was legitimate. Winning this fight comes down to one thing: building an airtight case with compelling evidence.

Think of it like you're a detective piecing together clues. Your mission is to gather every bit of data that tells the true story of the transaction. You need to present a rebuttal that so clearly proves the purchase was authorized by the cardholder that the issuing bank has no other choice but to side with you.

Your Essential Evidence Checklist

A powerful rebuttal is all about the data. The more specific and detailed you are, the better your odds. Your first move should be to pull together every piece of transactional and customer data you have.

Here are the absolute must-haves for your evidence file:

- AVS and CVV Results: These are your front-line defense. Show that the Address Verification System (AVS) and Card Verification Value (CVV) checks were a match. It's a strong signal that the real cardholder was the one making the purchase.

- IP Address Geolocation: Pinpoint the IP address used for the order and show how it matches the cardholder's billing address. If they're in the same city, it’s much harder for someone to claim a random fraudster made the purchase.

- Signed Delivery Confirmation: If you sell physical products, a signature on delivery is gold. It’s hard evidence that the package arrived at the right address and someone was there to receive it.

- Customer Communications: Dig up any emails, chat logs, or support tickets. If the customer reached out about their order before claiming fraud, it shows they were fully aware of the purchase.

This timeline breaks down the typical stages of a dispute, from the moment the complaint is filed to when you need to respond.

As you can see, there’s a critical window where you have to get your evidence together and submit it. Timing is everything.

Tailoring Evidence for Your Business Model

The best evidence often depends on what you sell. The core goal is always the same: prove the customer got exactly what they paid for.

For Digital Products and Services: You can't get a delivery signature for a software download, so you need a different strategy. Use server logs to show the product was downloaded or that the customer logged into their account. For subscriptions, pull usage data, login histories, and any other activity logs that prove the service was actively used after the billing date.

A winning representment tells a clear, concise story backed by undeniable facts. Each piece of evidence should build on the last, systematically taking apart the cardholder's claim of fraud.

Putting together a strong case takes sharp record-keeping and a fast response. For a deeper dive, you can explore this guide on the chargeback representment process to pick up more advanced strategies. When you respond with a professional, evidence-loaded rebuttal, you dramatically improve your chances of reversing the chargeback and getting your money back where it belongs.

Why Proactive Prevention Beats Reactive Fighting

Winning a chargeback dispute can feel like a victory, but it's one that still hits your bottom line. You pour time and energy into building a case, not to mention the non-refundable fees you’ve already paid. Even when you win a chargeback for fraud, you never really come out ahead. This constant, reactive approach is like being a firefighter—always putting out fires instead of stopping them from ever starting.

A truly sustainable strategy means shifting from defense to offense. Proactive prevention isn't just about cutting your losses; it’s about safeguarding your profits, your team's focus, and your essential relationship with payment processors. Trying to fight every single dispute is a losing battle when you factor in the low average win rates and high labor costs.

Your First Line of Defense

A solid prevention plan starts right at the checkout page. There are some basic, yet powerful, tools that act as gatekeepers, filtering out obvious fraud before it ever becomes a headache.

For any ecommerce store, these checks are non-negotiable:

- Address Verification System (AVS): This is a simple but effective check. It confirms that the billing address a customer enters matches what the card-issuing bank has on file. A mismatch is a classic red flag.

- Card Verification Value (CVV): That little three or four-digit code on the back of the card is a crucial security layer. It helps prove the customer actually has the physical card in their hands.

- 3D Secure: You’ve probably seen this in action with services like Visa Secure or Mastercard Identity Check. It adds an extra authentication step where the customer has to enter a password or a one-time code sent to their phone to finalize the purchase.

While these tools are great for stopping clear-cut criminal fraud, they don't do much against the rising tide of friendly fraud. This is where a more sophisticated strategy is needed. A "refund hack" culture is blowing up on social media, creating a perfect storm for merchants. Recent data shows chargeback rates are climbing, with the retail ecommerce sector seeing a staggering 233% explosion. This spike is directly fueled by tutorials on platforms like TikTok, and an estimated 10% of consumers admit to trying these tactics themselves. You can explore the full findings on this refund hack economy to see just how big this problem has become.

The Game-Changer: Chargeback Alerts

This is where chargeback alerts completely change the game. Imagine getting a heads-up the moment a customer calls their bank to complain—before a formal chargeback is even filed. That's exactly what an alert system does.

Instead of waiting weeks for a formal dispute to land in your inbox, alerts give you a critical 24-72 hour window to act. This is your chance to resolve the issue directly with the customer, usually by issuing a refund, and stop the chargeback cold.

This single proactive step prevents the dispute from ever officially hitting your merchant account. You dodge the chargeback fee, protect your dispute ratio, and keep your business in good standing with the card networks. It’s the smartest way to turn a potential financial firefight into a simple customer service fix.

Automating Your Defense with Chargeback Alerts

Fighting a chargeback for fraud after it’s been filed is a necessary part of business, but what if you could sidestep the fight altogether? Think of it like a modern home security system. Instead of just recording a break-in after the fact, it warns you the moment someone steps onto your property, giving you a chance to act before they smash a window.

That’s exactly how chargeback alerts work for your business. These systems tap directly into alert networks run by major card brands like Visa and Mastercard. When a cardholder calls their bank to question a charge, the bank sends out a pre-dispute signal. An alert platform catches that signal instantly, opening up a critical 24-72 hour window for you to respond.

How Alert Systems Work

This small window of time is your golden opportunity. Instead of waiting days for a formal chargeback to land on your desk—bringing with it hefty fees and a hit to your dispute ratio—you can resolve the problem on the spot. Usually, this just means issuing a refund to the customer, which stops the chargeback dead in its tracks.

By connecting your payment processor, you can put this entire defense on autopilot. You simply set up custom rules defining which alerts get an automatic refund, and the system works for you 24/7. It’s a proactive strategy that saves you from penalties and protects your merchant account's health without you lifting a finger. To make this defense even stronger, you can integrate real-time monitoring and alerts to catch any unusual activity as it happens.

An alert system acts as an early-warning radar for potential chargebacks. It allows you to transform a costly dispute into a simple, automated refund, preserving your merchant account and saving you money.

This kind of automation is a game-changer for a few key reasons:

- Avoids Chargeback Fees: Because the dispute is never officially filed, you completely dodge the non-refundable penalty from your processor.

- Protects Your Ratio: A prevented chargeback never counts against your crucial dispute ratio with the card networks.

- Saves Time and Resources: Your team can finally stop spending hours gathering evidence and focus on what really matters: growing the business.

With an automated alert system, you’re no longer just reacting to problems. You’re getting ahead of them and keeping your revenue where it belongs. Curious about how this could impact your bottom line? You can explore different alert plans to find the right fit for your business.

Common Questions About Fraud Chargebacks

If you're dealing with fraud chargebacks, you've probably got questions. Let's break down some of the most common ones we hear from merchants trying to protect their bottom line.

What Is the Difference Between a Fraud Chargeback and Friendly Fraud?

This is a big one, and the distinction is crucial.

A true chargeback for fraud is exactly what it sounds like: a criminal got their hands on a stolen credit card and used it to buy something from your store. The real cardholder had no idea the transaction happened and is rightfully reporting it.

Friendly fraud is something else entirely. It's when the actual, legitimate cardholder makes a purchase but later disputes the charge. They might not recognize the transaction on their statement, have a case of buyer's remorse, or are trying to get something for free by falsely claiming fraud. For most online businesses, this is the real headache.

Can I Win a Fraud Chargeback with Proof of Delivery?

Yes, it's possible to win, but you're definitely fighting an uphill battle. When it comes to true fraud, the bank's default position is often to side with their customer, the cardholder.

To even have a shot, you need to build a compelling case with solid evidence. This includes:

- Proof of delivery showing the item arrived at the shipping address, especially if you have a signature confirmation.

- AVS and CVV match results to prove the correct card information was entered at checkout.

- IP address logs that place the order's origin at the cardholder's known location.

But even with all this, the odds aren't always in your favor. That’s why a proactive prevention strategy is so much more effective and less expensive than just fighting disputes after they’ve already happened.

A prevention-first strategy using alerts is far more reliable than fighting every dispute. It saves you from fees, protects your merchant account, and bypasses the uncertainty of bank decisions.

How Do Chargeback Alert Systems Actually Work?

Think of chargeback alert systems as your early warning signal.

When a customer calls their bank to question a charge, the bank doesn't immediately file a chargeback. Instead, it first sends a notification—an alert—through a network like Visa's RDR or Mastercard's CDRN.

An alert platform catches this notification for you in real-time. This opens up a precious 24-72 hour window for you to take action, which almost always means issuing a refund. By refunding the customer, you resolve the issue before it ever escalates into a formal, damaging chargeback. It’s a simple move that saves you from penalties and keeps your merchant account in good standing.

Stop losing revenue to preventable disputes. With Disputely, you can automatically intercept and resolve customer issues before they become costly chargebacks. See how much you can save and protect your business today.