A Merchant's Guide to Chargeback on a Debit Card

When a customer disputes a debit card purchase, it’s not just a simple refund request. A chargeback on a debit card is a powerful consumer protection tool where a customer’s bank steps in and forcibly reverses a transaction, pulling money directly out of your business account.

This process often happens without you even speaking to the customer first. It’s their last-resort option when they feel a charge was fraudulent, a product wasn’t delivered, or the service wasn’t what they paid for.

What Is a Debit Card Chargeback and How Does It Work?

Think of it this way: a refund is you giving money back to a customer. A debit card chargeback is the customer's bank taking it back. This isn't just a number on a statement; it's real cash yanked from your operating account, impacting your cash flow instantly.

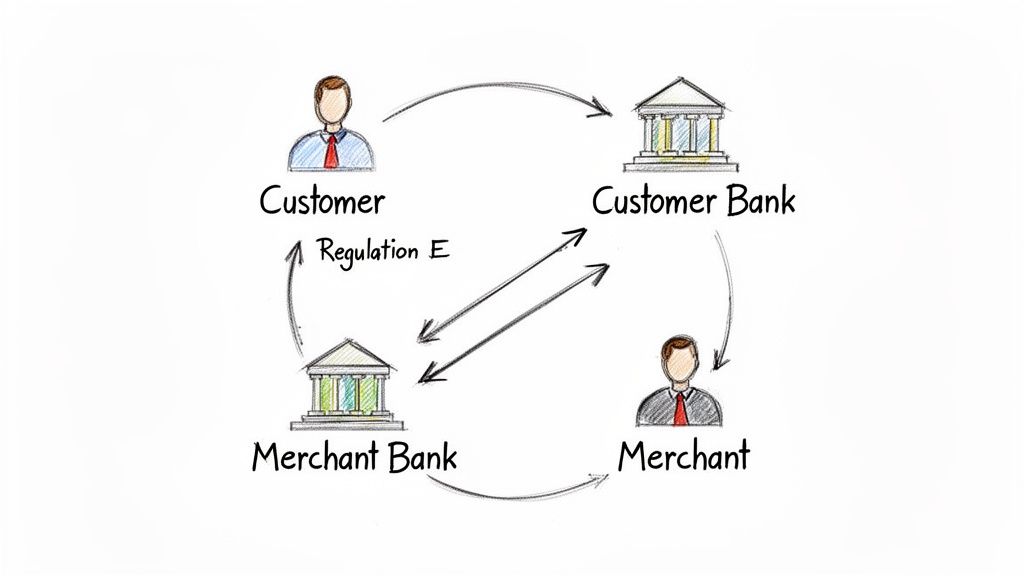

This whole process isn't just bank policy—it's backed by federal law. The main rule here is Regulation E, which is part of the Electronic Fund Transfer Act. This regulation lays out the ground rules for electronic payments and gives banks a clear procedure to follow when a consumer disputes a debit card transaction.

The Key Players in a Debit Card Dispute

Navigating a dispute is much easier when you know who’s who. Every debit card chargeback involves four main parties:

- The Customer (Cardholder): The person who originally made the purchase and is now claiming there's a problem with the charge.

- The Issuing Bank: This is the customer's bank (think Chase, Bank of America, etc.). They field the customer's complaint and kick off the chargeback process.

- The Acquiring Bank: This is your bank or payment processor. They're the ones who give you the merchant account to accept card payments and, unfortunately, the ones who have to pull the money from your account when a chargeback hits.

- The Merchant (You): Your business. You're the one who has to decide whether to accept the loss or invest the time and resources to fight the chargeback by proving the transaction was legitimate.

It all starts when your customer calls their bank. The bank then gives the customer a provisional credit, debits your account for the same amount, and sends you a notification letting you know you have a dispute on your hands.

Debit Chargebacks vs. Credit Card Disputes

On the surface, they seem the same, but a chargeback on a debit card and a credit card dispute are worlds apart, especially for your bottom line. The biggest difference is where the money comes from.

With a credit card dispute, the money is reversed from a line of credit. With a debit card chargeback, the money is pulled directly from your cash reserves—the actual funds sitting in your business bank account.

That immediate hit to your cash flow is what makes debit chargebacks so painful. There's no buffer. The money is gone the second the chargeback is initiated, and it stays gone unless you win the dispute.

For a clearer picture, here’s a quick breakdown of the fundamental differences.

Debit Card Chargeback vs Credit Card Dispute Key Differences

| Feature | Debit Card Chargeback | Credit Card Dispute |

|---|---|---|

| Fund Source | Direct debit from your business bank account. | Reversal against a line of credit. |

| Governing Regulation | Primarily Regulation E (EFTA). | Primarily Regulation Z (TILA). |

| Financial Impact | Immediate loss of cash from your operating funds. | Reduction in available credit; less immediate cash impact. |

Because your actual cash is on the line, mastering how to handle and—more importantly—prevent a chargeback on a debit card is crucial to keeping your business financially healthy and stable.

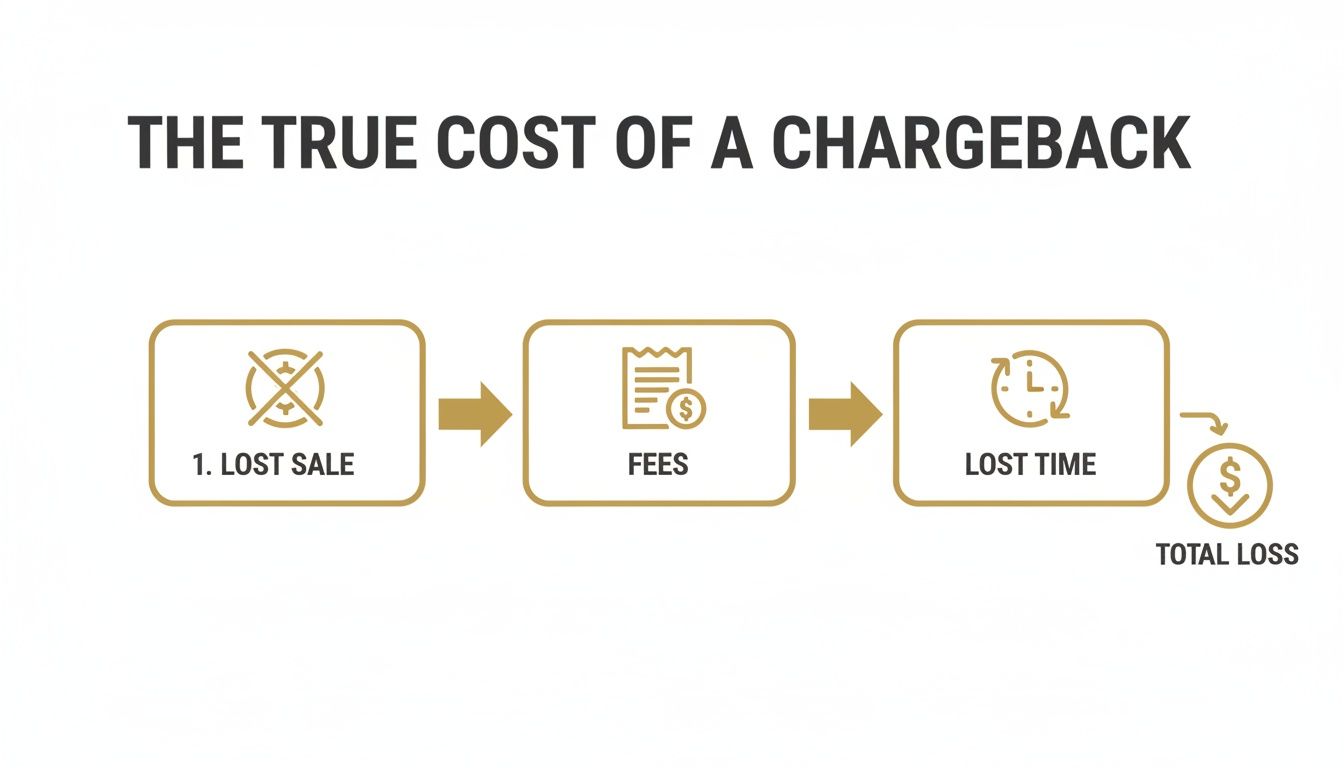

When a debit card chargeback hits your account, your first instinct is probably to look at the lost sale amount. But that’s just the tip of the iceberg. The real cost is a cascade of hidden fees, wasted time, and potential threats to your entire payment processing relationship.

Think of the initial transaction amount as a small leak in a boat. It's what you notice first. The real danger, however, comes from the water you don't see pouring in. For every single chargeback, your payment processor will slap you with a separate, non-refundable chargeback fee. This typically runs between $15 and $25, and you pay it whether you win or lose the dispute.

Beyond the Fees: The Hidden Operational Drain

The financial bleeding doesn't stop with the processor's fee. The next hit comes from the operational side of things. Your team has to drop everything to go into damage control mode, spending valuable hours on tasks that bring in zero revenue.

Suddenly, your staff is tied up with:

- Investigation: Someone has to become a detective, digging through order histories, shipping logs, and customer communication to figure out what went wrong.

- Evidence Gathering: This means compiling screenshots, delivery confirmations, terms of service agreements, and any other proof to build your case.

- Rebuttal Writing: A team member needs to write a clear, compelling rebuttal letter to challenge the bank's claim.

This is a massive drain on your resources. Every hour an employee spends fighting a dispute is an hour they aren't spending on marketing, improving your product, or helping legitimate customers.

The Escalating Threat of Online Transactions

This problem has exploded with the growth of ecommerce. For card-not-present (CNP) transactions—basically, any time a customer buys online without physically swiping their card—the risk of a dispute goes through the roof. The anonymous nature of online shopping makes it a breeding ground for both actual fraud and "friendly fraud," where a real customer disputes a charge they actually made.

The numbers are pretty staggering. In the U.S., the average chargeback is $110, but for every dollar lost to fraud, merchants actually lose a whopping $4.61 once you add up all the associated costs. It’s a global issue, too. Total chargeback values are projected to hit $33.79 billion in 2025 and climb to $41.69 billion by 2028. This isn't just a nuisance; it's a massive and growing threat to businesses. Read the full analysis on the true cost of chargebacks.

The Long-Term Risk to Your Merchant Account

Maybe the most dangerous cost of all is the damage done to your relationship with your payment processor. Every processor keeps a close eye on your chargeback ratio—the percentage of your transactions that turn into disputes. If this ratio creeps over their threshold, which is often around 0.9%, you get flagged as a high-risk merchant.

A high chargeback ratio sends a clear signal to banks and processors that there's a problem with your business model, customer service, or fraud controls. This can lead to severe consequences.

Once you're on their radar, processors might place a hold on your funds, demand a hefty cash reserve, or, in the worst-case scenario, shut down your merchant account completely. For an online business, losing the ability to process payments is a death sentence.

This is why managing every single chargeback on a debit card isn't just about winning back one sale. It’s about protecting the long-term health and survival of your entire operation. You can learn more about how to prevent disputes from impacting your ratio with alert services.

Navigating the Debit Card Chargeback Process

Getting a notification for a chargeback on a debit card can feel like a sudden storm—confusing, stressful, and a little overwhelming. But think of the process like a map. Once you understand the route and the key landmarks, navigating it becomes a series of predictable, manageable steps. This guide will walk you through the entire journey from a merchant's point of view, so you know exactly what’s happening and when.

The moment a customer disputes a transaction, a very specific process kicks off. It isn't instant; it's a sequence of events with strict timelines, involving several different players. And most importantly, it gives you a critical window to respond.

Stage 1: The Customer Initiates the Dispute

It all starts when your customer calls their bank—the issuing bank—to report an issue with a debit card transaction. They might claim the charge was fraudulent, they never received their order, or the product wasn't what they expected. The customer simply explains their side of the story.

At this point, you're completely out of the loop. This conversation happens entirely between the cardholder and their bank, so you won't even know a dispute has been filed yet.

Think of the bank as the customer's advocate in this first step. If the customer's claim fits one of the official chargeback reason codes, the bank will almost always move forward, giving the cardholder the benefit of the doubt.

Once the bank gives the customer's claim the green light, they take the next step, which is when you'll feel the financial impact.

Stage 2: The Bank Issues a Provisional Credit

After approving the dispute, the issuing bank gives the customer a provisional credit, putting the full transaction amount right back into their account. At the same time, the bank works through the card network (like Visa or Mastercard) to pull those same funds from your merchant account via your bank, the acquiring bank.

This is the moment a chargeback on a debit card hits your bottom line. The money is withdrawn from your business account immediately, and you’re also hit with a separate, non-refundable chargeback fee, typically between $15 and $25.

Stage 3: You Receive the Chargeback Notification

Your acquiring bank will now formally notify you that a dispute has been filed. This notification is your official call to action. It contains all the key details about the transaction and, most critically, the reason code for the chargeback. This code tells you exactly why the customer is disputing the charge.

The true cost of a chargeback goes far beyond just the lost sale. It’s a painful combination of the lost revenue, the penalty fees, and the time your team spends dealing with it.

This is why having your funds frozen can be so disruptive. A single dispute instantly multiplies your losses. If you've ever dealt with something similar, you know how frustrating it can be, which we cover in our guide to handling a Shopify payment hold.

Stage 4: Your Critical Response Window

As soon as you get that notification, the clock starts ticking. You have a specific timeframe—usually somewhere between 20 and 45 days, depending on the card network—to respond. This is your one chance to fight back, a process known as representment.

During this window, you have two options:

- Accept the Chargeback: If you know the chargeback is valid or you just don't have the evidence to fight it, you can accept it. The provisional credit becomes permanent, and the case is closed.

- Fight the Chargeback (Representment): If you believe the chargeback is unfair, you need to gather compelling evidence to prove your case. You’ll then submit this evidence packet to your acquiring bank.

Stage 5: The Final Decision and Outcome

Your evidence gets passed from your acquiring bank all the way back to the customer's issuing bank for review. The issuing bank acts as the final judge, weighing your evidence against the customer’s original claim.

If they rule in your favor, the chargeback is reversed, and the money is returned to your account. But if they side with the customer, the chargeback stands, the customer keeps the funds, and the case is closed—unless you’re willing to escalate to a costly and complex arbitration.

Why Your Customers File Debit Card Chargebacks

To stop a debit-card chargeback dead in its tracks, you have to get inside your customer's head. What makes someone call their bank instead of just reaching out to your support team for a simple refund? It’s never as simple as it seems, but the reasons almost always boil down to one of three things.

Think of it like this: one path is pure crime, another is an honest mistake (often yours), and the third—and most common—is a messy tangle of confusion, impatience, and misunderstanding. All three paths lead to the same destination: your lost revenue.

Category 1: True Fraud

This is the one everyone thinks of first. True fraud is exactly what it sounds like: a criminal gets ahold of a customer's debit card information and goes on a shopping spree in your store. The real cardholder eventually spots the charge, knows they didn't make it, and immediately calls their bank to report the theft.

In this scenario, the chargeback is 100% legitimate. Your customer is the victim, and you're the unfortunate collateral damage. You can't win this kind of dispute because the transaction was illegitimate from the start. Your only move here is to beef up your fraud prevention to catch these transactions before they're ever approved.

Category 2: Merchant Error

This category is all about slip-ups and miscommunications on your end. While you didn't mean for it to happen, these errors create a frustrating experience for the customer, sending them straight to their bank for help.

Some classic examples of merchant error include:

- Weird Billing Descriptors: Your business is "Artisan Goods LLC," but the charge shows up as "AG-LLC-PAYMENTS." The customer has no idea what that is and assumes the worst.

- Shipping Fumbles: The package is weeks late with no updates, arrives looking like it went through a blender, or gets delivered to the wrong state entirely.

- Website Glitches: A technical hiccup causes a customer to be billed twice for the same item.

More often than not, the real issue is that the customer just wasn't happy with the product or their experience. Taking steps to improve customer satisfaction is one of the best ways to get ahead of these kinds of disputes.

Category 3: Friendly Fraud

Welcome to the most frustrating, and fastest-growing, reason for chargebacks. Friendly fraud (sometimes called chargeback abuse) is when a real customer makes a perfectly valid purchase with their own card and disputes it anyway. There’s no stolen card here; the cardholder themselves is the one initiating the chargeback for a purchase they actually made.

But it’s not always malicious. More often than not, friendly fraud is born from simple human error, forgetfulness, or a misunderstanding of your policies.

Here’s what that looks like in the real world. A customer might file a chargeback because they:

- Forgot About the Purchase: They see the charge on their statement a month later and have no memory of what it was for.

- Have Buyer's Remorse: They regret buying something but find it easier to call their bank than to deal with your return process.

- Misunderstand a Subscription: They signed up for a free trial, forgot to cancel, and dispute the first real charge rather than asking you to stop it.

- A Family Member Made the Purchase: Their kid or spouse used the card, and they dispute the charge to avoid a family argument.

This "hidden crisis" is a huge drain on businesses. Friendly fraud is the culprit behind roughly 75% of all chargeback cases and makes up 45% of the total dispute volume across the globe.

In fact, eCommerce chargeback rates exploded by 222% from Q1 2023 to Q1 2024, showing just how fast this problem is spiraling. To make matters worse, for every dollar lost to the actual fraud, U.S. merchants end up losing $4.61 once you add in all the associated fees and operational costs. Digging into these motivations is the first step toward building a defense that works.

How to Fight a Debit Card Chargeback and Win

That chargeback notification you just received? It’s not a final verdict. Think of it as the starting bell for round one. This is your chance to step into the ring and formally challenge the dispute through a process called representment.

This is where you shift from defense to offense. Your job is to build a rock-solid case with compelling evidence proving the original transaction was completely legitimate. A half-hearted response just won't do; you need to present a clear, evidence-based argument that leaves the customer's bank with no other choice but to side with you.

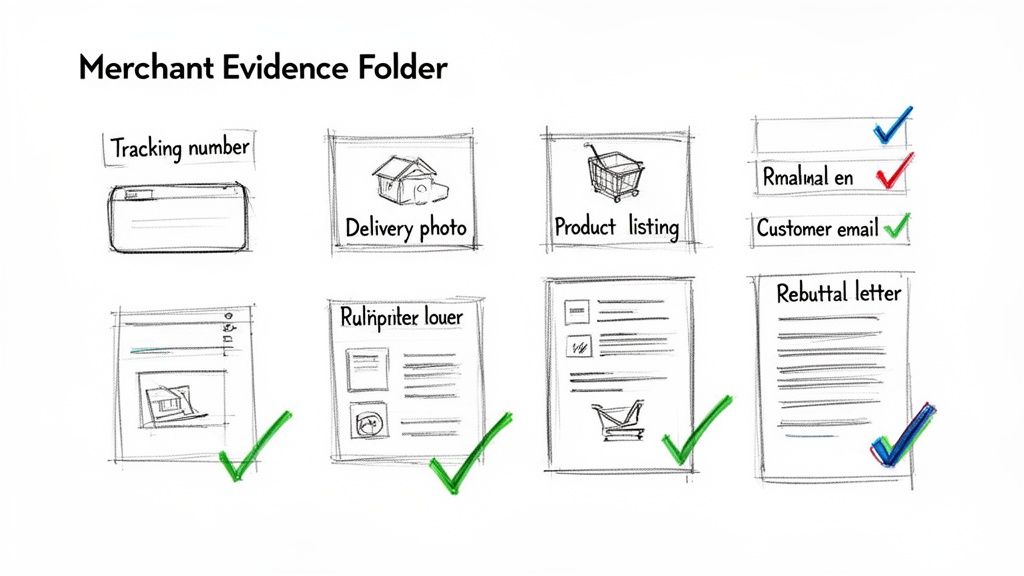

Gathering Your Compelling Evidence

The key to winning is understanding the "reason code" that comes with the dispute. This code tells you exactly why the customer is disputing the charge, and your evidence must directly poke holes in that specific claim. One-size-fits-all responses get tossed aside; tailored evidence wins.

For a "Product Not Received" dispute, your entire case hinges on one thing: proving you delivered the goods. Your shipping records are your best friend here.

- Tracking Information: Don't just list the number. Provide the full tracking link from a major carrier showing the journey and successful delivery to the customer's address.

- Delivery Confirmation: A clean screenshot from the carrier’s website showing the "Delivered" status, complete with the date, time, and city, is non-negotiable.

- Photo Evidence: If your carrier provides it, a photo of the package sitting on the customer's porch is the gold standard. It's tough to argue with a picture.

If the claim is "Product Not as Described," the focus shifts. Now you have to prove that what you sent is exactly what they ordered.

- Product Page Details: Send screenshots of the product page from the time of purchase. Circle the descriptions, specs, and photos that accurately show the item.

- Customer Communications: Dig up any emails, support chats, or social media messages. A conversation where the customer talks about the product without mentioning any issues is powerful proof.

- Order Confirmation: The original invoice or confirmation email is crucial. It shows the exact item, size, color, or model they chose, confirming there was no mix-up on your end.

To make this easier, we've put together a quick checklist for the most common dispute types.

| Dispute Reason | Required Evidence | Optional (but helpful) Evidence |

|---|---|---|

| Product Not Received | Tracking number with "Delivered" status & matching address. | Photo of delivery; any customer emails confirming receipt. |

| Product Not as Described | Screenshots of the product page showing accurate descriptions & images. | Customer service chats/emails discussing the product; order confirmation. |

| Fraud/Unauthorized | AVS/CVV match results; IP address of the order vs. customer's location. | Past order history from the same customer/address; login records. |

| Canceled Recurring | Proof of a clear cancellation policy; customer's agreement to terms at checkout. | Records of the customer using the service after the alleged cancellation date. |

Having these documents ready will dramatically speed up your response time and increase your odds of winning.

Structuring Your Rebuttal Letter

Once your evidence is collected, you need to present it in a formal rebuttal letter. This isn’t a place to vent or tell a long story. The bank agent reviewing your case is looking at dozens of others, so make their job easy. Get straight to the point.

Your rebuttal letter is the cover sheet for your evidence. Its only purpose is to guide the reviewer through your proof and lead them to the undeniable conclusion that the charge was valid.

A winning letter follows a simple, professional formula:

- Introduction: Right away, state the case number, transaction date, and amount. Open with a clear statement like, "We are disputing this chargeback because our records confirm the item was successfully delivered on [Date]."

- Evidence Summary: This is the heart of your letter. Use a simple bulleted list to itemize your proof, referencing each document you’ve attached. For example: "Proof of delivery from FedEx (See Exhibit A)" or "Screenshot of product page description (See Exhibit B)."

- Conclusion: Wrap it up with a polite but firm request. Simply restate that the evidence validates the transaction and ask for the chargeback on a debit card to be reversed.

This straightforward approach turns a stressful situation into a manageable checklist. By carefully matching the right evidence to the reason code and presenting it cleanly, you give yourself the absolute best shot at keeping your hard-earned revenue.

Preventing Chargebacks with Proactive Alerts

Knowing how to fight a chargeback on a debit card is important, but the best strategy is to stop them before they even start. Instead of just reacting after the damage is done, you can get ahead of disputes with proactive chargeback alerts.

Think of these alerts as a smoke detector for your merchant account. Before a small customer complaint turns into a full-blown chargeback fire, an alarm goes off. This gives you a critical window to put it out.

How Chargeback Alerts Work

This early-warning system is powered by the card networks themselves, primarily Visa and Mastercard.

- Visa's Rapid Dispute Resolution (RDR): This system catches disputes from Visa cardholders at the source, giving you a chance to resolve them before they escalate into formal chargebacks.

- Mastercard's Consumer Dispute Resolution Network (CDRN): Works much like Visa's RDR, flagging potential disputes from Mastercard users the moment they contact their bank.

Here’s how it unfolds: a customer calls their bank to question a charge. Instead of that inquiry immediately starting the formal chargeback process, these networks send you an instant notification.

This alert opens up a golden opportunity—usually between 24 and 72 hours—to solve the problem directly. You can issue a full refund right away. Once the customer is refunded, the bank sees the issue is settled and the dispute simply goes away. It never becomes an official chargeback on your record.

That one simple action lets you sidestep the entire messy chargeback process. You dodge the non-refundable fees, protect your chargeback ratio, and avoid all the time and effort of gathering evidence and writing rebuttal letters.

The Impact of a Proactive Strategy

Switching from a reactive to a preventative mindset makes a huge difference, especially as dispute volumes climb. Global chargeback cases are expected to reach a staggering 337 million by the end of 2025—that's a 27% jump from 2022.

For a high-volume business, even a "low" 0.65% chargeback rate can mean thousands in lost revenue. And if you cross that dreaded 0.9% threshold, you’re looking at serious penalties from your payment processor. Early alerts are your best defense to keep your rates safely in the green.

By integrating with an alert platform, you can put this whole prevention process on autopilot. An alert comes in, a refund is issued based on rules you set, and the threat is neutralized before it can hurt your business.

Beyond alerts, merchants can also explore advanced tools like a biometric-first approach to reduce fraud risk, which adds another layer of security to stop fraudulent transactions in their tracks. Adopting this proactive stance is the key to keeping your merchant account healthy and protecting your bottom line.

Frequently Asked Questions

Let's face it, dealing with debit card chargebacks can feel like navigating a maze. You've got questions, and we've got straightforward answers based on years of experience in the trenches.

Can a Chargeback on a Debit Card Be Reversed?

Absolutely. A chargeback is just the first step in a formal conversation—it's not the final word. You have every right to fight it.

This process is called representment. If you can provide solid evidence showing the transaction was legitimate and you held up your end of the deal, the bank can reverse the chargeback. When you win, the money is returned to your account.

What Is the Time Limit for a Debit Card Chargeback?

The clock starts ticking for everyone, but the timelines aren't the same. Customers generally have up to 120 days from the transaction date to file a dispute. In some cases, like with undelivered services, that window can be even longer.

Your response window, however, is much tighter. Once a chargeback lands in your lap, you typically only have 20 to 45 days to build your case and submit your evidence. Miss that deadline, and you automatically lose.

Can I Get My Chargeback Fees Back if I Win?

This is a tough one, but the short answer is no. That chargeback fee, usually between $15 and $25, is an administrative cost your acquiring bank charges just for processing the dispute.

It's non-refundable, no matter the outcome. You pay it if you win, you pay it if you lose. This is exactly why a proactive prevention strategy is so critical—it's always cheaper to stop a dispute before it happens. You can get support and learn more about prevention right here.

Stop losing revenue to preventable disputes. Disputely integrates with Visa RDR and Mastercard CDRN to give you a 24-72 hour window to refund a customer before a dispute becomes a costly chargeback. Protect your merchant account and keep your hard-earned money by visiting https://www.disputely.com to see how it works.