The Merchant's Guide to Credit Card Pre Authorization

Ever wonder what a "pending charge" on your credit card statement really is? Most of the time, it's a credit card pre-authorization—a temporary hold a merchant places on your card to make sure it's legitimate and has enough funds to cover a future purchase.

Think of it less like an actual charge and more like a financial reservation. It’s a smart way for businesses to secure the funds before a service is delivered or a final bill is calculated, protecting them from the headache of a declined payment after the fact.

Understanding the Core Concept of Pre-Authorization

The best analogy for a pre-auth is making a dinner reservation. You call the restaurant, and they hold a table for you. They haven't charged you for dinner yet, but they've guaranteed your spot. A pre-authorization works the same way for a customer's credit line; it "reserves" a specific amount of their available credit without actually taking a dime.

At its core, this is a crucial safety check for any merchant. It's a quick, automated handshake between your business, the customer's bank (the issuer), and the card network (like Visa or Mastercard). The entire point is to get a simple "yes" or "no" on whether the customer can actually pay before you hand over the rental car keys or check them into their room.

The Hold vs. The Final Charge

It's easy to mix up a temporary hold and a final charge, but they are two very different steps in the payment process. The pre-authorization is just the beginning. The final charge, which is technically called a "capture," is when you actually tell the bank to move that reserved money into your account.

This two-step dance gives merchants a ton of flexibility, which is especially useful when the final bill isn't set in stone.

To make this crystal clear, let's break down the fundamental differences between a temporary hold and a completed payment. This table gives you a clear view of the transaction lifecycle.

Pre Authorization Hold vs. Final Charge

| Aspect | Pre-Authorization (Hold) | Final Charge (Capture) |

|---|---|---|

| Purpose | Verifies card validity and reserves funds. | Completes the sale and transfers the money. |

| Customer View | Shows up as a "pending" transaction. | Appears as a posted, final transaction. |

| Impact on Funds | Temporarily reduces available credit/balance. | Permanently deducts funds from the account. |

| Action | A temporary hold is placed on the funds. | The reserved funds are moved to your account. |

Essentially, the hold is the question, and the capture is the answer.

A credit card pre-authorization is your way of asking, "Is this customer good for the money?" before you commit. It’s a low-risk method to guarantee a smooth and secure transaction for everyone involved, saving you and your customer from the frustration of a payment that just won't go through.

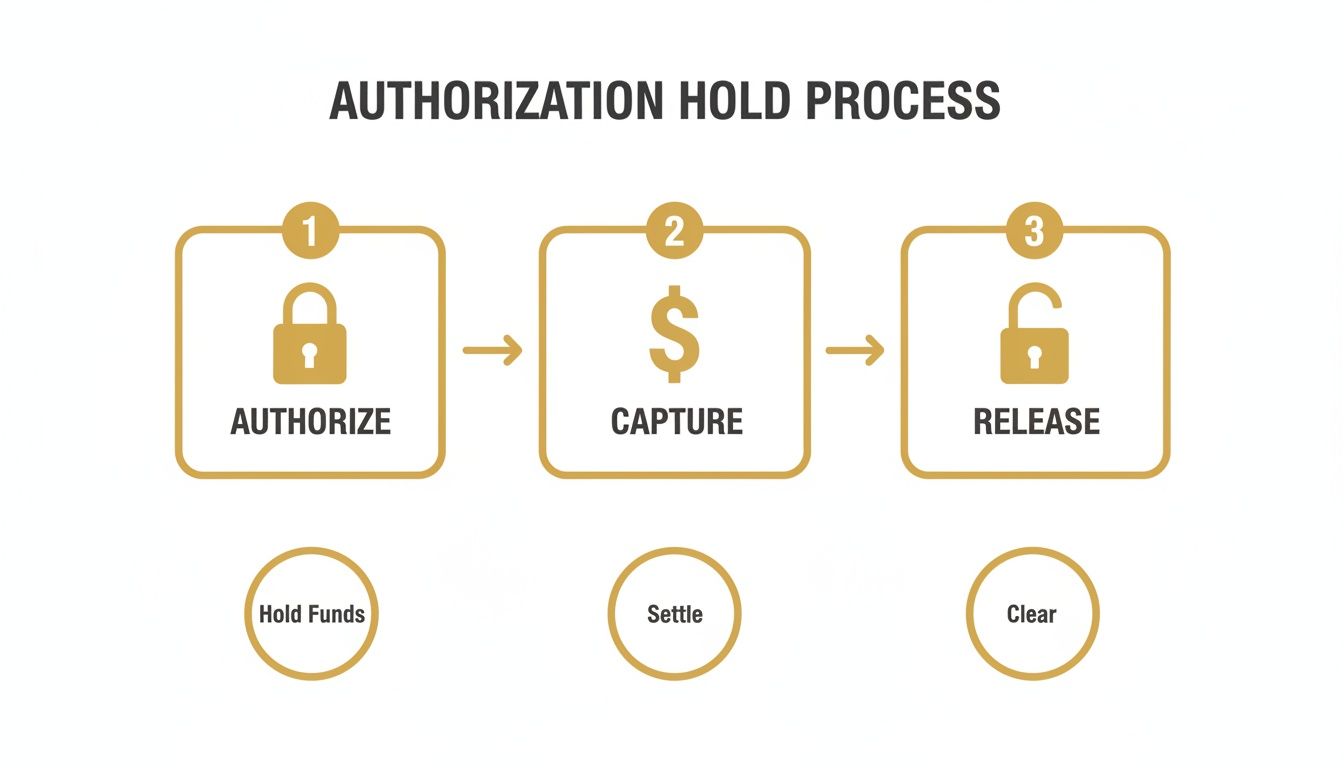

The Lifecycle of a Pre-Authorization Hold: From Hold to Final Charge

Every pre-authorization has a clear beginning, middle, and end. Grasping this three-part journey is key to managing your cash flow and, just as importantly, keeping your customers happy and informed.

Think of it like reserving a table at a restaurant. First, you put your name down (the authorization). Then, you enjoy your meal and pay the bill (the capture). Finally, the "reserved" sign is taken off your table (the release). Let's break down how this works for a credit card transaction.

Stage 1: The Authorization

This is where it all begins. A customer gives you their card, and your payment system sends a quick message to their bank. The request is simple: "Can you please set aside a certain amount of money for a potential charge?"

The customer's bank then does a quick check. Does the card exist? Is it stolen? Does the customer have enough available credit? If everything looks good, the bank puts a temporary hold on the funds. No money has actually moved—it's just been earmarked for you. It’s the digital equivalent of putting a sticky note on a stack of cash that says, "Reserved for this merchant."

Stage 2: The Capture

The capture is the moment you officially collect the money. Once the service is complete or the final bill is calculated, you send a second message to the bank, telling them to "capture" the funds you had them hold. You can capture the full pre-authorized amount or just a portion of it.

For instance, a hotel might pre-authorize $500 at check-in to cover the room and potential incidentals. If the final bill is only $450, that's the amount they'll capture.

The capture is when the transaction goes from "pending" to "posted." It's the critical step that converts the temporary hold into a real charge, moving money from the customer’s account into yours.

This is the action that gets you paid. On the customer's end, they'll see the charge finalized on their statement.

Stage 3: The Release or Void

Finally, the hold needs to be cleared. This happens in one of two ways, depending on how the transaction played out.

Release after a Capture: If you captured less than the original hold amount, the bank releases the leftover funds. In our hotel example, after capturing the $450 bill, the bank would release the remaining $50 hold, freeing up that credit for the customer.

Void or Expiration: What if the transaction is cancelled, or you simply never capture the payment? In that case, the entire hold has to go. You can actively void the authorization, which tells the bank to release the funds right away. If you don't do anything, the hold will eventually just expire on its own, usually in about 5-7 business days, though this can vary.

Handling this last step correctly—by promptly capturing what you're owed or voiding what you're not—is crucial. It gives customers their buying power back faster and avoids any confusion or frustration.

How Authorization Holds Impact Your Business and Your Customers

A credit card pre-authorization means two very different things depending on which side of the transaction you're on. For your business, it’s a smart way to check that a customer can actually pay for something. But for your customer, it’s just a confusing "pending" charge that ties up their money.

Getting a handle on this dual reality is crucial. It’s the key to heading off customer confusion, explaining your process clearly, and avoiding the kind of misunderstandings that turn into frustrating disputes.

This simple flowchart lays out the entire journey, from the initial hold to the final payment.

As you can see, the process always starts by locking the funds (Authorize), then collecting the actual amount owed (Capture), and finally, freeing up any leftover cash (Release).

The Merchant Perspective: A Safety Net

From a business owner’s point of view, a pre-authorization is all about managing risk. Think of it as your insurance policy against getting stuck with an unpaid bill after you’ve already delivered a service or product.

It gives you the power to:

- Confirm Funds: Instantly verify that the customer's card is legitimate and has enough money available before you commit your time or inventory.

- Secure Payment: Essentially "reserve" the estimated total, guaranteeing the money will be there when you're ready to charge the final amount.

- Reduce Declines: Massively cut down on the risk of a payment failing later, which is a lifesaver in industries where final costs can change, like hotels or rental agencies.

The Customer Perspective: A Temporary Inconvenience

Your customer doesn't see any of that behind-the-scenes security. All they see is a chunk of their available credit or bank balance disappearing, even though they haven't technically paid you yet. If you don't explain what's happening, it can be pretty alarming.

To a cardholder, a pending authorization looks and feels like a real charge. This perception gap is the primary source of friction, often leading them to believe they've been overcharged or billed incorrectly.

This hold eats into their spending power for other things until it's released, which can sometimes take several business days. If the hold is much higher than the final charge, it’s a recipe for frustration and can easily trigger a dispute.

Being upfront and transparent about your hold policies is the best way to keep customers happy. It’s also wise to keep an eye on regulatory trends, like the ongoing CFPB investigation into credit card practices, to ensure you're always treating customers fairly.

For those wanting to get into the nitty-gritty of managing these holds, you can learn more here about placing a hold on a customer's card with Shopify: https://disputely.com/shopify-hold.

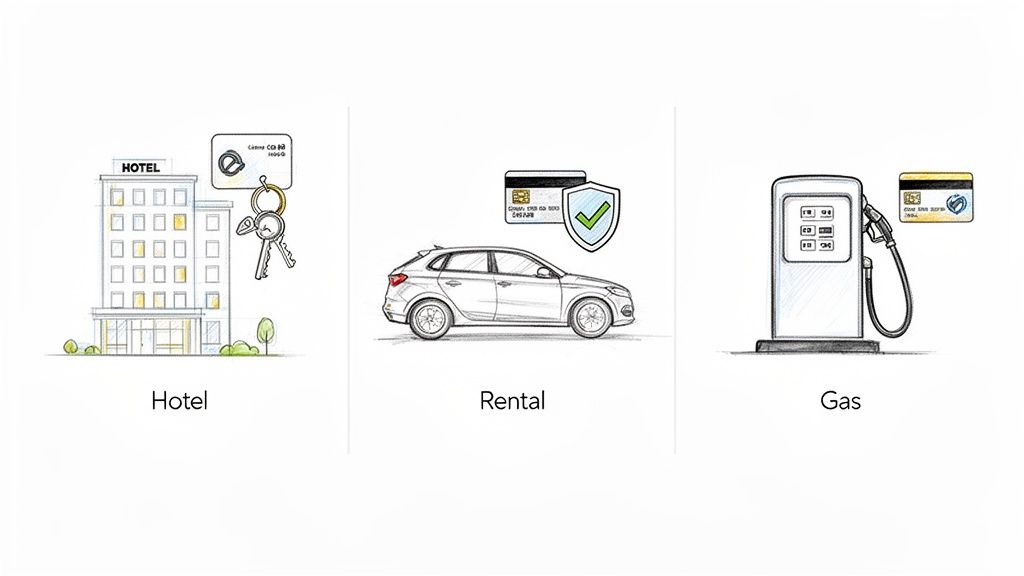

Why Certain Industries Depend on Pre-Authorizations

For some businesses, a credit card pre-authorization isn't just a handy feature—it’s the entire foundation of their payment process. Think about it: many industries deal with a unique problem where the final cost of a service is a complete unknown when the customer first walks in. This makes charging someone upfront impossible and opens the door to huge financial risks.

Pre-authorizations are the perfect solution. By placing a temporary hold on a customer's funds, these businesses can essentially guarantee they’ll get paid for a bill that hasn't even been calculated yet. It’s a vital financial safeguard against fraud, unpaid services, and even potential damage to their assets. For any business where the final bill is a moving target, this is a non-negotiable part of the playbook.

Managing Variable Final Costs

The most common reason you’ll see a credit card pre-authorization is in businesses where the final bill is anyone's guess. Hotels are the classic example. When you check in, the front desk has no clue if you're going to order late-night room service, empty the minibar, or book a spa treatment.

To cover all their bases, the hotel places a hold on your card for the room rate plus an estimated amount for these "incidentals." This simple step ensures that when you check out, the funds to cover your entire stay are already ring-fenced and ready to go. Without that hold, the hotel is just hoping you have enough left on your card to pay for those extra mojitos.

This same logic is at work in plenty of other places:

- Restaurants and Bars: It’s how they keep a "tab" open. The hold lets you order throughout the night without swiping your card every time, and the final amount is captured when you're ready to leave.

- Online Grocery Orders: Ever notice the initial charge is slightly different from the final one? The store authorizes an estimate when you place the order, then captures the exact amount after weighing your produce and accounting for any substitutions.

A pre-authorization provides a flexible financial cushion. It allows merchants to secure an estimated amount upfront, then adjust and capture the precise final total once the service is complete, eliminating guesswork and reducing payment failures.

Securing High-Value Assets

Another crucial job for pre-authorizations is protecting expensive assets that customers borrow. Car rental agencies are the poster child for this. When you drive off the lot, you’re in control of an asset worth tens of thousands of dollars. The agency needs a way to protect itself from damage, late fees, or an empty gas tank on return.

That’s why they place a hefty pre-authorization hold on your card, often for several hundred dollars. This hold acts as a security deposit. It gives the rental company immediate financial recourse if the car comes back needing repairs or a fill-up. It's an absolutely essential practice for managing the risks baked into the rental business model.

How Pre-Authorizations Can Backfire into Disputes and Chargebacks

While pre-authorizations are a fantastic way to manage risk, they can become a customer service nightmare and a direct pipeline to disputes if you're not careful. This isn't usually about fraud; it's almost always about confusion. A customer glances at their online banking app, sees a pending charge they don't recognize or that looks wrong, and their first move is often to call the bank. Just like that, you’re dealing with a chargeback.

This friction almost always points back to a few simple, avoidable mistakes. The most common culprit? A pre-authorization hold that just sits there, long after the customer has paid and left. Another frequent issue is a duplicate authorization—a quick glitch or simple human error slaps two holds on an account for one purchase, making the customer think they've been double-charged. These are small operational hiccups that create massive headaches.

From a Simple Hold to a Costly Dispute

The journey from a standard hold to a full-blown chargeback starts with a communication gap. Let's walk through a common scenario. A customer rents a car, and the agency places a $500 hold on their card for incidentals. The final bill comes to just $150. But if the agency is slow to capture that final $150 and release the rest, the customer sees that $500 pending charge for days, eating up their available credit.

From their perspective, their money is trapped. That feeling creates stress and kills trust, making them far more likely to hit the "dispute" button.

Here are the most common things that set customers off:

- Lingering Holds: The authorization isn't captured or voided right away, leaving the customer's funds in limbo.

- Shockingly High Holds: The amount you pre-authorize is way more than the final bill, which naturally looks like an error.

- The Element of Surprise: The customer was never told a temporary hold would be placed on their card in the first place.

When a customer is surprised by a pending charge, they don't see a "temporary hold"—they see a mistake. This perception gap is the single biggest driver of authorization-related chargebacks.

The Hidden Costs of Sloppy Authorization Management

These disputes do more than just cost you the transaction amount. Every chargeback eats away at the health of your business. They drive up your dispute ratio, which can land you in hot water with your payment processor and even put your merchant account at risk. Getting your payment flow right isn't just about providing good service; it's a fundamental part of staying in business.

What's really surprising is that even though authorization rates are a key metric tied directly to revenue, roughly 40% of businesses don't even track them. Even a small dip in your authorization rate can lead to a huge loss in profit over time. This makes managing pre-authorizations a top priority.

Effectively managing these holds is your first and best defense in a smart chargeback prevention plan. At Disputely, we've seen firsthand how proactive alerts and clear communication can stop these issues before they ever turn into a costly dispute.

Best Practices for Managing Authorization Holds

If you handle authorization holds smartly, you can turn what might have been a messy dispute into a smooth customer experience. A few simple operational tweaks can make a massive difference in reducing confusion, protecting your merchant account, and actually building customer trust. It really all boils down to two things: clarity and speed.

The single most important thing you can do is be upfront about your hold policies. A credit card pre-authorization should never come as a surprise. Make sure your policies are clearly stated at the checkout counter, on your website, and in any confirmation emails. When customers know what to expect, they don't panic when they see a pending charge.

Communicate Clearly and Proactively

Most disputes born from pre-authorizations start with simple confusion. A customer sees a hold they don't recognize or understand, assumes it's an error, and calls their bank. You can head this off entirely with proactive communication.

Here’s how to build a solid communication plan:

- Point of Sale Disclosures: Get your staff in the habit of verbally explaining hold policies. This is especially vital for businesses like hotels or car rentals where the final bill can change.

- Digital Messaging: Weave a simple, easy-to-understand note about authorization holds into your booking confirmations, email receipts, and website FAQs.

- Hold Amount Logic: Briefly explain why the hold might be higher than the initial cost. Mentioning that it covers potential incidentals goes a long way.

Giving someone a quick heads-up transforms a potentially alarming bank statement entry into just another part of the process.

Key Takeaway: An informed customer is your best defense against authorization-related disputes. Transparency isn't just about good service; it's a fundamental risk management tool that stops chargebacks before they even start.

Act with Urgency and Precision

Once you’ve nailed your communication, the next piece of the puzzle is operational efficiency. A pre-auth that hangs around on a customer's account for too long is a major source of frustration. Speed is your friend here.

Stick to these two golden rules to keep your payment process clean and your customers happy:

- Capture Charges Promptly: The moment you know the final transaction amount, capture the payment. This action tells the customer’s bank to finalize the charge and begin releasing any excess funds from the hold.

- Void Unused Authorizations Immediately: If a customer cancels their booking or decides to pay with cash, don't just wait for the hold to expire naturally. You need to actively void the pre-authorization. This tells the bank to release the funds right away.

By promptly capturing or voiding every hold, you’re minimizing the time your customer’s money is tied up. It's a simple sign of respect that dramatically lowers your dispute risk. Many modern payment systems can even help automate these steps, giving you a safety net to manage your payment lifecycle without letting anything fall through the cracks.

Answering Your Top Questions About Pre-Authorizations

Even after you've got the basics down, you're bound to have a few nagging questions. Let's tackle some of the most common ones merchants ask about credit card pre-authorizations to clear up any lingering confusion.

How Long Does a Pre-Authorization Hold Last?

Typically, you can expect a pre-authorization hold to stick around for 5 to 7 business days. But that’s just a rule of thumb. The actual duration can swing quite a bit depending on the card network (think Visa vs. Mastercard) and your line of business.

For example, hotels and car rental agencies often see holds that last up to 30 days. The best move is always to act fast. As soon as the final bill is settled, either capture the payment or void the hold. It’s a simple step that keeps your customers happy by freeing up their available credit sooner.

What's the Difference Between Authorization and Settlement?

Think of authorization as the initial handshake. It's the moment the customer's bank gives you a thumbs-up, confirming the card is valid and the funds are available, and then places a temporary hold on that amount. It's important to remember no money has actually changed hands yet.

Settlement is when you actually "capture" the funds. This is the step that finalizes the sale and moves the money from the customer's account into yours. Simply put, authorization reserves the money; settlement collects it.

The real difference comes down to the movement of money. An authorization is just a temporary hold on credit, while a settlement is the final transfer of cash. Nailing this distinction is key to managing your payments correctly.

Can a Pre-Authorization Be Canceled?

Yes, absolutely. And you definitely should cancel it when necessary. This process is called "voiding" the transaction. When you void a pre-auth, you're sending a direct message to the customer's bank to release the hold on their funds.

This is the right thing to do if a customer cancels their booking or decides to pay with cash instead. If you do nothing, the hold will eventually time out and expire, but voiding it is much better for the customer. It frees up their money right away and helps you avoid any frustration that could lead to a dispute.

For more detailed help on navigating specific payment issues, you can always find answers in our support center.

At Disputely, we help you stop chargebacks before they happen by resolving disputes the moment they arise. Our automated alert system gives you the power to refund a customer and prevent a damaging chargeback from ever hitting your merchant account. Learn how Disputely can protect your business.