Credit Card Processing High Risk: credit card processing high risk tips

When you hear the term “high-risk credit card processing,” it’s easy to think of it as a penalty. But that’s not really what it is. It’s more like a specialized insurance policy for businesses that, by their very nature, face a higher chance of financial hiccups like chargebacks or fraud.

Think of it like insuring a high-performance race car versus a standard family sedan. Both need insurance, but the race car's policy accounts for a completely different set of risks. This specialized approach ensures that businesses in more volatile industries can still accept credit card payments, just with the right safety measures in place.

What Is High Risk Credit Card Processing?

At its heart, high-risk credit card processing is simply a classification that acquiring banks and payment processors assign to merchants they see as a greater financial liability. This isn't a moral judgment on your business. It's a pragmatic risk assessment based on hard data from your industry and the specifics of your business model.

A low-risk merchant is like a borrower with a perfect credit score and a steady, predictable job—a safe bet. A high-risk business, however, might be more like a freelancer with a fluctuating income. The loan is still very possible, but the lender is going to build in some extra safeguards to protect themselves.

Why Processors Care So Much About Risk

Payment processors work on razor-thin margins. When a customer disputes a charge and files a chargeback, the processor is often on the hook for that money until it’s all sorted out. If a merchant in a high-risk industry suddenly shuts down, the processor could be left holding the bag for tens of thousands of dollars in unresolved chargebacks.

That’s precisely why the "high-risk" category exists. It activates a different playbook with rules and pricing designed to shield the processor from that potential fallout. These measures typically include:

- Higher processing fees to build a buffer against potential losses.

- More rigorous underwriting to deeply analyze a business’s financial health and stability.

- A rolling reserve, where a small percentage of your revenue is held back temporarily to cover any future chargebacks.

This system is what makes it possible for businesses in industries like travel, subscription boxes, and nutritional supplements to operate and grow. To dig deeper into the world of payment solutions for all types of businesses, the folks at payment processing experts offer some great insights.

Getting a "high-risk" classification isn't a dead end—it's just a different route to the same destination. It means you need to be more diligent, and your processor needs to provide more security, creating a partnership focused on managing financial risk together.

The Growing Tsunami of Chargebacks

The need for solid high-risk processing has never been more critical. We're seeing an explosion in global chargeback volumes, which is putting incredible strain on merchants, particularly those running subscription services or selling directly to consumers.

Industry data shows that worldwide chargeback volume is expected to jump from 261 million transactions in 2025 to a massive 324 million by 2028. That's a 24% increase in just three years, signaling a major challenge for businesses trying to protect their revenue.

Why Your Business Might Get Labeled "High Risk"

Payment processors don't just throw a "high-risk" label on businesses for no reason. It’s a calculated decision, almost like how a home insurer looks at a house in a hurricane zone. They aren't passing judgment on the homeowner; they're simply pricing in the very real environmental risks.

The classification boils down to two main things: your industry and how you operate your business. Some industries get flagged right away because of a long history of chargebacks or tight government regulations. On the other hand, some business practices, no matter the industry, just create more financial uncertainty for the processor.

Figuring out where your business stands is the first step. It's not about changing your core business, but about understanding the processor's perspective so you can prepare, negotiate, and protect your account.

It Might Just Be Your Industry

Some industries are almost always considered high-risk for credit card processing high risk accounts. This isn’t a knock on their legitimacy. It’s simply because the nature of their business opens the door to more disputes, fraud, or regulatory headaches.

Take the travel industry, for instance. People often book expensive vacations months in advance. If that airline cancels the flight or the cruise changes its itinerary six months down the road, you can bet a chargeback is coming. That long delay between payment and when the service is actually delivered is a huge window of risk for the processor.

Here are a few other industries that often land on the high-risk list:

- Nutraceuticals and Supplements: This space is constantly under the microscope for product claims and heavily relies on subscription models, which are a magnet for customer disputes.

- Subscription Services: Recurring billing is the number one cause of "friendly fraud," where customers simply forget they signed up for something and dispute the charge.

- Travel and Hospitality: Think big-ticket purchases and long waits for fulfillment. This combination naturally leads to more cancellations and chargebacks.

- Adult Entertainment: Acquiring banks see "reputational risk" here, and the industry historically deals with a higher number of customer disputes.

- Online Gaming and Gambling: These businesses operate under a complex web of regulations and are constant targets for fraud and chargebacks.

At the end of the day, a processor is looking for predictability. An industry with shifting regulations, a lot of returns, or a business model built on recurring payments throws a wrench in the works. Standard, low-risk processing just isn't built to handle that kind of unpredictability.

Your Business Model Can Be a Red Flag, Too

Even if you're not in a "risky" industry, how you run your business can get you classified as high-risk. Underwriters are trained to spot operational triggers that are statistically linked to higher financial losses for the payment processor.

Here are the most common operational red flags:

- High Average Ticket Size: Any transaction regularly over $500 makes processors nervous. If a chargeback happens, the financial hit is that much bigger.

- Card-Not-Present (CNP) Transactions: Selling online or over the phone is naturally riskier. It's much harder to confirm the person using the card is the actual owner, which makes CNP a playground for fraudsters.

- Recurring Billing Models: As we touched on, subscriptions are a headache. They’re notorious for high chargeback rates from customers who forgot they subscribed or found it too hard to cancel.

- International Sales: Selling globally sounds great, but it adds layers of complexity—currency conversions, messy shipping logistics, and a tangle of different banking laws all ramp up the risk.

- Poor or No Credit History: If the business owner has a shaky personal credit history, or if the business is brand new with no payment processing track record, it’s an automatic red flag. There’s no data to prove you’re financially stable.

To help you see how this all connects, we’ve put together a table showing how these risk factors play out in the real world for different industries.

High Risk Industries and Their Core Risk Factors

This table breaks down common high-risk industries, the main reason processors classify them as such, and a practical example of the risk involved.

| Industry | Primary Risk Factor | Example Scenario |

|---|---|---|

| Supplements | Recurring Billing & Claims | A customer forgets about their monthly auto-ship and files a chargeback, claiming they never authorized the recurring payment. |

| Travel Agency | High-Ticket & Future Delivery | A family books a cruise nine months out. The cruise line later changes the itinerary, leading the family to dispute the large charge. |

| Online Coaching | Intangible Goods & High Value | A client pays for a high-ticket coaching program but feels they didn't get the promised results and disputes the charge months later. |

| CBD Products | Regulatory Uncertainty | A processor's banking partner decides to stop supporting CBD merchants due to changing laws, leaving the merchant without a payment solution. |

As you can see, the "high-risk" label often comes from factors that are just a normal part of doing business in these sectors. The key isn't to stop doing them, but to manage the associated risks proactively.

How Processors Evaluate and Price High-Risk Accounts

When a payment processor looks at your business, think of them less as a service provider and more as a bank underwriter sizing up a complex loan. They aren't just looking for a single red flag; they're piecing together a complete risk profile to predict how your business will behave financially down the road. This isn't about penalizing you—it's about them understanding the liability they're taking on.

This underwriting process is the absolute heart of what credit card processing high risk services are all about. The processor’s main goal is to answer one critical question: what’s the chance this merchant will rack up more chargebacks and fraud than their revenue can cover? Their entire pricing model and the terms you get are built around the answer.

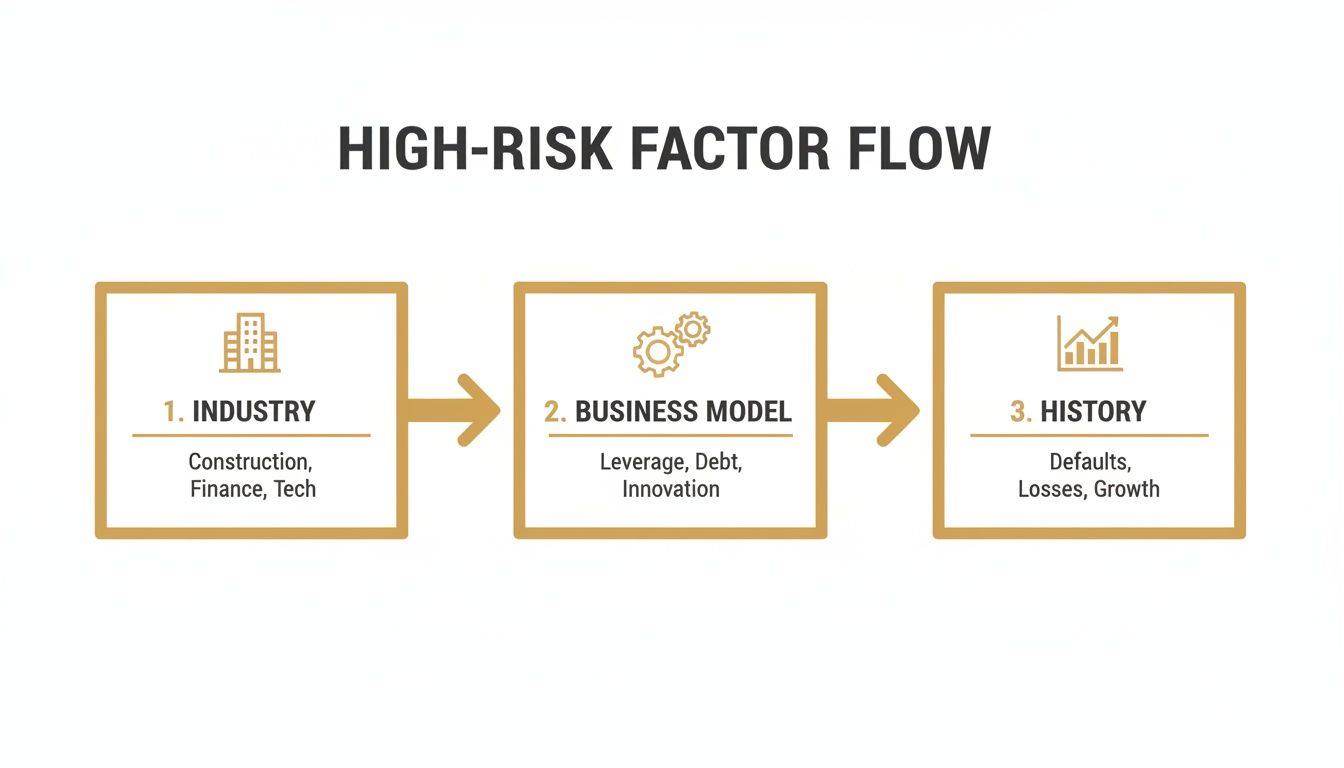

Building Your Business's Risk Profile

The first step is a deep dive into your business fundamentals. Underwriters meticulously comb through your industry, your specific business model, and your financial track record to get a full picture. Every piece of information helps them put a number on the potential for future losses.

This flowchart shows you exactly what they're looking at.

As you can see, the assessment starts broad with your industry and gets more and more specific, drilling down into your actual operational history. It’s a cumulative process.

But they aren't just hunting for problems; they're also looking for signs of stability. A business with clean, organized books and a transparent way of operating is a much more attractive partner, even if it’s in a high-risk industry. Processors need to see that you have a solid handle on your finances and a clear plan for managing disputes.

To build this profile, they need to see the proof. You’ll be asked for specific documents that act as evidence of your business's health and history.

Here’s what you’ll typically need to provide:

- Recent Bank Statements (3-6 months): These show your real-world cash flow, average daily balance, and any overdrafts or NSF events, which are major warning signs.

- Processing History (3-6 months): If you've taken cards before, these statements are crucial. They reveal your sales volume, average transaction size, and most importantly, your chargeback ratio.

- Business Formation Documents: Your articles of incorporation or LLC registration prove that your business is a legitimate, legally recognized entity.

- Supplier Agreements: For anyone selling physical goods, these show you have a reliable supply chain and can actually fulfill the orders you take.

Think of it this way: an underwriter's job is to tell a story about your business using data. Your processing history is the most important chapter, as it provides hard evidence of how you've handled payments in the real world. A low chargeback ratio can make a world of difference.

Why High-Risk Pricing Is Different

Once your risk profile is built, the processor sets up a pricing structure to match it. Those higher fees you see with high-risk accounts aren't random penalties. They are carefully calculated measures designed to create a financial safety net for the processor.

The two biggest factors in high-risk pricing are the processing rates themselves and something called a rolling reserve. Each one serves a very specific purpose in protecting the processor from taking a loss. This is why it pays to understand the different pricing models available; check out our guide on credit card processing fees to see what your options might be.

Here’s a quick breakdown of how it works:

Higher Transaction Fees: A standard, low-risk merchant might pay something like 2.9% + 30¢ per transaction. A high-risk business, on the other hand, could be looking at rates from 3.5% to 5.0%, or even higher. That extra margin gives the processor a buffer to cover the higher rate of chargebacks and fraud they expect from your type of business.

Rolling Reserves: This is probably the most misunderstood part of high-risk processing. A rolling reserve means the processor holds back a small percentage of your daily sales (usually 5-10%) for a set amount of time (often 180 days). This cash is kept in a separate, non-interest-bearing account as collateral. If your business were to close down and leave a pile of chargebacks behind, the processor uses that reserve to cover the losses instead of paying out of their own pocket. Don't worry, the money is released back to you on a "rolling" basis once the holding period for each transaction is over.

Getting Your High Risk Merchant Account Approved

Getting approved for a high-risk merchant account can feel like a huge mountain to climb, but it's really more about building trust than passing a test. Don't look at the application as just another form to fill out. See it as your chance to make a strong, evidence-based case that your business is stable, responsible, and a good bet. The whole game is won with preparation and transparency.

When you gather all your documents beforehand and make sure your business looks solid online, you're sending a clear message to the underwriters: you get what they're worried about, and you're ready to be a reliable partner. This simple shift in approach turns the approval process from a frantic scramble into a confident presentation of your business's best self.

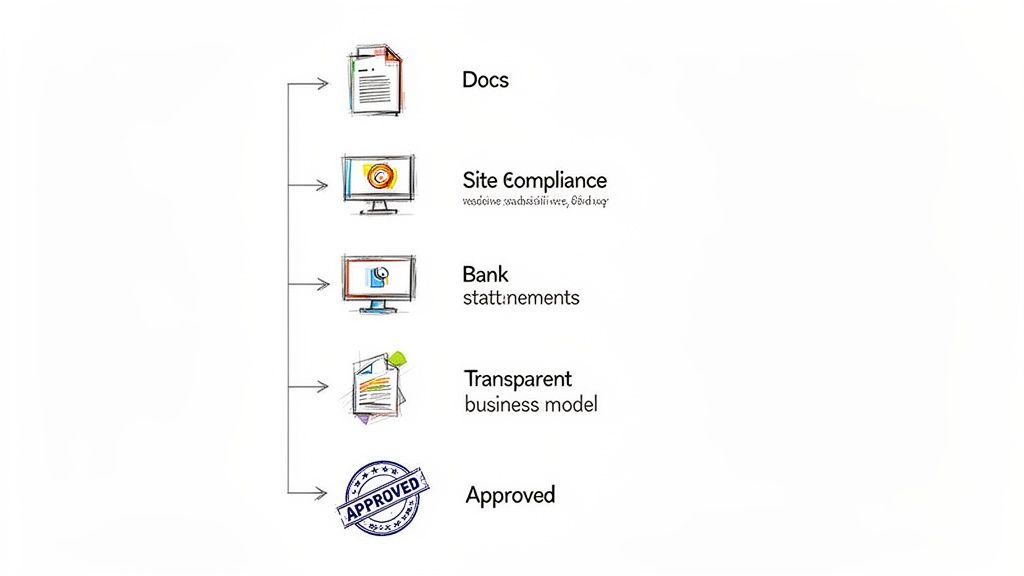

Gather Your Essential Documents First

Before you even think about starting an application, get your paperwork in order. Underwriters are always on the clock, and showing up with a complete, organized package proves you're a professional and helps them move things along faster. A neat file folder can make you stand out from the sea of disorganized applicants right away.

Your mission here is to paint a crystal-clear picture of your financial health and how you operate. The more buttoned-up your submission is, the fewer questions they'll need to ask.

You'll definitely need these items:

- Government-Issued ID: A crisp, clear copy of the business owner's driver's license or passport.

- Voided Business Check: This is how they verify the business bank account where your money will be deposited.

- Bank Statements: You'll need the last three to six months of your business bank statements. They're looking for consistent cash flow and a healthy daily balance.

- Processing History: If you’ve taken card payments before, pull together the last three to six months of your processing statements. This is your moment to prove you can keep your chargeback ratio under control.

- Business Formation Documents: Your Articles of Incorporation or LLC filing paperwork confirms that your business is a real, legal entity.

Optimize Your Website for Underwriting Scrutiny

Your website is often the very first place an underwriter goes to figure out your business. They aren't just glancing at your design; they are conducting a full-blown compliance audit. If your site is vague, makes wild claims you can't back up, or hides its customer service info, you’re raising major red flags.

Make sure your website clearly and honestly shows what you sell and how you do business.

An underwriter’s core job is to confirm your business is legitimate, compliant, and transparent. Your website is the primary piece of evidence they use to make that call. Make it easy for them to say yes.

Here are the key things underwriters are looking for on your site:

- Clear Product/Service Descriptions: They have to understand exactly what you’re selling. Being fuzzy about your products is a top reason for denial in credit card processing high risk applications.

- Visible Contact Information: A phone number, a real business address, and a customer support email need to be incredibly easy to find. It shows you’re accessible and not hiding from customers.

- Detailed Policies: Your Refund Policy, Privacy Policy, and Terms of Service must be detailed, easy to understand, and easy to find—usually in the website footer.

Present Your Business Model with Honesty

Finally, be an open book about your business model, especially the parts that land you in the high-risk category. If you’re a subscription service, explain your billing cycle and how customers can cancel. If you sell big-ticket items, walk them through your fulfillment process and how you verify customer identity.

Trying to hide or downplay the risky elements of your business is the single fastest way to get your application tossed in the "no" pile. Underwriters are pros at spotting inconsistencies. When you tackle their potential concerns head-on, you build credibility and prove you know how to manage your business's unique risks.

Strategies to Protect Your High Risk Merchant Account

Getting approved for a high-risk merchant account is a huge win, but the real work starts now. Think of it like this: you’ve just been handed the keys to a high-performance race car. The real skill isn't just starting it, but keeping it on the track and out of the wall. Your long-term success hinges on managing your account proactively and diligently.

At the heart of this is one core discipline: proactive chargeback prevention. For any business navigating the world of high-risk processing, this isn't just a good idea—it's the single most critical strategy for survival. Letting your chargeback ratio get out of control is the fastest way to get your account shut down.

The Non-Negotiable Role of Chargeback Alerts

What if you could get a heads-up that a customer was about to file a chargeback, giving you a chance to step in and fix the problem first? That’s exactly what chargeback alert systems do. For high-risk merchants, these services are an absolute must-have. They act as an early warning system, opening a crucial window of opportunity—usually 24 to 72 hours—to resolve an issue before it escalates.

Instead of finding out about a dispute weeks later when it officially hits your account, an alert pings you the moment a customer complains to their bank. This gives you time to issue a refund, make the customer happy, and stop the dispute from ever being recorded as a damaging chargeback against your record.

This simple, proactive step is the key to staying under that dreaded 1% chargeback threshold that card networks like Visa and Mastercard enforce.

Leveraging Card Network Prevention Tools

Today’s prevention tools go even further by plugging directly into the card networks' own resolution platforms. Two of the heavy hitters here are Visa's Rapid Dispute Resolution (RDR) and Mastercard's Chargeback Dispute Resolution Network (CDRN). When you use a service that integrates with these programs, you add a powerful, automated layer of protection.

- Visa RDR: This system lets you set up rules to automatically refund certain disputes without you having to lift a finger. For instance, you could create a rule to auto-refund any transaction under $25 with a specific reason code.

- Mastercard CDRN: This network delivers alerts straight from Mastercard-issuing banks, giving you that same critical window to solve a problem before it becomes a chargeback.

By using a platform that taps into these networks, you can automate a huge chunk of your dispute management. It's a powerful defense against account holds or termination, which can be absolutely devastating for a business. For merchants on platforms like Shopify, knowing how to handle these issues is vital; we have a detailed guide on what to do if you face a Shopify Payments account hold.

Combating the Rise of Friendly Fraud

One of the sneakiest threats out there is "friendly fraud," which happens when a customer disputes a legitimate charge. Maybe they forgot about a subscription, didn't recognize your company name on their statement, or just had a case of buyer's remorse. More and more, however, we're seeing a malicious version where customers knowingly dispute valid charges to get something for free.

This has become a silent killer for high-risk businesses. In fact, first-party fraud (where the actual cardholder is the one making the false claim) has exploded. It's a problem that requires a specific strategy to manage.

Your best weapon against friendly fraud is proactive communication. A clear billing descriptor, easy-to-find contact info, and a no-hassle cancellation process can stop a huge number of these disputes before they ever happen.

Best Practices for Long-Term Account Stability

Beyond automated tools, a few fundamental business practices will go a long way in protecting your merchant account and building a stable processing history.

- Crystal-Clear Communication: Make sure your billing descriptor is instantly recognizable. A generic name like "WEB SERVICES" is a recipe for a chargeback. Something specific like "ACME*YourBrandName" works much better.

- Exceptional Customer Service: It should be far easier for a customer to contact you than their bank. Put your phone number and email front and center, and respond to people quickly and professionally. Smart customer relationship management can also help reduce customer churn and the disputes that often come with it.

- Transparent Policies: Your refund, cancellation, and shipping policies need to be written in plain English and easy to find. Confusion leads to frustration, and frustration leads to chargebacks.

- Transaction Scrutiny: Always use fraud prevention tools like Address Verification Service (AVS) and CVV checks. Keep an eye out for red flags, like unusually large orders or multiple orders shipping to one address but paid for with different credit cards.

Ultimately, protecting your high-risk merchant account boils down to two things: creating a trustworthy and transparent customer experience, and having a powerful, automated safety net to catch the disputes that inevitably slip through.

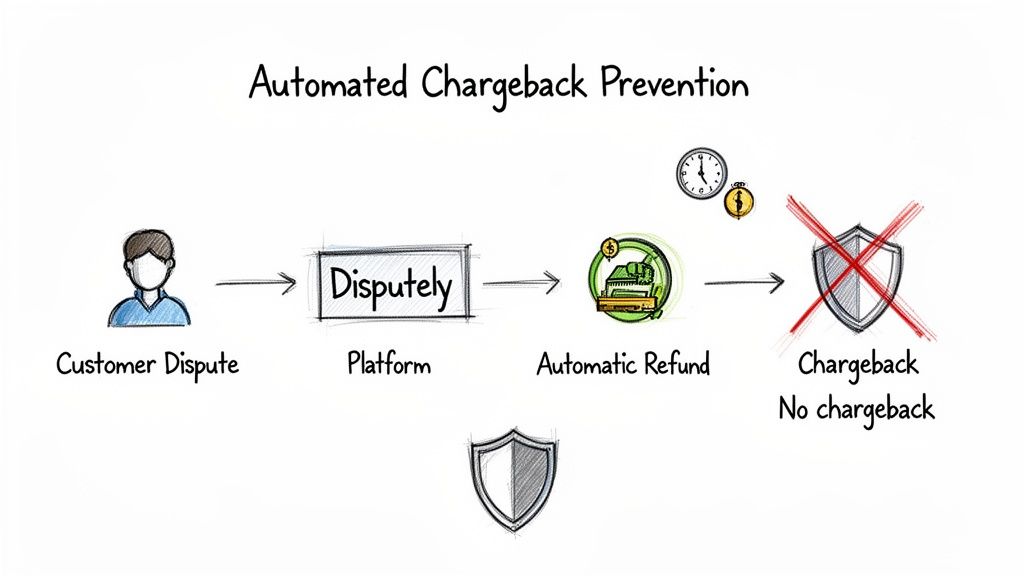

How Disputely Puts Chargeback Prevention on Autopilot

It's one thing to talk about strategies, but it’s another to see them work in the real world. For any business navigating the tricky waters of high-risk credit card processing, automation is what turns good intentions into solid results. Think of a platform like Disputely as a tireless security guard for your merchant account, standing watch 24/7 to stop problems before they escalate.

Let’s put this into perspective. Imagine you're running a thriving online supplement company built on a subscription model—a classic high-risk business.

One of your customers, Jane, is reviewing her credit card statement and spots a charge she doesn’t recognize. Her first move is to call her bank to ask about it. The second she does, her bank sends out an alert through networks like Visa’s RDR or Mastercard’s CDRN.

The Automated Intervention Process

Without an automation platform plugged in, you wouldn't hear a whisper about this for weeks. By then, it’s too late—it has already become a full-blown chargeback, dinging your precious chargeback ratio. But since you’ve connected your payment processor to Disputely, the story plays out very differently.

- Alert Received: Disputely’s system intercepts the bank's alert the moment it's sent.

- Rule-Based Action: The platform instantly analyzes the inquiry against the rules you’ve set. For example, you might have a rule to automatically refund any first-time dispute under $50 on a subscription.

- Instant Refund: Jane's transaction matches your rule, so Disputely automatically issues a refund directly through your payment processor.

- Dispute Deflected: The refund solves Jane’s problem, her bank gets the notification, and the inquiry is closed. Most importantly, it never becomes a chargeback.

This entire sequence happens in a matter of seconds, completely hands-off for you and your team. The system just neutralizes the threat, keeping your merchant account in good standing and your processor happy.

This kind of automated deflection is the secret to survival and growth for any high-risk business. It keeps your chargeback ratio safely below that dreaded 1% threshold, which helps you avoid costly monitoring programs. Even better, it sends a clear signal to your processor that you’re serious about managing risk, making you a partner they want to keep.

Of course, automation is about surgically removing the disputes you don’t need to fight, freeing you up to focus on the ones you can win. To learn more about that, check out our guide on the Q4 chargeback representment process.

Frequently Asked Questions

Stepping into the world of high-risk credit card processing can feel like learning a whole new language. It’s completely normal to have questions—the rules are different, the stakes feel higher, and the terminology can be a bit of a maze. Let's clear up some of the most common questions we hear from merchants.

Why Are My Processing Fees So High?

It’s easy to look at the higher fees and think of them as a penalty, but they’re actually more like an insurance policy for your payment processor. Because your business model or industry has a statistically higher chance of facing chargebacks and fraud, the processor is taking on a much bigger financial risk.

Those elevated fees are how they compensate for that exposure. That extra margin gives them a buffer to cover potential losses from disputes and pays for the hands-on, intensive monitoring needed to keep a high-risk account running smoothly.

Can I Switch to a Low-Risk Account Later?

Absolutely, but it’s a marathon, not a sprint. Getting reclassified from high-risk to low-risk is all about proving your business has become a stable, predictable partner. You have to build a rock-solid track record over time.

To make that happen, you'll generally need to show:

- A consistently low chargeback ratio—think well under 1% for at least 6 to 12 months.

- Steady and predictable sales volume, without any sudden, wild spikes that set off alarm bells.

- A healthy business bank account that isn’t constantly dipping into the red.

What Is a Rolling Reserve and How Does It Work?

A rolling reserve is simply a safety net for the payment processor. It’s a standard tool in high-risk processing where a small percentage of your daily sales (say, 10%) is held back for a set period, usually around 180 days.

You can think of a rolling reserve like a security deposit on an apartment. It creates a cash fund the processor can dip into to cover chargebacks or other unexpected losses if your business hits a rough patch. This way, they aren't left holding the bag. The funds are then released back to you on a "rolling" basis once the hold period for each transaction is over.

How Do Chargeback Alerts Prevent Disputes?

Chargeback alert systems are basically an early warning signal. When a customer calls their bank to question a charge, the alert network pings you instantly. This gives you a precious 24-72 hour window to handle the problem before it officially escalates into a damaging chargeback.

That heads-up gives you just enough time to issue a refund directly and solve the customer's issue on the spot. By doing so, you stop the dispute dead in its tracks. It never gets recorded against your merchant account, which is crucial for keeping your processing history clean and your account in good standing.

Protecting your revenue shouldn't be a constant battle. Disputely integrates directly with card networks to stop chargebacks before they happen, putting your dispute management on autopilot. See how much you can save and secure your merchant account today.