A Merchant's Guide to Debit Card Chargeback Prevention

When a customer disputes a transaction, merchants often think of credit card chargebacks. But a debit card chargeback is a whole different animal—and a much more immediate threat to your cash flow.

It’s essentially a forced refund, triggered by your customer’s bank. The money isn’t just held; it’s pulled directly out of your business bank account. Unlike a standard refund that you control, this process is involuntary and always comes with extra fees and penalties.

How Debit Card Chargebacks Really Work

Think of a customer refund as you willingly handing money back over the counter. A debit card chargeback, on the other hand, is like the customer's bank reaching directly into your cash register and taking the money back for them. It often happens with little to no warning.

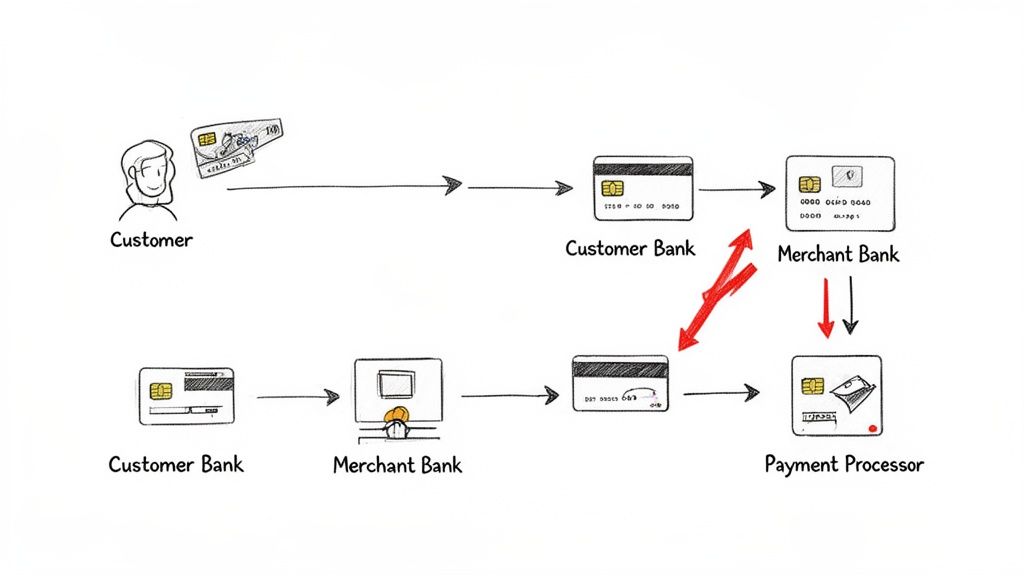

This isn't a simple two-way street. Several parties get involved:

- The Cardholder: This is your customer, the one who files the dispute.

- The Issuing Bank: The customer's bank. They investigate the claim and, if they find it credible, they pull the funds.

- The Acquiring Bank: This is your bank. They have to comply with the issuer's demand and facilitate the fund transfer.

- The Payment Processor: Companies like Stripe or PayPal act as the go-between, communicating the dispute from the banks to you.

Key Differences Every Merchant Needs to Understand

It's easy to lump all disputes together, but you can't treat a debit chargeback, a credit chargeback, and a simple refund the same way. Each one has a different impact on your business, and knowing the difference is the foundation of a solid dispute-prevention strategy. These processes are rooted in general banking practices, which set the rules for how money moves.

A common mistake is thinking debit and credit chargebacks are the same. They're not. A debit dispute yanks cash right out of your bank account today. A credit dispute freezes funds from a future payout. That makes the debit chargeback a much bigger emergency for your daily cash flow.

Let's break down exactly what sets them apart. This table shows the core differences from a merchant’s point of view. For more deep dives into managing disputes, our team regularly posts new guides on the Disputely blog.

Debit Card Chargeback vs Credit Card Chargeback vs Refund

| Attribute | Customer Refund | Debit Card Chargeback | Credit Card Chargeback |

|---|---|---|---|

| Initiator | Merchant (Voluntary) | Customer's Bank (Forced) | Customer's Bank (Forced) |

| Financial Impact | Loss of sale revenue | Revenue loss + fees + penalties | Revenue loss + fees + penalties |

| Cash Flow Effect | Controlled by merchant | Immediate cash withdrawal | Affects future settlement |

| Merchant Control | High (You set policies) | Low (Bank-driven process) | Low (Bank-driven process) |

As you can see, the key takeaway is the immediacy and lack of control associated with chargebacks, especially those tied to debit cards. While a refund is a manageable part of doing business, a chargeback is an expensive, time-consuming battle you're forced to fight.

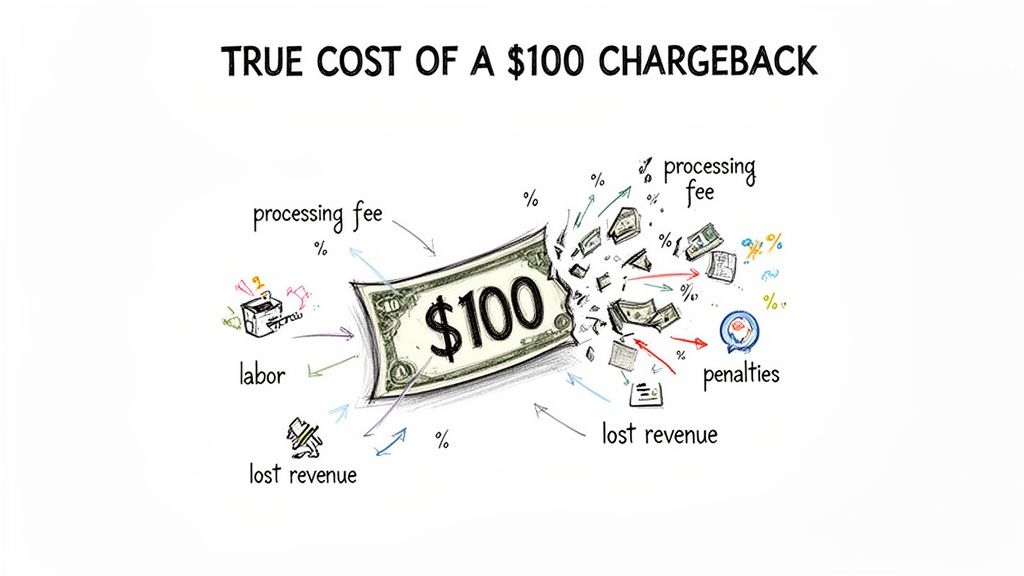

The True Cost of a Single Chargeback

A $100 chargeback might feel like a $100 loss. If only it were that simple. In reality, the financial fallout from a single debit card chargeback is much, much worse, and it catches most merchants completely off guard.

This is because of a painful "multiplier effect." The initial lost revenue is just the beginning. Layered on top of that are non-refundable processing fees, steep bank penalties, and the hidden operational costs that really start to add up.

And this isn't some minor issue; it's a rapidly growing threat to businesses everywhere. Global chargeback volumes are projected to jump from 238 million to 337 million between 2023 and 2026—a massive 41% increase in just a few years.

Even more telling, recent research shows that for every $1 lost to a chargeback, U.S. merchants actually lose an estimated $4.61. That’s a 37% spike from 2020. So, that seemingly small $100 debit card reversal actually ends up costing your business around $461 once you factor everything in. You can dig deeper into these chargeback statistics and their impact on merchants.

Deconstructing the Financial Damage

So where do all these hidden costs come from? It's not just the original sale and a penalty fee. The financial drain is multifaceted, pulling from different parts of your budget.

Think about your team's time. When they have to drop what they’re doing to fight a dispute, that’s a real labor cost.

- Operational Labor: Your staff has to spend precious hours digging up evidence, crafting compelling rebuttal letters, and going back and forth with your payment processor.

- Lost Product or Service: You're out the goods you already shipped or the service you delivered. In most cases, you're never getting that back.

- Marketing and Acquisition Costs: Don't forget the money you spent on ads, content, and sales efforts just to get that customer in the door. That's gone, too.

A chargeback isn't just a transaction reversal; it's a productivity killer. Every minute your team spends fighting a dispute is a minute they aren't spending on growing your business, improving your product, or helping legitimate customers.

The Long-Term Consequences

The damage doesn't end when a single dispute is resolved. A high chargeback ratio signals to payment processors that your business is risky, and that can trigger some serious long-term problems.

Processors might lock up a percentage of your revenue in a rolling reserve, holding your money for weeks or even months to cover any future chargebacks. In a worst-case scenario, they can just terminate your merchant account. That means you can no longer accept online payments at all.

Suddenly, a debit card chargeback looks less like a simple "cost of doing business" and more like a critical financial threat that demands a solid defense strategy.

Why Friendly Fraud Is Your Biggest Threat

While you might think of chargebacks as a result of stolen cards or your own shipping mistakes, the reality is much more frustrating. The single biggest driver behind most debit card chargebacks today is something called friendly fraud.

Friendly fraud isn't some complex hacking scheme. It's simply when a real customer disputes a purchase they actually made. It happens all the time for surprisingly common reasons: someone forgets about a recurring subscription, doesn't recognize your company's name on their bank statement, or just has a case of buyer's remorse. Sometimes, a family member might have used their card without asking first. In every case, a legitimate sale is being treated as if it were fraudulent.

Unfortunately, the modern banking world has made filing a dispute almost too easy. For many customers, a few taps inside their banking app feels a lot faster than trying to find your customer service number. The chargeback becomes a misguided shortcut to a refund.

The Alarming Rise of First-Party Misuse

This trend is more than just a minor headache; it's a growing epidemic that hits businesses hard. Friendly fraud, sometimes called first-party misuse, is now the number one reason for disputes, accounting for a massive chunk of merchant losses.

Research shows that this type of fraud now drives roughly 45% of all chargebacks. In some industries, that number skyrockets to 70%. The fallout can be devastating, especially for smaller businesses. A study backed by Mastercard found that nearly 1 in 5 small businesses hit by chargeback fraud were eventually forced to close their doors. You can dig into more of the data on how fraudulent chargebacks impact businesses.

What makes this type of dispute so damaging is that your standard fraud filters are completely blind to it. From your system's perspective, everything looks perfect—a real customer, a valid payment method, and a matching shipping address. No red flags go up until that dreaded chargeback notice lands in your inbox.

Friendly fraud weaponizes the very system designed to protect consumers, turning it against honest merchants. Because the transaction appears legitimate on the surface, proving your case becomes incredibly difficult, forcing you to fight an uphill battle to recover your rightful revenue.

Why It's More Than Just a Lost Sale

Unlike a clear-cut case of criminal fraud, friendly fraud blurs the lines and puts you in a tough spot. You're forced to spend precious time and resources fighting what often boils down to a customer's forgetfulness or a change of heart.

Every single one of these disputes adds to your overall chargeback ratio, putting your merchant account in jeopardy with payment processors. Each one also demands a detailed, time-consuming response, pulling your team away from tasks that actually grow the business. It's a silent profit killer that chips away at your bottom line, one dispute at a time.

Understanding the Debit Card Chargeback Lifecycle

The debit card chargeback process can feel like it comes out of nowhere, but it follows a predictable path. Once you learn the sequence of events, you can turn a chaotic situation into a clear series of actions. Think of it as a roadmap, guiding you from the moment a customer complains to the final decision.

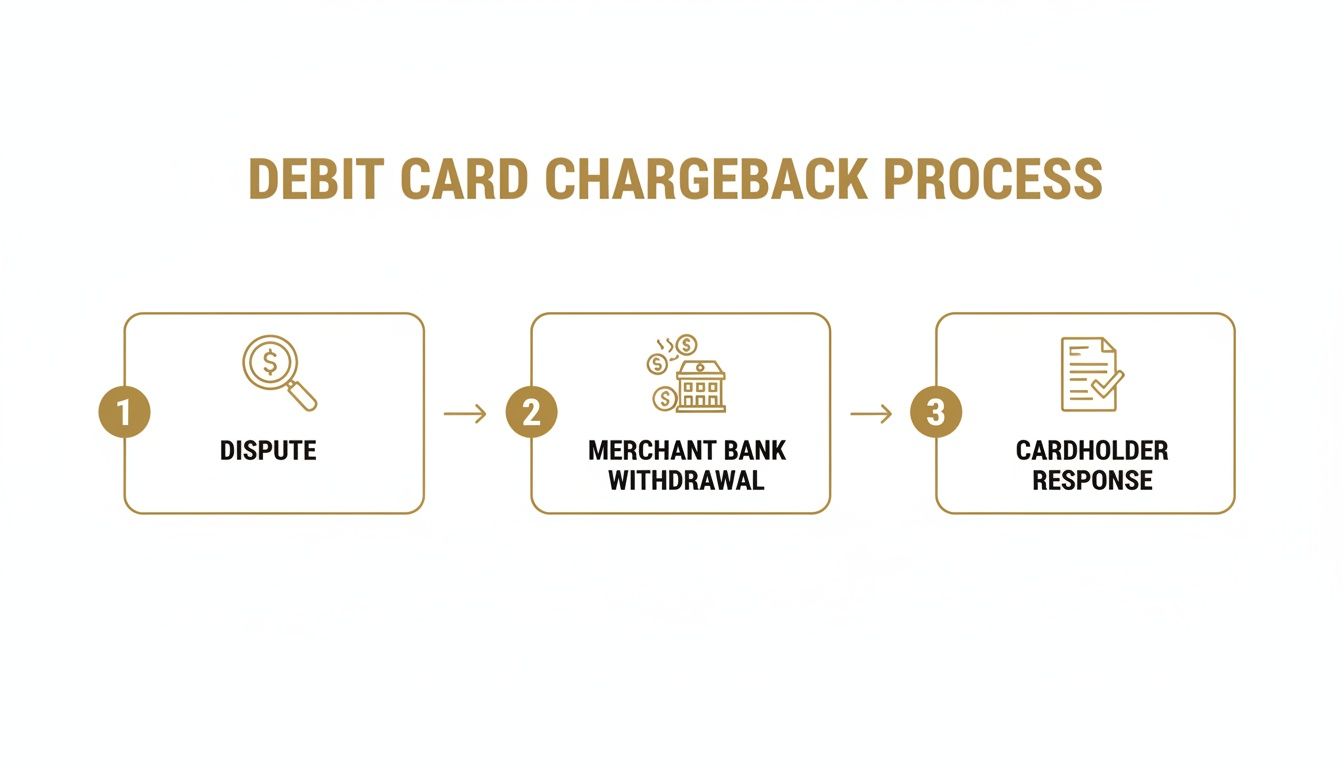

It all starts when your customer calls their bank—the issuing bank—to dispute a charge. Maybe they claim the product never arrived, they don't recognize the transaction, or the service wasn't what they expected. The bank doesn't call you first; it almost always gives its customer the benefit of the doubt, at least temporarily.

The Initial Fund Reversal

At this point, the issuing bank officially kicks off the chargeback. The disputed funds are immediately pulled from your merchant account by your bank, the acquiring bank. This is the part that stings with debit card chargebacks: real cash is pulled directly from your bank balance, hitting your cash flow instantly.

Next, you'll get a formal notification about the dispute, usually from your payment processor. This alert is packed with crucial information:

- The Transaction Details: The amount, date, and the specific product or service being disputed.

- The Reason Code: A specific code from the card network (like Visa or Mastercard) that explains exactly why the customer is disputing the charge.

- The Response Deadline: A strict timeline, typically just 20-45 days, for you to take action.

Think of this notification as a countdown timer. If you miss that deadline, you automatically lose. The funds are gone for good, you've lost the sale, and you never even got a chance to defend the transaction. It’s like not showing up for your court date.

Your Chance to Fight Back: Representment

Now it's your turn. You get to tell your side of the story in a process called representment. This is your official rebuttal to the chargeback claim, and it’s where you need to present compelling evidence that proves the transaction was legitimate and you held up your end of the bargain. Your success lives or dies by the quality of the evidence you provide.

Let's say the reason code is "Product Not Received." Your evidence packet should include things like:

- Proof of Delivery: Shipping confirmation with a tracking number that clearly shows the item was delivered to the customer’s address.

- Customer Communications: Any emails or chat logs where the customer acknowledges the order or even asks questions about the product.

- Order Details: A copy of the original invoice and the order confirmation you sent to the customer.

Submitting a strong, organized case is everything. You can get a much deeper look into building a winning response by checking out our guide to mastering the chargeback representment process.

After you submit your evidence, the issuing bank reviews everything and makes the final call. If they side with you, the funds are returned to your account. If they don't, the chargeback is upheld, and the customer keeps the money.

Proactive Strategies to Prevent and Fight Disputes

Okay, let's shift gears from understanding the problem to actively solving it. Tackling debit card chargebacks effectively means playing both offense and defense—preventing disputes from happening in the first place and responding quickly when they do. Winning this battle isn’t about fighting harder; it’s about fighting smarter.

The best defense is built long before a customer even thinks about calling their bank. Simple, proactive steps can cut down on the misunderstandings that often spiral into friendly fraud. Of course, solid fraud detection is also a must-have. Using tools like advanced transaction monitoring systems helps you spot and stop suspicious activity before it turns into a real problem.

Prevention Starts with Clarity

You'd be surprised how many disputes are born from simple confusion. By making your communication crystal clear at every turn, you can head off a huge chunk of these issues.

- Use Clear Billing Descriptors: Make sure the name on your customer’s bank statement is one they’ll recognize instantly. A vague legal entity name like "ABC Holdings" is a recipe for a chargeback. Use your website or brand name instead.

- Maintain Transparent Policies: Don't hide your refund and return policies in the fine print. When a customer knows how to get a refund, they’re far less likely to resort to a chargeback.

- Offer Exceptional Support: Make it easy for customers to reach you. A prominent phone number or a live chat can resolve an issue in minutes. A buried contact form, on the other hand, just fuels frustration and often leads to a call to the bank.

This whole process can escalate quickly. A customer complaint can become a direct withdrawal from your merchant account before you know it, forcing you into a formal response.

The visual above really drives home how fast a simple issue becomes a financial headache, which is why prevention and a rapid response plan are so critical.

The Power of Chargeback Alerts

Even with the best preventative measures, some disputes are just going to happen. This is where modern tech becomes your secret weapon. Instead of being blindsided by a formal chargeback notice weeks later, you can get out in front of it with chargeback alert networks.

Chargeback alerts intercept a dispute before it officially becomes a chargeback. This gives you a critical 24-72 hour window to resolve the issue directly with the customer by issuing a refund, completely avoiding the chargeback, its fees, and the negative mark on your record.

Platforms like Disputely tie into alert systems from Visa (RDR), Mastercard (CDRN), and Ethoca, giving you real-time notifications. This lets you automate refunds based on rules you set, stopping the dispute dead in its tracks. You sidestep the whole representment battle, keep your merchant account in good standing, and save a ton of money. For managing debit card chargeback risk, it’s a total game-changer.

Choosing Your Chargeback Management Approach

When it comes to handling debit card chargebacks, you're really looking at two paths: rolling up your sleeves and managing them yourself, or bringing in a specialized automated platform to do the heavy lifting. The best choice for you really hinges on your business's size, how many sales you're making, and the resources you have on hand.

For a smaller shop that only sees a few disputes a month, a manual approach can feel practical at first. This usually means someone on your team is tasked with digging up evidence, crafting compelling rebuttal letters, and sending everything off to your payment processor.

The upside is you avoid paying for software. The downside? It’s slow, it’s easy to make mistakes, and it simply doesn't work once you start growing. That administrative headache gets bigger with every new sale.

Manual vs. Automated Management

This is where modern, automated platforms completely change the game. These systems plug directly into your payment processor and connect to chargeback alert networks, giving you a chance to resolve a customer issue before it ever escalates into a formal chargeback. It’s a proactive strategy that saves your revenue and protects your all-important merchant account.

Manual management feels like bailing water out of a boat with a bucket. An automated platform is like finding the leak and patching it for good. You shift from constant damage control to smart, proactive prevention.

Think about this: 2025 data shows debit cards have a 5.93% chargeback ratio. For a busy ecommerce store handling thousands of orders, that percentage isn't just a nuisance—it's a serious financial threat. At that scale, automation becomes a necessity, not a luxury. You can dig into more chargeback statistics and their financial impact to see the full picture.

At the end of the day, a small subscription box service might get by with a manual system for a while. But any merchant with an eye on growth will quickly find that automation provides a much stronger return on investment. The time you save, the disputes you win, and the protection you gain are vital for building a sustainable business. You can explore the different tiers of automated chargeback protection to see how this works in the real world.

A Few Common Questions About Debit Card Chargebacks

When you're dealing with payment disputes, the same questions tend to pop up again and again. Getting straight answers is the first step toward building a solid strategy that protects your revenue and keeps your merchant account in good standing.

Can I Stop a Debit Card Chargeback After It's Filed?

In a word, no. Once a customer's bank officially files a debit card chargeback, the process is in motion. The money is automatically pulled from your account, and your only path forward is to fight it by submitting compelling evidence in a process called representment.

This is why prevention is everything. A chargeback alert service gives you a heads-up before a dispute becomes an official chargeback. This opens up a crucial 24-72 hour window for you to issue a refund, sidestepping the chargeback, the associated fees, and the hit to your reputation.

What Counts as Compelling Evidence to Win a Dispute?

Think of compelling evidence as your proof that you held up your end of the bargain. Your goal is to build an open-and-shut case that directly dismantles the customer's claim.

Here’s what that looks like in practice:

- Proof of Delivery: A shipping confirmation with a tracking number that shows the package was successfully delivered to the customer's address.

- AVS and CVV Results: The data from your payment gateway confirming the address and security code matched what the bank has on file for the cardholder.

- Customer Communications: Any emails, support tickets, or chat transcripts where the customer confirms their purchase or even just discusses the product.

- Terms of Service Agreement: A digital record or screenshot showing the customer actively checked a box agreeing to your policies before completing the purchase.

The strength of your evidence is what wins or loses a dispute. A clear, well-organized rebuttal with undeniable proof is your best shot at convincing the issuing bank to reverse the chargeback.

How Does My Chargeback Ratio Affect My Business?

Think of your chargeback ratio as a key health indicator for your business—one that payment processors monitor very carefully. If the number of chargebacks you receive creeps above the threshold set by the card networks (usually around 0.9% of your total transactions), you're heading into dangerous territory.

The consequences can be severe. You might face higher processing fees or have your funds frozen. In the worst-case scenario, your merchant account could be terminated, which essentially cuts off your ability to accept card payments altogether.

Trying to manage all of this manually is an uphill battle. Disputely automates your defense, giving you the chance to resolve disputes before they ever escalate into damaging chargebacks. It's about protecting your revenue and securing your business's ability to operate.

Learn how Disputely can safeguard your merchant account today.