Deposit Return Chargeback: deposit return chargeback Tactics to Protect Revenue

You've probably seen it before. A customer pays a deposit, something goes wrong, and suddenly you're hit with a chargeback. This is what we in the industry call a deposit return chargeback.

It's not an official reason code you'll find on a bank's list. Instead, it’s a merchant-specific headache that crops up when a customer disputes a charge tied to a security deposit or down payment. At its heart, this kind of dispute signals a total breakdown in communication and mismatched expectations between you and your customer.

What Exactly Is a Deposit Return Chargeback?

Unlike a clear-cut case of fraud where a stolen card is used, a deposit return chargeback is born from a customer relationship that's gone sour. It starts when a customer feels they're owed their deposit back, but you, the merchant, disagree and hold onto the funds based on your terms. Feeling stonewalled, the customer goes to their bank to get the money back by force. And just like that, you have a chargeback on your hands.

These disputes are especially rampant in businesses that lean on deposits to protect their assets or guarantee services. We see them all the time in vacation rentals, equipment leasing, event planning, and even with freelance contracts. In every case, that deposit is your safety net against damages, cancellations, or broken agreements.

A Look at Common Deposit Return Scenarios

To get ahead of these chargebacks, you first have to understand what triggers them. I've seen countless variations over the years, but they almost always fall into a few familiar patterns.

Below is a breakdown of the most common situations I've encountered. See if any of these sound familiar—recognizing your specific risk areas is the first step toward building a better defense.

Common Scenarios for Deposit Return Chargebacks

| Scenario | Customer's Claim | Merchant's Position | Common Industry |

|---|---|---|---|

| Damages & Repairs | "The damage was already there," or "It's just normal wear and tear." | The security deposit was rightfully used to cover damages caused by the customer. | Vacation Rentals, Car Rentals, Equipment Leasing |

| Service Cancellation | "I cancelled, so I should get my non-refundable deposit back." | The deposit was clearly stated as non-refundable to cover losses from cancellation. | Event Planning, Freelance Services, Custom Orders |

| Unmet Expectations | "The service/product didn't meet my expectations or match the description." | The service was delivered as agreed upon in the contract terms. | Web Design, Consulting, Home Improvement |

| Contract Disagreements | "I didn't agree to those terms," or "That clause is unfair." | The customer signed a contract explicitly outlining the terms for deposit forfeiture. | Any contract-based business |

Each of these examples highlights the messy, subjective nature of these disputes. It's not about a stolen credit card; it's one person's word against another's. That gray area is precisely why these chargebacks are so frustrating and difficult to win. If you want to dive deeper into handling different kinds of disputes, you can find more strategies on our blog.

The biggest challenge with a deposit return chargeback is that the burden of proof is on you. You have to provide compelling evidence showing the customer did violate your agreement, which is a much taller order than just proving a product was shipped.

The Real Financial Drain of Deposit Disputes

The damage from these chargebacks goes way beyond the disputed amount. Globally, chargeback volumes have swelled from 238 million to an estimated 261 million transactions, with the average dispute now costing over $169.

For merchants here in the U.S., the problem is even worse. We now lose an estimated $4.61 for every dollar in chargebacks due to all the associated fees, operational costs, and lost revenue.

Think about that. A single $500 deposit dispute could actually cost your business more than $2,300 in total losses. This doesn’t even touch on the potential harm to your merchant account's health, which can lead to higher processing fees or, in worst-case scenarios, account termination. These disputes are a slow, painful bleed on your revenue, turning what should have been profitable transactions into major losses.

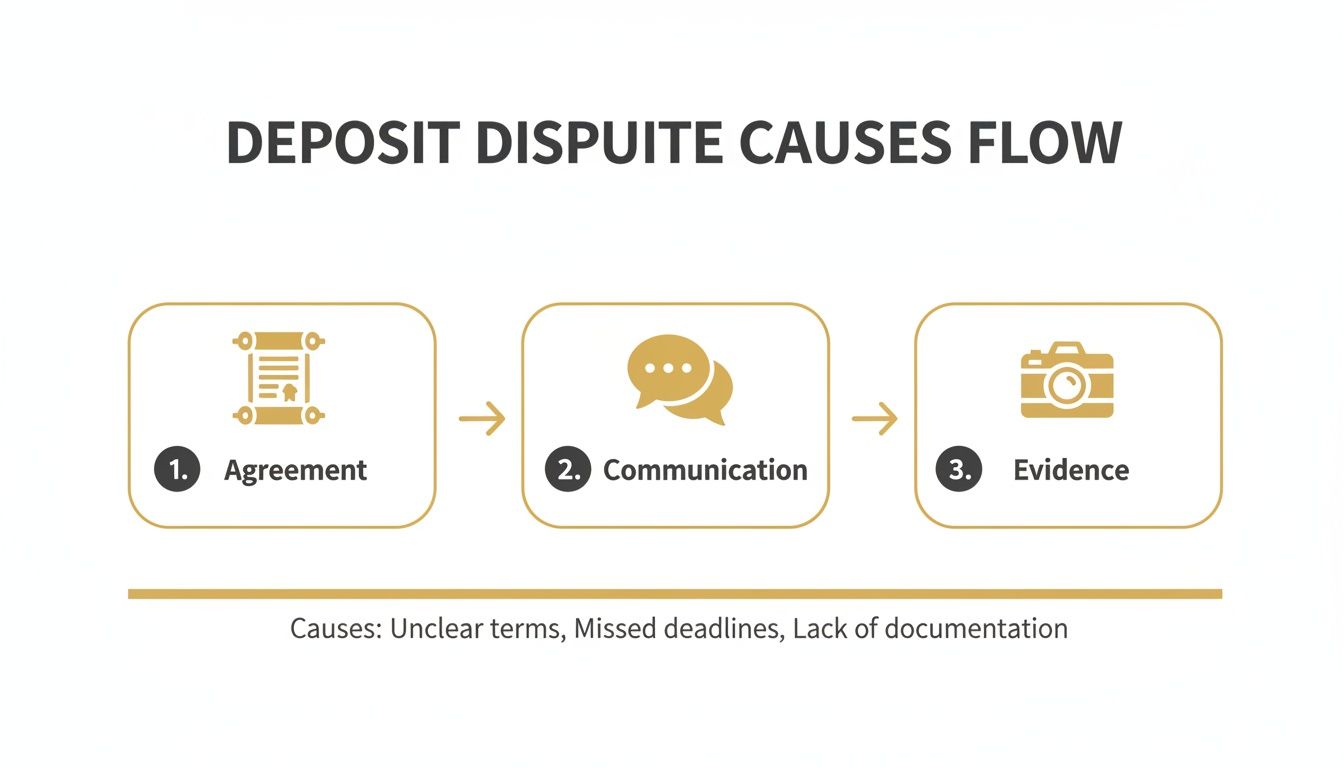

Getting to the Root of Deposit Disputes

A deposit return chargeback is never a random event. It’s the last, frustrating step in a process that went wrong much earlier. More often than not, these disputes sprout from small operational gaps—minor oversides that create just enough confusion for a customer to feel they have no choice but to call their bank.

Understanding where things break down is the secret to stopping these disputes before they ever start. It’s a mindset shift: stop fighting chargebacks reactively and start proactively fixing the issues that cause them. From what I've seen, most of these problems fall into three main buckets.

Vague Terms and Confusing Agreements

The first place things often go sideways is the rental or service agreement itself. Too many businesses grab a generic, boilerplate contract packed with legalese that customers either can't understand or just skim through. When a problem comes up later, that ambiguity becomes the customer’s biggest advantage.

Think about a clause that says something like, "deposit may be withheld for damages." That's practically an invitation for a chargeback. What's the difference between "damage" and "normal wear and tear"? If you don't define it with clear examples in your agreement, you’re leaving it up to interpretation. And you can bet the customer will interpret it in their favor.

Key Takeaway: Your deposit agreement isn't just a legal shield to hide behind. It needs to be a communication tool that sets crystal-clear expectations for everyone right from the get-go.

If a customer can argue they didn't understand why their deposit was at risk, the bank is very likely to side with them. This is especially true for any non-refundable deposits—the rules for those have to be explicitly spelled out and acknowledged by the customer before they ever pay.

Bad Communication (or No Communication at All)

Even with an ironclad contract, how you communicate during the return process can be the difference between a smooth transaction and a costly dispute. The absolute biggest mistake you can make is radio silence. Imagine a customer expecting a $500 refund, but only $300 shows up in their bank account with no explanation. Their first reaction isn't going to be calm curiosity; it's going to be anger.

This communication vacuum is where most preventable chargebacks are born. The customer just assumes you're trying to pocket their money, so they call their bank to get it back by force.

Instead, try being proactive. Let’s walk through a better scenario for an equipment rental:

- You inspect the returned gear and find a broken part.

- You immediately snap a clear photo of the damage.

- Right away, you text or email the customer the photo, point to the specific clause in their signed agreement, and explain the $200 deduction needed for the repair.

This simple act of transparent communication changes everything. You’ve shown them the evidence and given them an explanation before they even notice the partial refund. A potential shouting match becomes a documented business transaction. They might not be thrilled about the charge, but they understand it—and that makes a chargeback far less likely. By the way, if high dispute rates are causing other problems for you, our guide on handling a Shopify Payments hold has some great tips for staying in good standing with processors.

Weak or Missing Evidence

The final nail in the coffin for your defense is a lack of good evidence. When a customer files a chargeback, the script flips. The burden of proof is now 100% on you, the merchant, to prove you had a legitimate reason to keep that deposit. If you don't have solid documentation, your chances of winning are next to zero.

This is where so many businesses stumble. They don't document the "before" condition of a rental item or event space, so they have nothing to compare it to when it comes back.

Evidence you absolutely need to be collecting:

- Timestamped Photos/Videos: Get clear shots of the asset before it goes out and the moment it comes back.

- Signed Checklists: A detailed condition report or checklist, signed by the customer at the start, is invaluable.

- Clear Communication Trail: Keep a record of every email, text message, and note from phone calls about the deposit or any potential deductions.

Without this proof, any dispute just devolves into a "he said, she said" argument—and that’s a fight you’re statistically set up to lose. A customer’s claim that “it was already broken” is impossible to beat if you don’t have dated proof showing it wasn't. Building a simple, consistent evidence-gathering habit is the best insurance policy you can have against these disputes.

Building a Proactive Prevention Workflow

Let's move from theory to action. The only way to stop a deposit return chargeback is to get ahead of it. If you're reacting, you're already losing money. A proactive approach, on the other hand, protects your revenue and gives you back your peace of mind. This isn't about crossing your fingers; it's about building a solid, end-to-end playbook you can start using tomorrow.

This entire workflow breaks down into three key phases of the customer journey. By reinforcing your processes at each stage, you build an undeniable chain of evidence and clear communication that simply leaves no room for a dispute. It all starts long before a customer even thinks about asking for their deposit back.

Solidifying Your Pre-Transaction Safeguards

Your first line of defense is an ironclad agreement. This document has to be more than just a formality—it needs to be a simple, clear, and direct communication tool that sets crystal-clear expectations from the very first click.

Vague language is your absolute worst enemy. Don't just say, "deposit will be withheld for damages." Your agreement needs to define what "damage" is versus what counts as "normal wear and tear." For a vacation rental, you might specify that stained linens are considered damage, while minor scuffs on the floor are not.

Here's what every strong deposit agreement needs:

- Specific Deduction Scenarios: Clearly list the exact reasons a deposit might be partially or fully kept. Think property damage, missing items, a need for excessive cleaning, or late returns.

- Defined Timelines: State precisely when the customer can expect their deposit back. For instance, "Your deposit will be refunded within 7 business days following a satisfactory inspection."

- Digital Signature Requirement: Never, ever proceed without a digital signature and a timestamped record of the customer's agreement. This is your proof they saw and accepted your terms, shutting down any future claims that they "didn't know."

This flow chart really breaks down the common failure points that trigger disputes, highlighting how a weak agreement is often the first domino to fall.

As you can see, a solid agreement is the foundation for everything else. It makes your communication and evidence collection that much more powerful.

Documenting Everything During the Service Period

Once the rental or service actually begins, your focus has to shift to meticulous documentation. This is where you build the body of evidence that will make any potential dispute an open-and-shut case in your favor.

Your goal is to create a shared, undeniable record of the asset's condition from start to finish. A casual walk-through just won't cut it. You need tangible proof that both you and the customer are on the same page.

A common mistake is treating the check-in process as a casual handover. In reality, it's your most critical evidence-gathering opportunity. Every minute you spend here can save you hours of fighting a chargeback later.

Use a co-signed checklist that the customer reviews and signs right at the beginning. For an equipment rental, this list would detail every single component, its current condition, and any pre-existing scratches or dings. Pair this with timestamped photos or a quick video walkthrough that you immediately share with the customer via email or text. Now you have a baseline that can't be argued with.

Mastering the Post-Service Return Process

The final phase is where most businesses drop the ball—and where a deposit return chargeback is born. A structured, transparent return process is completely non-negotiable. It should be just as formal and buttoned-up as your check-in.

If you can, conduct the final inspection with the customer present. If they can't be there, record a video of your inspection and send it to them right away. This kind of transparency builds trust and heads off any accusations that you "found" damages after they left.

If you do need to make a deduction, your communication has to be swift and precise.

- Notify Immediately: Don't let the customer find out by seeing a partial refund on their bank statement. Contact them the moment you identify an issue.

- Provide Proof: Send them the "before" and "after" photos, referencing the exact clause in the agreement they signed.

- Itemize Costs: If repairs are necessary, provide an itemized invoice or a credible estimate for the cost. A vague "damage fee" is a huge red flag for both customers and their banks.

Finally, process the refund promptly—within the timeline you promised in your agreement. Many deposit disputes come from fuzzy expectations around refund timing. Implementing clear policies for effective return management can dramatically reduce these issues by making customers feel informed and respected. Delays just create anxiety and suspicion, giving the customer every reason to think something is wrong and call their bank.

Using Chargeback Alerts to Intervene Instantly

Even with a rock-solid prevention workflow, you're not going to stop every single dispute. A customer might still feel wronged, get impatient waiting for a refund, or simply misunderstand your terms. When that happens, you need a way to step in before a simple complaint spirals into a full-blown, revenue-draining chargeback.

This is where chargeback alert networks become your most valuable ally. Services from providers like Ethoca (owned by Mastercard) and Verifi (owned by Visa), which offers the Consumer Dispute Resolution Network (CDRN), act as a crucial early warning system. They open up a direct line of communication between the customer’s bank and you, the merchant.

How Chargeback Alerts Change the Game

So, how does it work? When a customer calls their bank to dispute a charge, the bank doesn't immediately file a formal chargeback. Instead, it sends an alert through these networks that lands right in your system.

This alert gives you a critical window—usually just 24 to 72 hours—to fix the problem directly.

For a deposit return chargeback, this is a complete game-changer. Let's say a customer disputes a $200 deduction from their security deposit because of a damaged rental item. You get an alert. Instead of gearing up for a fight you’re likely to lose, you can simply issue a full refund on the spot.

The complaint is resolved, the customer is happy, and most importantly, the chargeback never officially happens. You completely sidestep the non-refundable chargeback fee, protect your merchant account's dispute ratio, and avoid a long, drawn-out battle gathering evidence.

Proactive Deflection vs. Reactive Fighting

Without alerts, your first sign of trouble is the chargeback notice itself. By then, it’s already too late. The damage is done: the fee has been slapped on your account, your dispute ratio takes a hit, and the funds are long gone. You're left scrambling to build a representment case that, statistically, is an uphill battle.

Think of it like a smoke detector versus a fire extinguisher. Prevention workflows are the fireproofing you build into your house. Chargeback alerts are the smoke detector that wakes you up the moment a small problem starts, letting you handle it before the whole house is engulfed in flames. Fighting the chargeback itself is like using the extinguisher after the fire is already raging.

This proactive approach has never been more critical. The chargeback crisis has exploded, with retail ecommerce seeing an unbelievable 233% surge in chargeback rates. This volatility is fueled by the normalization of 'friendly fraud,' where an estimated 75% of chargebacks now come from legitimate customers. What's more, 84% of customers admit that filing a chargeback is just more convenient than asking for a refund. You can find more insights on how these dispute trends impact businesses.

Making Smart Financial Decisions Instantly

Alerts let you make a strategic business decision, not an emotional one. For many deposit disputes, especially those under a certain amount like $100, the math is brutally simple.

- Cost to Fight: Lost revenue ($100) + a non-refundable chargeback fee (~$25) + your team's time (hours of work) = $125+ and a black mark on your dispute ratio.

- Cost to Refund via Alert: Lost revenue ($100) + the alert fee (~$15) = $115 and a clean record.

By refunding through an alert, you still take the revenue hit, but you prevent all the follow-on financial and reputational damage. You’re essentially buying your way out of the chargeback process for a fraction of the total cost, preserving your relationship with your payment processor and keeping your business out of high-risk monitoring programs. This instant intervention turns a potential catastrophe into a manageable operational expense.

Putting Your Chargeback Defense on Autopilot

Staying on top of alerts from services like Ethoca and CDRN is a solid first step, but let's be honest—it’s still reactive. Alerts don't care about business hours; they pop up whenever they want, demanding you drop everything. The real game-changer is connecting all those pieces—your prevention tactics and alert systems—into a single, automated strategy that works around the clock.

Think of it like this: you plug your Stripe or Shopify Payments account into a system that handles the entire alert workflow for you. Suddenly, you're not frantically checking emails or dashboards. Instead, you have a defense system that stops a deposit return chargeback while you sleep. The goal is to make chargeback prevention a quiet background process, not your main job.

Setting Your Automated Defense Rules

This is where you get to be strategic. True automation isn't one-size-fits-all; it’s about setting simple, custom rules that reflect how you run your business. Using a platform like Disputely, you can define exactly how to respond to different alerts without lifting a finger.

For instance, a no-brainer for many businesses is setting a rule to automatically refund any alerted dispute under $75. The math is simple. The cost of the alert fee plus the small refund is almost always less than the hit you'd take from a non-refundable chargeback fee, lost revenue, and the time you'd sink into fighting it. One simple rule can wipe out a huge chunk of those frequent, low-value disputes.

You can get even more specific, especially for deposit-related headaches:

- Auto-Refund by Product: If a particular rental item is notorious for causing deposit disagreements, you can set a rule to auto-refund any alert tied specifically to it.

- Auto-Refund by Value: Set a threshold, say $100, for any security deposit dispute. If you know from experience it’s not worth the fight, let the system handle it.

- Intelligent Filtering: Got ironclad evidence for a transaction, like a signed damage waiver? Create a rule to ignore alerts for those, so you're only fighting the battles you know you can win.

Having a clean dashboard gives you a bird's-eye view of your automated defense, turning what used to be a mess of data into clear, actionable insights.

This kind of centralized view is crucial. It lets you see how your rules are performing in the real world and tweak them over time to get the best results.

The Real Business Benefits of Automation

Automating your chargeback defense is about so much more than just saving time. It’s about building a stable foundation for your business by protecting your most critical asset: your ability to accept payments.

The ultimate benefit of automation isn't just stopping chargebacks; it's gaining total peace of mind. Knowing you have a system in place that protects your business 24/7 lets you focus on growth instead of constantly playing defense.

When your dispute ratio stays consistently low, you unlock some serious advantages. First off, you avoid getting flagged and dumped into costly monitoring programs by Visa and Mastercard. Those programs are a nightmare of heavy fines and intense scrutiny—automation is your best bet for staying off their radar.

Second, you keep your payment processor happy. Processors like Stripe are constantly on the lookout for high-risk merchants. A low dispute rate proves you’re a reliable partner, making it far less likely they’ll place holds on your funds or, in a worst-case scenario, shut down your account. You can learn more about fortifying your business at https://disputely.com/campaign/q4-representment.

To see the difference clearly, let's compare the old way of doing things with an automated approach.

Manual Dispute Handling vs. Automated Disputely Workflow

| Process Step | Manual Handling (Without Disputely) | Automated Workflow (With Disputely) |

|---|---|---|

| Alert Notification | Receive individual emails or log into multiple portals. | All alerts are aggregated into a single dashboard. |

| Initial Review | Manually assess each alert's details (amount, reason, customer). | Pre-defined rules filter alerts instantly based on your criteria. |

| Decision Making | Someone on your team has to decide: refund or ignore? | The system decides automatically based on your rules (e.g., refund if <$75). |

| Action Execution | Manually process a refund in your payment gateway. | The system triggers the refund automatically via API. |

| Time Investment | 5-15 minutes per alert, often at inconvenient times. | Zero minutes per alert. The system runs 24/7. |

| Risk Factor | High risk of human error, missed alerts, and delayed responses. | Extremely low risk. Consistent, instant, and error-free execution. |

| Cost | Unpredictable. Includes labor costs, alert fees, and potential chargeback fees. | Predictable. A fixed platform cost and controlled refund amounts. |

Ultimately, automation shifts chargeback management from a chaotic, unpredictable drain on your resources into a manageable, predictable operational cost. No more being blindsided by random fees and revenue losses. Instead, you have a system that handles threats methodically, giving you a clear financial picture and a stable foundation to scale your business.

Clearing Up the Confusion: Your Top Deposit Chargeback Questions Answered

Even with the best game plan, deposit return chargebacks can feel like a curveball. Questions always come up. Let's tackle some of the most common ones we hear from merchants dealing with these tough disputes.

I Have Proof—Can I Actually Win a Deposit Return Chargeback?

Technically, yes, you can fight a deposit chargeback with solid evidence. But I have to be honest with you: it's an uphill battle. These disputes often devolve into a messy "he said, she said" situation where the customer’s bank tends to side with their customer.

If you’re going to fight, your evidence needs to be airtight. We're talking about:

- A digitally signed agreement where your deposit and damage terms are spelled out in plain English.

- Timestamped photos or videos—before the rental and immediately after—showing the item's condition.

- A crystal-clear log of every email, text, and phone call with the customer about the deposit or any charges against it.

Even with a mountain of proof, representment is a drain on your time and money. That’s why using a chargeback alert system is often the smarter play. Refunding through an alert lets you dodge the non-refundable chargeback fee and keeps your merchant account's dispute ratio in a safe zone.

My Take: Winning a dispute is about proving the customer was wrong. Preventing a dispute is about making it impossible for one to be filed. When it comes to deposits, prevention is almost always the more profitable route.

How Does Disputely Know Which Alerts to Refund?

Here's the great thing: you're the one in the driver's seat. Inside the Disputely dashboard, you're not getting a one-size-fits-all solution. You create your own custom automation rules that make sense for your business and your risk level. You tell the system exactly how to react when an alert comes in.

For instance, you can easily build rules to:

- Auto-refund all alerts below a set dollar amount, like $50. It just doesn't make financial sense to fight over small amounts.

- Zero in on specific products or services that you know are magnets for deposit disagreements.

- Set up "ignore" rules for certain transactions. Maybe you have ironclad evidence for a specific high-value rental and you're prepared to take that fight to representment.

This kind of smart filtering means you're only refunding what you have to, stopping the chargebacks that hurt the most without giving away revenue unnecessarily. It's a scalpel, not a sledgehammer.

Isn't an Alert System Like Disputely Expensive?

Not when you compare it to the alternative. A single chargeback fee can set you back anywhere from $15 to over $100 before you even factor in the lost revenue and the time your team spends fighting it.

Chargeback alert services work on a pay-per-alert basis. The cost to deflect a dispute is just a small fraction of what you'd pay in fees if it turned into a full-blown chargeback. For any business that handles deposits, it’s an investment with a massive ROI that protects your cash flow and, just as importantly, your relationship with your payment processor.

Ready to stop fighting fires and start preventing them? Disputely hooks up to your payment processor in just a few minutes. You can set up smart rules to automatically handle alerts before they ever become costly chargebacks, protecting your revenue and your merchant account. Get started with Disputely today.