Your Essential Guide to High Risk Merchant Accounts

A high risk merchant account is a special kind of payment processing account built for businesses that banks and processors see as having a greater chance of chargebacks or fraud. Think of it as a financial safety net for the processor, making it possible for businesses in less conventional industries to accept credit and debit cards.

If you've ever been turned down by mainstream processors like Stripe or PayPal, this "high-risk" label is almost certainly the reason why.

Decoding The High Risk Label

Getting flagged as 'high-risk' can feel like a penalty, but it’s not a reflection of your business's quality or your integrity as an owner. It’s simply a risk calculation from the perspective of the financial institutions that move the money.

It’s a bit like car insurance. A teenager driving a sports car will always pay a higher premium than a 40-year-old with a minivan. It's not personal; it's just based on statistics. The sports car simply carries more financial risk for the insurer. A high risk merchant account works the same way—it's specialized coverage for a business model that carries more statistical risk.

What It Really Means for Your Business

So, what is this "risk" all about? It boils down to financial liability. When a customer files a chargeback, the payment processor is often left holding the bag, forced to refund the money while the dispute is investigated.

Industries labeled high-risk are those where chargebacks happen more frequently, which creates a huge financial headache for the processor.

At its core, the high risk classification is a proactive measure by financial institutions to protect themselves from potential losses stemming from chargebacks, fraud, and regulatory complexities associated with certain industries or business models.

This is exactly why standard processors often shut down accounts in these industries without much notice. Their entire business model is based on serving low-risk, predictable businesses at a massive scale. They just aren't set up to handle the underwriting or potential losses that come with a high-risk business.

Why Chargebacks Are Central to Risk

Chargebacks aren't a small problem—they're a massive one. In 2023 alone, the payment world was hit with 238 million chargebacks, costing merchants billions of dollars. This is the central reason the high-risk category even exists.

For companies in these sectors, finding dedicated high risk merchant account solutions isn't just a good idea; it's essential for survival. A high-risk processor understands your industry's challenges and has the systems in place to manage them, giving your business a stable and reliable way to get paid.

Of course. Here is the rewritten section with a more human, expert tone.

Why Processors Might Label Your Business "High Risk"

Let's get one thing straight: when a payment processor calls a business "high risk," it’s not a judgment call on your character or the quality of your work. It's a purely financial assessment. This label is all about statistics and risk management from their perspective.

Think of it like an insurance company assessing a driver. They aren't deciding if you're a "good" or "bad" person; they're looking at your age, your car, and your driving record to predict the likelihood of an accident. In the same way, payment underwriters look at specific traits of your business and industry to predict the odds of financial loss—mainly from chargebacks.

So, what are they actually looking at? Let's break down the common triggers that land businesses in the high-risk category.

Industries Prone to Chargebacks

The biggest factor, by far, is the potential for chargebacks. If your industry has a reputation for frequent customer disputes, you're almost guaranteed to be considered high risk. The magic number here is often a chargeback ratio that creeps over 1%. Once you hit that threshold, standard processors get very nervous.

Why do some industries get hit with so many disputes? It usually comes down to a few core issues:

- Subjective Results: Think about businesses in the nutraceuticals or online coaching space. They sell an outcome that isn't always guaranteed or measurable. When a customer doesn't see the results they hoped for, their first move is often to file a chargeback.

- Recurring Billing Confusion: Subscription boxes, SaaS products, and membership sites are fantastic business models, but they have a built-in chargeback problem. Customers forget they signed up, don't recognize the company name on their statement, and dispute the charge.

- "Friendly" Fraud: Some sectors are just magnets for this. A customer buys and uses your product or service, then files a chargeback to get their money back. It’s essentially a dishonest way to get a refund, and it's a huge headache for merchants.

How You Sell Can Be a Red Flag

Sometimes, the risk isn't about what you sell, but how you sell it. Your business model itself can introduce risks that make processors uneasy, especially when there's a long delay between payment and fulfillment.

The travel industry is a perfect example. Someone might book a cruise six months from now. In that half-year gap, a lot can happen. Plans can change, the trip could get canceled, or the customer might just get cold feet.

The longer the time between a customer's payment and when they get what they paid for, the more risk the processor sees. This long liability window is a prime breeding ground for chargebacks, leaving the processor on the hook if your business can't cover the refund.

This isn't just about travel. The same logic applies to businesses like:

- Event Ticketing: Selling tickets to a festival that’s months away.

- High-Ticket Items: Think custom furniture or luxury goods that have long lead times. A single dispute on a $5,000 item is a much bigger loss than one on a $50 product.

- Pre-Orders: Taking money for a product that hasn't even been manufactured yet is a classic high-risk model.

Regulated and Controversial Industries

Finally, some industries are flagged as high risk simply because of legal, regulatory, or reputational issues. If you operate in a field that's heavily scrutinized or operates in a legal gray area, you’re automatically in this category.

Here are a few common ones:

- CBD and Nutraceuticals: With constantly shifting state laws and FDA scrutiny, the regulatory ground is always moving.

- Adult Entertainment: High chargeback rates combined with reputational risk for the acquiring bank make this a classic high-risk niche.

- Online Gaming and Gambling: These industries are tightly regulated and come with a high risk of fraud and disputes.

- Credit Repair and Debt Services: These businesses are watched like a hawk for consumer protection violations, which adds a compliance burden that many processors won't touch.

If your business falls into any of these buckets, you won't be able to just sign up for a standard, off-the-shelf merchant account. You'll need a processor that specializes in your world—one who truly understands the compliance landscape and is equipped to handle the risks involved.

Getting to Grips With Underwriting and Pricing

If you're used to standard payment processing, applying for a high-risk merchant account is a whole different ball game. Forget the instant, automated approvals. This is more like a full-scale financial check-up for your business, and it's intentionally thorough.

Think of the processor's underwriting team as financial detectives. Their mission is to dig into your business operations to fully understand the specific risks they'd be taking on. They're not trying to find a reason to say no; they're building a complete risk profile to price their services accurately.

This deep dive is essential because the processor is on the hook financially if your business goes under or gets hit with a wave of chargebacks you can't cover. In a very real sense, they're co-signing on your business's future.

The Underwriting Deep Dive

So, what does this "financial check-up" actually look at? Underwriters will comb through several key parts of your business to assess its stability and legitimacy. They want to see signs of a well-managed company that, despite its high-risk label, is a solid partner.

Having your ducks in a row here is non-negotiable. Get your documents ready ahead of time, which usually means providing:

- Financial History: At least six months of business bank statements are needed to show you have consistent cash flow and a healthy financial pulse.

- Processing Statements: If you're not new to this, they'll want to see your past processing statements. They’ll be zeroing in on your transaction volume, average ticket size, and, most critically, your chargeback ratio.

- Business Model Verification: Get your supplier agreements, business plans, and any necessary licenses together. This proves your operation is above board and compliant.

- Website Compliance: Your website will be put under the microscope. Make sure your terms of service, privacy policy, and contact info are clear and easy to find.

This level of scrutiny gives the processor a clear picture of the potential financial exposure before they sign on. A complete, organized set of documents makes the entire approval process much smoother.

Why High-Risk Accounts Cost More

After the underwriting team gives the green light, you'll get your pricing. It’s crucial to understand that the higher fees aren't a punishment. They're more like an insurance premium, compensating the processor for shouldering a much greater degree of financial risk.

The higher fees directly reflect the increased statistical odds of chargebacks, fraud, and business failure. The processor is simply pricing the risk that your specific business model and industry bring to the table, creating a financial cushion for potential losses.

Here are some common costs you can expect:

- Higher Discount Rates: This is the percentage fee taken from every transaction, and it will be noticeably higher than what low-risk businesses pay.

- Increased Transaction Fees: That small, fixed fee tacked onto each sale might also be a bit steeper.

- Monthly Service Fees: Plan on a higher monthly fee for account maintenance, support, and monitoring.

- Rolling Reserves: This is a big one. A processor might hold a percentage of your revenue (e.g., 10% for 180 days) in a non-interest-bearing account as a safety net against future chargebacks.

Knowing these realities from the start lets you approach the application process with your eyes wide open. When you’re prepared for the financial and paperwork requirements, you can secure the processing you need to grow. As you move forward, looking into the pricing for chargeback prevention tools is a smart way to get a handle on these costs over the long run.

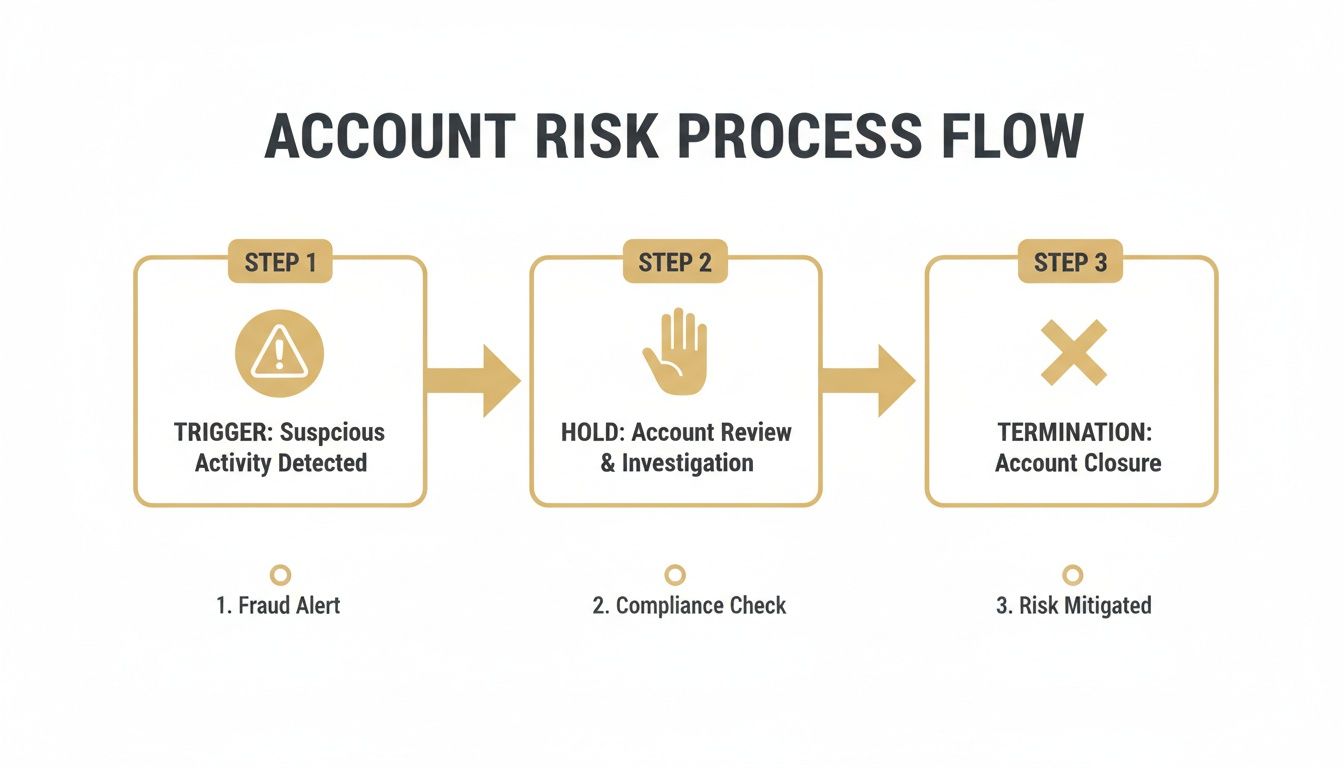

Navigating Account Holds, Reserves, and Terminations

For any high-risk business owner, there are three words you never want to hear from your payment processor: hold, reserve, and termination. Waking up to find your funds frozen or your account shut down can feel like a sudden catastrophe, but these actions are rarely random.

Think of them as a processor's self-defense system. They aren't trying to punish you; they're protecting themselves from the financial fallout of chargebacks. When their systems detect patterns that scream "future losses," they act fast to create a financial buffer. The good news? These triggers are predictable. If you know what to look for and manage your business proactively, you can keep your processor happy, your cash flow stable, and your account in good standing.

What are Rolling Reserves and Account Holds?

Let's demystify the two most common measures processors use to protect themselves.

A rolling reserve is a standard tool in the high-risk playbook. It’s like a security deposit that’s constantly in motion. Your processor will hold back a small percentage of your daily sales in a separate, non-interest-bearing account for a set period.

For instance, a common setup is a 10% rolling reserve held for 180 days. This means on Monday, 10% of your sales are set aside. On Tuesday, 10% of that day's sales are set aside. After 180 days, Monday's funds are released back to you as Tuesday's funds continue to be held. This rolling fund gives the processor a safety net to cover potential chargebacks down the road, even if your business hits a rough patch.

An account hold (often called a freeze) is a much more serious step. This is when the processor stops all payouts to your bank account—period. It usually happens in response to a sudden, alarming event, like a massive sales spike that looks fraudulent or a sudden flood of customer disputes. Your money is still coming in, but you can't touch it until the processor completes its investigation. This can create a serious cash flow crisis, which is why it's so critical to understand how to handle an unexpected Shopify hold if one happens to you.

A hold is the processor's emergency brake. They pull it when they see activity so far outside your normal patterns that it forces a complete stop to assess the potential damage from fraud or chargebacks.

Common Triggers That Put Your Account on Thin Ice

So, what exactly makes a processor hit the panic button and slap a reserve or hold on your account? While every provider has its own risk models, some red flags are universal.

- Blowing Past Chargeback Thresholds: This is the big one. If your chargeback ratio starts creeping over the 1% industry line in the sand, you're going to get a call. It often starts with a warning, but it can escalate to a reserve or hold very quickly.

- Sudden Jumps in Sales Volume: Nothing looks more like a "bust-out" scheme than a business that goes from $5,000 a day to $50,000 overnight without giving the processor a heads-up. That kind of spike almost guarantees a manual review.

- A High Tide of Refunds: A refund is always better than a chargeback, but a consistently high refund rate is a signal of widespread customer dissatisfaction. To a processor, that’s a leading indicator that a wave of chargebacks is about to hit.

- Pivoting Your Business Model: If you suddenly start selling a completely different type of product—especially if it’s a higher-risk item—your processor needs to re-underwrite your account. They based their original approval on a specific risk profile, and any major change requires a new look.

These triggers are made worse by the sheer scale of the fraud problem. In 2024 alone, businesses are on track to lose an estimated $8.9 billion to chargebacks globally. With friendly fraud—where a customer disputes a charge they actually made—now accounting for around 75% of all cases, you can understand why processors are on high alert. Knowing these triggers is the first step in safeguarding your business and ensuring your revenue keeps flowing.

Proven Strategies to Protect Your Merchant Account

Knowing the risks of holds, reserves, and terminations is one thing, but actively preventing them is a whole different ballgame. Securing your high-risk merchant account isn't about crossing your fingers and hoping for the best. It takes a hands-on, strategic approach to risk management that builds trust with your payment processor and protects your hard-earned revenue.

The goal is pretty straightforward: show your processor, through your actions, that you're a reliable partner, even if you operate in a "risky" industry. This comes down to a mix of transparent communication, smart business practices, and using the right tech to get ahead of problems before they even start.

Adopt Best Practices to Reduce Chargebacks

The single most effective way to protect your account is to choke off chargebacks at the source. Every dispute you prevent is a direct win for your chargeback ratio and sends a clear signal to your processor that you’ve got things under control.

It all starts with the basics of good communication. A surprising number of chargebacks, especially those from "friendly fraud," happen because a customer simply doesn't recognize a charge on their statement.

- Use Crystal-Clear Billing Descriptors: Make sure the name that shows up on a customer's credit card statement is instantly recognizable. It should be your store or product name, not some obscure legal entity they've never heard of.

- Maintain Open Customer Communication: Make it ridiculously easy for customers to contact you. Put your phone number and email front and center, and be quick to respond. A customer who can get a refund directly from you is far less likely to file a chargeback with their bank.

- Send Proactive Notifications: If you run a subscription service, always send renewal reminders before you bill. For physical goods, get that shipping and tracking info into the customer's hands right away.

The path from a small risk trigger to potential account closure is often predictable. The key is knowing where to intervene.

As you can see, getting ahead of these issues is everything. Addressing a trigger early stops it from snowballing into a hold or termination that could threaten your entire business.

Leverage Technology to Stop Disputes in Their Tracks

While solid business practices are your foundation, the most powerful tactic is to stop disputes before they ever become official chargebacks. This is where chargeback alert and prevention technology comes in, acting as an early-warning system for your business.

Services like Visa's Rapid Dispute Resolution (RDR) and alert networks from Ethoca and Verifi give you a critical heads-up. When a customer calls their bank to question a charge, these systems fire off an immediate, real-time alert directly to you.

This alert is not a chargeback. It’s a pre-dispute warning that gives you a chance to solve the problem—usually by issuing a refund—before it’s officially filed. When you do, the issue is resolved, and it never hurts your official chargeback ratio.

This one move is an absolute game-changer for any high-risk merchant. Instead of fighting a messy, uphill battle after a chargeback is filed, you completely sidestep the damaging process. Your chargeback ratio stays low, your processor stays happy, and you avoid all the fees and headaches that come with formal disputes. For the disputes you can't avoid, it's worth reading our guide on developing an effective chargeback representment strategy.

Plugging in a platform like Disputely puts this entire defense system on autopilot. It connects directly to these alert networks, watches your transactions 24/7, and can automatically issue refunds based on rules you define. No more disputes slipping through the cracks. This automated shield is the most powerful tool you have for keeping your merchant account safe, stable, and open for business.

Choosing the Right High Risk Payment Processor

Picking the right partner for your high risk merchant account is one of the most critical decisions you'll make. This goes way beyond just shopping for the lowest rates. You're looking for a stable, long-term relationship with a provider who actually gets your business and is built to handle its unique challenges.

Think of it this way: you wouldn't hire a general contractor to perform heart surgery. You'd want a specialist. The same logic applies here. The right processor is a specialist who won’t get spooked by the first sign of turbulence.

Look for Deep Industry Experience

Your first and most important question for any potential processor should be about their experience in your specific industry. A processor that specializes in, say, subscription boxes will understand the chargeback patterns and customer behavior common in that space. That's a world away from the risks involved in travel or online gaming.

This kind of specialized knowledge is invaluable. It means a faster, more intelligent underwriting process and risk monitoring that makes sense for your business model. They've seen what works (and what doesn't) for businesses just like yours, which makes them more of a strategic partner than just a service provider. Don't settle for a jack-of-all-trades.

Scrutinize Their Policies and Support

Before you even think about signing a contract, you need to dig into the fine print. Get really clear on the policies that can directly impact your cash flow. Ask direct questions and don't stop until you get a straight answer.

- Holds and Reserves: What’s their standard rolling reserve policy? What exactly triggers an account hold, and what’s the step-by-step process for getting your funds released?

- Customer Support: When your money is frozen, you need a human being on the other end of the line, not an endless phone tree. Is their support team available 24/7? Will you get a dedicated account manager who knows your name?

- Integrated Risk Tools: A true partner is invested in your success. Do they offer built-in tools like chargeback alerts or fraud prevention services? Processors who help you lower your risk are the ones you want to work with.

The cheapest processor is almost never the best. Higher fees for a stable account with fantastic support and risk management tools are a much smarter investment than rock-bottom rates from a provider who will drop you at the first sign of trouble.

Understand Who You Are Working With

Finally, it’s crucial to know who you’re actually partnering with. Are you talking to an Independent Sales Organization (ISO), which is essentially a sales agent for a larger bank, or are you working directly with a dedicated high-risk processor?

There's no single right answer, but transparency is key. They should be upfront about their relationship with the acquiring bank and be fully equipped to handle your business’s volume and risk profile. Your goal is to find a partner who acts as an advocate for your business, helping you navigate the complexities of high-risk payments so you can get back to what you do best—running your company.

Your High-Risk Questions, Answered

Venturing into high-risk payment processing naturally brings up a lot of questions. Let's tackle some of the most common ones you'll encounter, so you can move forward with confidence.

Can I Get a High-Risk Merchant Account with Bad Credit?

Yes, you can, but expect a tougher road. When personal credit is a concern, underwriters will shift their focus and dig much deeper into other areas of your business. They’ll want to see a solid processing history and healthy bank statements to feel confident in your business's stability.

To compensate for the added risk, they might ask for a larger rolling reserve or set stricter contract terms. Your best bet is to be upfront about your credit situation. Come prepared with documentation that paints a clear picture of your business's financial health and shows you have a handle on risk management.

How Long Does Approval for a High-Risk Account Take?

Patience is key here. Unlike a standard account that can sometimes get approved in hours, a high-risk application is a more deliberate process. You should plan for it to take anywhere from a few days to several weeks.

This isn't just bureaucratic red tape. The extended timeline allows the processor's underwriting team to perform a serious deep dive. They’re scrutinizing your business model, financial records, website compliance, and your entire risk profile before they agree to a partnership.

What's the Difference Between a Chargeback and a Refund?

Understanding this difference is non-negotiable for any merchant, especially a high-risk one.

A refund is a simple, direct transaction between you and your customer. You agree to return their money, and the issue is resolved amicably. It has no negative impact on your merchant account. A chargeback, on the other hand, is a forced reversal of funds triggered by the customer’s bank. It gets officially recorded by the card networks and directly damages your chargeback ratio.

Letting chargebacks pile up is a fast track to hefty fines and, ultimately, the termination of your account. This is precisely why preventing them is so critical.

Why Can’t I Just Use Stripe or PayPal for My Business?

While amazing for low-risk businesses, payment aggregators like Stripe or PayPal have an extremely low appetite for risk. Their automated systems are built to identify and shut down accounts in high-risk industries or those with fluctuating sales volumes—often with little to no warning.

That’s where a dedicated high-risk merchant account comes in. It's underwritten from day one with your specific business model in mind. This gives you the stability and specialized support you need to grow your business without constantly looking over your shoulder, worried that your payment processing could be shut down overnight.

Ready to stop disputes before they become costly chargebacks? Disputely integrates directly with alert networks to give you the power to refund a transaction before it damages your merchant account. Protect your revenue and secure your payment processing relationships by visiting the Disputely website to see how it works.