A Guide to High Risk Merchant Processing

If your business has been labeled "high-risk," it can sound a little scary. But in the world of payment processing, this isn't a judgment call on your business's quality or legitimacy. It’s simply a classification based on risk—a bit like how car insurance companies view a teenager driving a sports car versus a seasoned driver in a minivan.

High-risk merchant processing is a specialized service designed for businesses that, for one reason or another, have a higher statistical chance of chargebacks, fraud, or financial hiccups. It's the system that allows these businesses to accept card payments when a standard processor might say "no thanks."

What Does High-Risk Merchant Processing Actually Mean?

Think of it this way: when a standard, low-risk business accepts a credit card, the processor sees it as a pretty safe bet. The chances of that transaction going sour are minimal. But for a high-risk business, the processor is taking on more liability.

Imagine you're the one lending the money. Lending to someone with a perfect credit score is one thing. Lending to someone with a shakier history? You'd probably want some extra assurances, like a higher interest rate or a co-signer. That’s essentially what high-risk processors do. They provide the same service—letting you accept payments—but with different terms to protect themselves from potential losses.

This structure isn't meant to be a punishment. It's the financial framework that makes it possible for industries like subscription services, travel agencies, and supplement companies to even exist in the e-commerce space. Without it, they'd be cut off from the primary way customers pay for things online.

The Financial Reality of High-Risk

So, what's the big deal? It all comes down to financial exposure. In 2024 alone, businesses lost a jaw-dropping $8.9 billion to chargebacks. That number is only climbing as fraud schemes get more sophisticated.

High-risk industries are on the front lines of this battle. Many see their chargeback rates creep above the 1% threshold that card networks like Visa and Mastercard use as a warning sign. Once you cross that line, you land squarely in high-risk territory. You can dig into the latest fraud trends to see just how prevalent this has become for certain merchants.

The bottom line is that if a high-risk business racks up a bunch of chargebacks and can't cover the cost, the processor is left holding the bag.

At its heart, high-risk merchant processing is a partnership built on a different set of rules. It acknowledges the unique challenges certain business models face and provides a structured, albeit more expensive, pathway to participate in the global digital economy.

The extra fees, rolling reserves, and stricter underwriting are all part of that "insurance policy" for the processor. Understanding this foundation is the first step. From here, you can start building strategies to manage your account, lower your risk profile, and eventually qualify for better terms.

Why Your Business Is Considered High Risk

Getting slapped with the "high risk" label can feel personal, but it’s not. For payment processors and their partner banks, it’s purely a numbers game based on a calculated risk assessment. Think of it like a car insurance company quoting a premium for a 17-year-old driving a sports car—the data suggests a higher probability of an incident.

Processors look at your business model and industry through the same lens, trying to predict their financial exposure to things like chargebacks and fraud. It’s not a judgment on your business’s quality, but a pragmatic decision based on historical data. Understanding exactly what they see as risky is the first step to getting a handle on it.

Some Industries Are Just Born Risky

Let’s be honest: some business models are just naturally prone to more disputes. Processors aren’t just looking at your company in a vacuum; they’re looking at the track record of your entire industry. If your sector has a history of high chargeback rates, you’re almost guaranteed to be flagged from the start.

This table breaks down some of the most common high-risk industries and the specific factors that make processors nervous.

Common High-Risk Industries and Their Primary Risk Factors

| Industry | Primary Risk Factor(s) | Common Business Model |

|---|---|---|

| Nutraceuticals & Supplements | Aggressive marketing claims lead to customer dissatisfaction and disputes. | E-commerce, Subscriptions |

| Subscription Services | Customers forget about recurring charges, leading to "friendly fraud." | Recurring Billing, Trials |

| Travel & Ticketing | Long gap between payment and service delivery increases cancellation/dispute risk. | Future Delivery, High-Ticket |

| Online Gaming & Gambling | Subject to heavy regulation, legal complexities, and high-value fraud attempts. | MOTO/CNP, International |

| Adult Entertainment | Reputational risk for the bank, high chargeback rates, and regulatory concerns. | Subscriptions, Digital Content |

| Credit Repair & Debt Services | Promises of future results often lead to disputes if outcomes aren't met. | Future Delivery, Regulated |

| Firearms & Ammunition | Strict legal regulations and reputational risk for financial institutions. | E-commerce (CNP), Regulated |

As you can see, the "why" often comes down to a few core issues: future delivery of services, recurring billing models that customers forget, and products that live in a regulatory gray area.

How You Run Your Business Is Under the Microscope

Beyond your industry, your specific day-to-day operations play a massive role. You could have two coffee shops on the same street, but if one only takes online orders and has a new owner with bad credit, its risk profile will be completely different.

Processors dig into these operational details during underwriting, and a few things always raise red flags:

- High Average Transaction Value: Selling big-ticket items means each chargeback hurts more. A single $2,000 disputed charge is a much bigger financial hit for the processor than a $20 one. This simple math makes businesses with high average order values appear much riskier.

- Card-Not-Present (CNP) Transactions: Any time the credit card and the customer aren't physically in the same room, the risk of fraud skyrockets. E-commerce and MOTO (mail order/telephone order) sales are prime targets for fraudsters using stolen card information.

- Poor or Limited Credit History: This applies to both the business and its owner. If the owner has a low personal credit score or the business is brand new with no processing history, banks have no data to prove you can manage your finances and cover potential chargebacks. You're an unknown quantity.

A business isn't just one thing—it's a collection of risk factors. A new subscription box company (subscription model + no history) selling high-end electronics (high transaction value) online (CNP) is a perfect storm of elements that demand a high risk merchant processing solution.

Ultimately, your risk status is a composite score. It’s a mix of the industry you operate in, how you sell your products, your financial background, and your history with chargebacks. By pinpointing which of these factors apply to your business, you can start seeing things from the processor’s perspective—and that’s the key to building a strategy to manage and reduce that risk over time.

Understanding the True Cost of Your Merchant Account

That "high-risk" label does more than just categorize your business—it completely redraws your financial map. To really get a handle on the impact, you have to look past the surface-level transaction fee. It’s not just one higher rate; it’s a whole ecosystem of costs designed to protect the processor, and it can seriously eat into your profits and choke your cash flow.

Think of it as the processor building a financial buffer. They see a greater chance of chargebacks and fraud with your business model, so they hedge their bets. While a standard, low-risk shop gets predictable, low costs, your account plays by a different, much more expensive set of rules.

The Sticker Shock of Processing Fees

The first and most obvious hit comes from the percentage you pay on every single sale. A low-risk e-commerce store might be paying somewhere between 2% to 3% in processing fees. For a high-risk business, that's just the starting line.

High-risk merchant fees often kick off at 4% and can soar to 8% or even higher. That jump isn't arbitrary; it's a direct reflection of the risk they believe they're taking on. In fact, a 2025 analysis shows that when you factor in all the extra fees, the total cost of accepting payments can devour 10% to 12% of total revenue for many high-risk businesses. This is a tough pill to swallow, especially for high-volume brands in industries like supplements, online gaming, and subscription services that depend on specialized high-risk merchant processing. You can dig deeper into these numbers by checking out the latest analysis of high-risk merchant costs from PaymentNerds.com.

Demystifying the Merchant Account Reserve

Beyond the bite out of every transaction, one of the biggest financial hurdles you'll face is the merchant account reserve. The simplest way to think about a reserve is as a security deposit held by your processor. It’s a chunk of your own money they set aside to cover any potential losses from future chargebacks. For most high-risk accounts, this isn't optional.

You'll typically run into two main types of reserves:

- Rolling Reserve: This is the most common. The processor holds back a percentage of your daily sales—usually 5-10%—for a set amount of time, often around six months. So, as each day passes, the money they held from 180 days ago is released back to you, but they hold onto a new percentage from today's sales. It creates a constantly refreshing safety net for them, but it can put a serious strain on your working capital.

- Capped Reserve: With this setup, the processor holds a percentage of your funds until the reserve hits a specific, agreed-upon dollar amount (the "cap"). Once you hit that cap, they stop holding money back. However, if a wave of chargebacks depletes the reserve, they’ll start holding funds again to build it back up.

The merchant account reserve directly impacts your cash flow. It’s not a fee you pay, but rather your own revenue being held in escrow, unavailable for paying suppliers, running marketing campaigns, or covering payroll.

The Hidden Costs That Add Up Quickly

Unfortunately, the financial hits don't stop with processing rates and reserves. A high-risk account often comes with a whole menu of other charges that can sneak up on you and turn a manageable cost into a major expense.

Here are a few of the most common ones to watch out for:

- Chargeback Fees: Every time a customer files a dispute, you get hit with a penalty fee—and you pay it whether you win or lose the fight. For high-risk accounts, these fees are much steeper, often ranging from $25 to over $100 per incident.

- Monthly Minimum Fees: Many processors will require you to generate a certain amount in processing fees each month. If you have a slow month and don't hit that minimum, you’ll be charged the difference.

- Setup and Application Fees: Just getting approved can come with one-time costs. These are fees that low-risk merchants almost never have to worry about.

Let's see how this plays out in the real world. Imagine an online supplement store doing $50,000 in monthly sales. A 6% processing fee instantly takes $3,000 off the top. Then, a 10% rolling reserve holds another $5,000 of their revenue hostage. If they get hit with just 20 chargebacks in a month at $50 a pop, that’s another $1,000 gone.

All of a sudden, a huge chunk of their revenue is either paid out in fees or tied up where they can't touch it, making financial planning a nightmare. This is exactly why protecting your business from disputes is so critical. A smart next step is understanding the pricing and ROI of chargeback prevention tools to stop these costs from spiraling out of control.

How to Proactively Reduce Chargebacks and Lower Your Risk

If you're a high-risk merchant, it's easy to fall into the trap of thinking chargebacks are just a cost of doing business. That’s a massive mistake. Think of dispute prevention as your single most powerful tool for taking back control. This isn't just about saving money on fees; it’s a direct strategy for improving your risk profile, building trust with your payment processor, and eventually earning better terms.

By actively managing and shrinking your chargeback ratio, you start to look less like a liability and more like a stable, reliable partner. That's the shift that gets you out from under restrictive reserves and the punishingly high fees that come with the high-risk label.

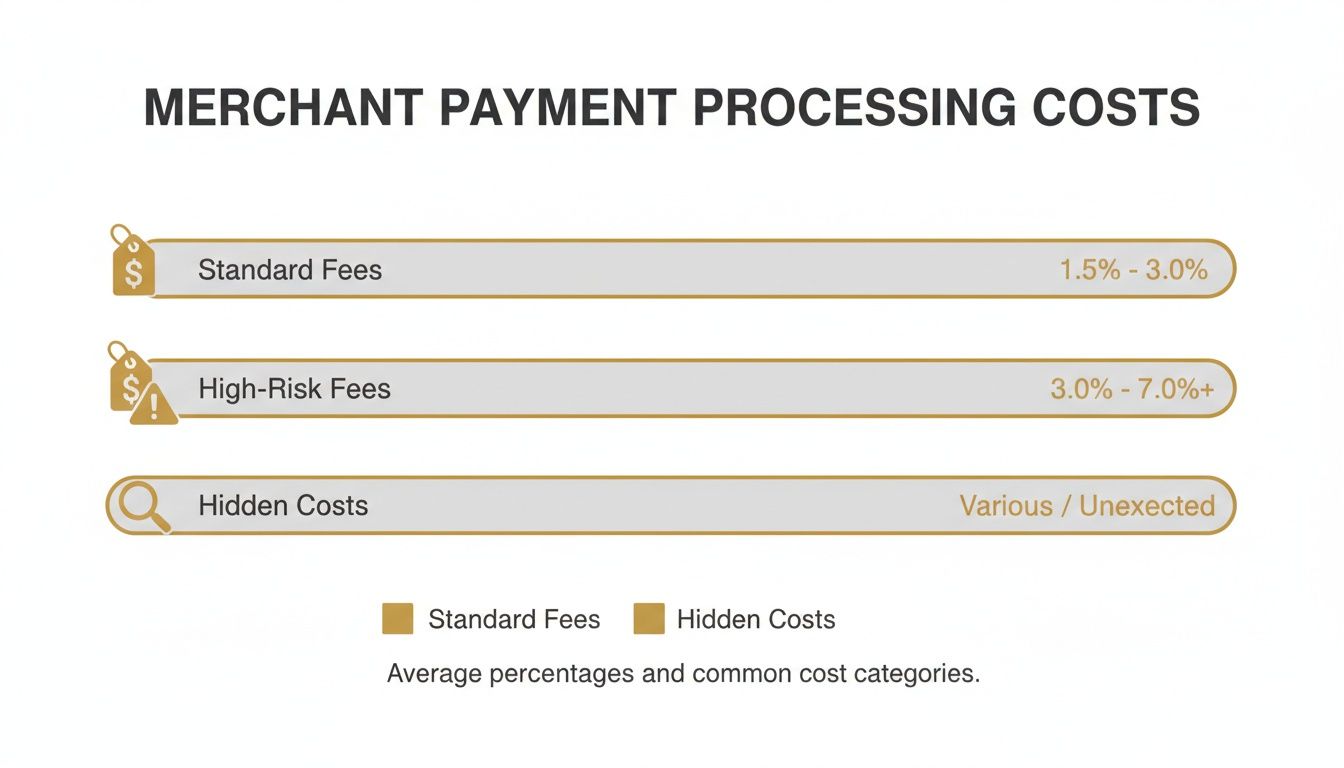

This infographic gives you a clear picture of the major cost categories high-risk merchants run into, putting the difference between standard and specialized processing fees in stark relief.

The numbers don't lie. While standard fees are one thing, the elevated rates and hidden costs tied to high-risk accounts can seriously eat into your bottom line.

Laying the Groundwork with Clear Communication

Before you even think about fancy tools, get the fundamentals right. A surprising number of chargebacks, especially the "friendly fraud" kind, are born from simple confusion or a clunky customer experience. A few small tweaks here can make a world of difference.

- Crystal-Clear Billing Descriptors: Make sure the name that shows up on your customer’s credit card statement is instantly recognizable. A cryptic descriptor like "ONLINE SVS-888" is practically begging for a chargeback. Instead, use your brand name loud and clear, something like "YOURBRAND NUTRITION."

- Responsive Customer Service: Make it ridiculously easy for customers to reach you with a problem. Put your phone number, email, and live chat options front and center. A support team that’s easy to find can resolve an issue and process a refund long before a frustrated customer resorts to calling their bank.

- Transparent Policies: Your refund, cancellation, and shipping policies should be simple to find and even simpler to understand. When expectations don't match reality, disputes are sure to follow.

The Power of Proactive Chargeback Alerts

Okay, strong fundamentals are non-negotiable, but the real game-changer in modern dispute management is chargeback alert services. These tools essentially intercept a dispute before it officially becomes a chargeback, buying you a critical window to take action.

Think of it as an early warning system for an earthquake. Instead of cleaning up the rubble, you get a heads-up that lets you sidestep the damage entirely. Leading alert networks like Ethoca (from Mastercard) and Verifi (from Visa) work directly with the banks that issue credit cards to make this possible.

Here’s a quick rundown of how it works:

- A customer calls their bank to question a charge from your business.

- The bank, instead of launching a formal chargeback, sends an "alert" through the Ethoca or Verifi network.

- Your alert management platform gets this notification almost instantly.

- You now have a 24 to 72-hour window to issue a full refund to the customer.

- By refunding the transaction, you’ve solved the customer's problem. The dispute is stopped in its tracks, a formal chargeback is never filed, and it never blemishes your merchant account record.

Chargeback alerts do more than just prevent one financial loss—they protect your all-important chargeback ratio. Keeping that ratio below the dreaded 1% threshold is the single most important metric for staying in good standing with your processor and the card networks.

Automating Your Defense for Maximum Impact

Trying to manage alerts manually is a recipe for disaster, especially if you're dealing with any real transaction volume. This is where automated alert management platforms become absolutely essential. These systems plug directly into the alert networks and your payment processor, creating a seamless line of defense.

You can set up rules to automatically refund transactions based on criteria like the dollar amount or the reason for the dispute. This ensures you never miss that critical 24-72 hour window. This kind of automation is a lifeline for merchants facing a constant threat of fraud. Recent data is sobering: by 2025, a staggering 98% of high-risk ecommerce merchants had been hit by at least one fraud attack, with friendly fraud and refund abuse leading the charge. Automated alerts offer a powerful shield, with some merchants slashing their dispute rates by up to 99%.

By putting these tools to work, you build an undeniable case for your business's stability. You can walk into a conversation with your processor armed with hard data showing a dramatically lower chargeback ratio. That’s your best leverage for negotiating lower fees, reducing your rolling reserve, and finally shedding the most painful parts of the high-risk label. For those times you need to fight back against illegitimate claims, you may want to check out our guide on how to handle chargeback representment.

How to Choose the Right High Risk Payment Processor

Choosing a high risk payment processor is less like picking a new software and more like entering into a serious business partnership. Get it right, and you have a partner who truly understands the pressures of your industry and can help you grow. Get it wrong, and you could face strangled cash flow, a damaged reputation, or even a sudden account termination that shuts you down overnight.

This isn't just about getting an account approved; it's about finding a stable financial backbone for your company. A processor with deep experience in your specific niche—whether it’s subscription boxes or supplements—will already know the common chargeback triggers and regulatory headaches you’re up against. That kind of specialized knowledge is gold.

For example, a business looking for iGaming Payment Solutions can't just go with any generic provider. They need a processor with the right banking relationships and risk models to navigate that complex world. A standard processor simply won't cut it.

Your Vetting Checklist: Questions to Ask

Before you even think about signing a contract, you need to interview potential processors. Treat this exactly like you're hiring a CFO. Their answers (or lack thereof) will tell you everything you need to know about their business and whether they’re the right fit for you.

Here’s a practical checklist of questions to get you started:

- Industry Experience: "Which other companies in my industry—like nutraceuticals or travel—do you work with?" This quickly confirms they have real-world experience and won't be learning on your dime.

- Fee Structure: "Can you give me a full, itemized breakdown of every single fee?" Push for total transparency. You need to know the transaction rates, monthly fees, chargeback fees, and any other potential "gotcha" costs.

- Reserve Policy: "What are the exact terms of your merchant account reserve?" Find out if it’s a rolling or capped reserve, the percentage they hold, and, most importantly, the criteria for lowering or removing it over time.

- Contract Terms: "What’s the contract length, and what are the penalties for early termination?" Be wary of long-term contracts with hefty cancellation fees. They can trap you with a partner that isn't working out.

- Integration Support: "How does your gateway work with my platform?" Whether you’re on Shopify, WooCommerce, or a custom cart, make sure the integration is smooth and well-supported.

Red Flags to Watch Out For

While you're looking for good signs, it's just as critical to spot the red flags. Some processors prey on high-risk merchants, dangling attractive offers that hide nasty surprises in the fine print.

A processor promising "guaranteed approval" or "instant setup" is a massive red flag. Proper high risk underwriting takes time and effort. Anyone skipping those steps is cutting corners that will inevitably cost you later.

Here are a few other warnings that should make you hit the brakes:

- Vague Fee Disclosures: If a provider won't give you a clear, written schedule of every fee, walk away. It’s a classic sign they plan on nickel-and-diming you with hidden charges down the road.

- Excessively Long Contracts: A three-year, non-cancellable contract is a huge gamble. A good processor is confident enough in their service that they don’t need to lock you into an iron-clad agreement.

- Poor Customer Support: Give their support line a call before you sign up. If you can't reach a knowledgeable human being when you're just a prospect, imagine how hard it will be when you have a real, urgent problem.

Taking the time to properly vet your options for high risk merchant processing is one of the smartest investments you can make. It protects your revenue, gives you stability, and sets you up for actual, sustainable growth.

Got Questions? Here Are Some Straightforward Answers

Diving into the world of high-risk merchant accounts can feel confusing, and it's natural to have a few questions. Let's clear up some of the most common ones so you can move forward with a solid plan.

Is Being Labeled "High-Risk" a Permanent Thing?

Not at all. Think of your high-risk status as a snapshot in time, not a life sentence for your business. It's a reflection of your current risk profile, and you absolutely have the power to change it.

The single most important thing you can do is get your chargeback ratio under control. If you can consistently keep your dispute rate below the 1% industry threshold for six to twelve months, you're sending a powerful message to your processor. It shows them your business is stable, well-run, and less of a liability. Tools like chargeback alerts, combined with top-notch customer service, are your best bet for making that happen.

Once you’ve built a solid track record of low chargebacks and steady processing, you'll be in a great position to go back to your provider and ask for better terms. You could even apply for a standard, low-risk account elsewhere.

What’s the First Thing I Should Do If My Merchant Account Gets Shut Down?

Getting your account terminated can feel like a punch to the gut, but you need to act fast. Don't panic—get strategic. The first step is to find out exactly why it was closed. The processor has to tell you, and it's usually due to too many chargebacks, breaking their rules, or a shift in their own risk policies.

With that information in hand, here's your game plan:

- Find a New Processor, ASAP: Start applying for a new high-risk merchant account right away. Don’t hide the fact that you were terminated. Be upfront about it and show them the concrete steps you've already taken to fix the root cause.

- Diagnose the Core Problem: If chargebacks were the issue, you need a rock-solid prevention plan in place before you apply. A new processor will want to see that you've learned from the experience.

- Audit Your Operations: Double-check that your marketing, products, and fulfillment all line up with the terms of service of any new processor you're considering. You can't afford to make the same mistake twice.

Losing an account is a serious wake-up call. But it's also a chance to rebuild your payment strategy on a much stronger foundation.

How Long Does It Take to Get Approved for a High-Risk Account?

Getting approved for a high-risk account definitely takes longer than it does for a standard one. A low-risk business might get the green light in 24 hours, but you should prepare for a more thorough review. The underwriting is just on another level.

You can think of high-risk underwriters as financial detectives. They're going to dig into your business model, comb through your credit history, analyze your past processing statements, and scrutinize your website. They need the full picture before they can sign off on the risk.

On average, you should expect the approval process to take anywhere from three days to two weeks. The final timeline really depends on a few things:

- How prepared you are: Having all your documents ready to go—bank statements, processing history, business license—can shave days off the process.

- Your industry: Niches like online gaming or firearms will always trigger extra scrutiny, which naturally takes more time.

- The processor's own efficiency: Some providers are just built to move faster than others.

The best thing you can do is be prepared and responsive. When they ask for something, get it to them quickly and accurately. This helps keep the process moving and gets you back to accepting payments without any more delays than necessary.

Ready to stop chargebacks before they start? Disputely integrates directly with alert networks to give you the power to refund a dispute before it becomes a costly chargeback. Protect your merchant account, eliminate reserves, and keep your payment processing secure by visiting https://www.disputely.com to see how it works.