How Do Chargeback Alerts Work? A Merchant Guide

Chargeback alerts are essentially an early warning system. When a customer disputes a charge with their bank, an alert gives you a heads-up before it escalates into a full-blown, official chargeback.

This gives you a critical, albeit short, window—usually 24 to 72 hours—to issue a refund and stop the dispute in its tracks. It's your chance to solve a problem before it actually becomes a problem for your business.

Understanding Chargeback Alerts and Why They Matter

Think of a chargeback alert as a smoke detector for your revenue. You get a warning at the first sign of trouble, giving you time to act before a fire (a formal chargeback) can cause serious damage to your merchant account.

Without alerts, you're flying blind. You might not learn about a customer's issue for weeks, and by then, it’s already a costly, formal dispute. An alert system flips that script entirely, letting you know the moment a cardholder raises a flag with their bank. This is what shifts you from a reactive, defensive position into a proactive, preventative one.

The Power of Proactive Resolution

The real magic of a chargeback alert is that it gives you a choice. Once you get that notification, you have a small window to resolve the issue directly, which almost always means issuing a refund. It sounds simple, but taking this one step achieves several critical goals:

- You avoid the formal chargeback entirely. The dispute is settled and never gets officially filed, which means it doesn't count against your precious chargeback ratio.

- You sidestep hefty fees. Processors love to tack on chargeback fees, often ranging from $20 to $100 per dispute. An alert lets you dodge that bullet.

- You protect your merchant account. Keeping your chargeback-to-sales ratio low is non-negotiable for staying in good standing with payment processors and avoiding penalties, or even account termination.

Merchants face all sorts of disputes, and understanding the common challenges in resolving Amazon chargeback disputes really drives home just how vital a good alert system is.

A proactive alert system isn't just about managing disputes; it's about preserving the health of your payment processing relationships, which are the lifeblood of any ecommerce business.

The difference between getting a heads-up via an alert and getting hit with a formal chargeback is night and day.

Chargeback Alert vs Formal Chargeback

Here's a quick comparison to highlight the key differences between receiving a chargeback alert and dealing with a formal chargeback.

| Attribute | Chargeback Alert | Formal Chargeback |

|---|---|---|

| Timing | Immediate (within 24-72 hours) | Delayed (weeks later) |

| Merchant Action | Issue a refund to resolve | Fight or accept (representment) |

| Impact on Ratio | None, the dispute is prevented | Counts against your ratio |

| Associated Fees | Small alert fee | High chargeback fees (often $20+) |

| Outcome | Customer is refunded, dispute closed | Complex, lengthy process with no guarantee of winning |

As you can see, the alert gives you control and a chance to mitigate damage, while the formal chargeback puts you on the defensive.

The impact of using pre-dispute notifications is real and measurable. Industry data shows that merchants using these systems can cut their chargeback cases by up to 33% compared to those who don't. You can dig into more chargeback prevention statistics to see the full scope. Ultimately, this simple shift from playing defense to offense can be the one thing that saves your revenue and your reputation.

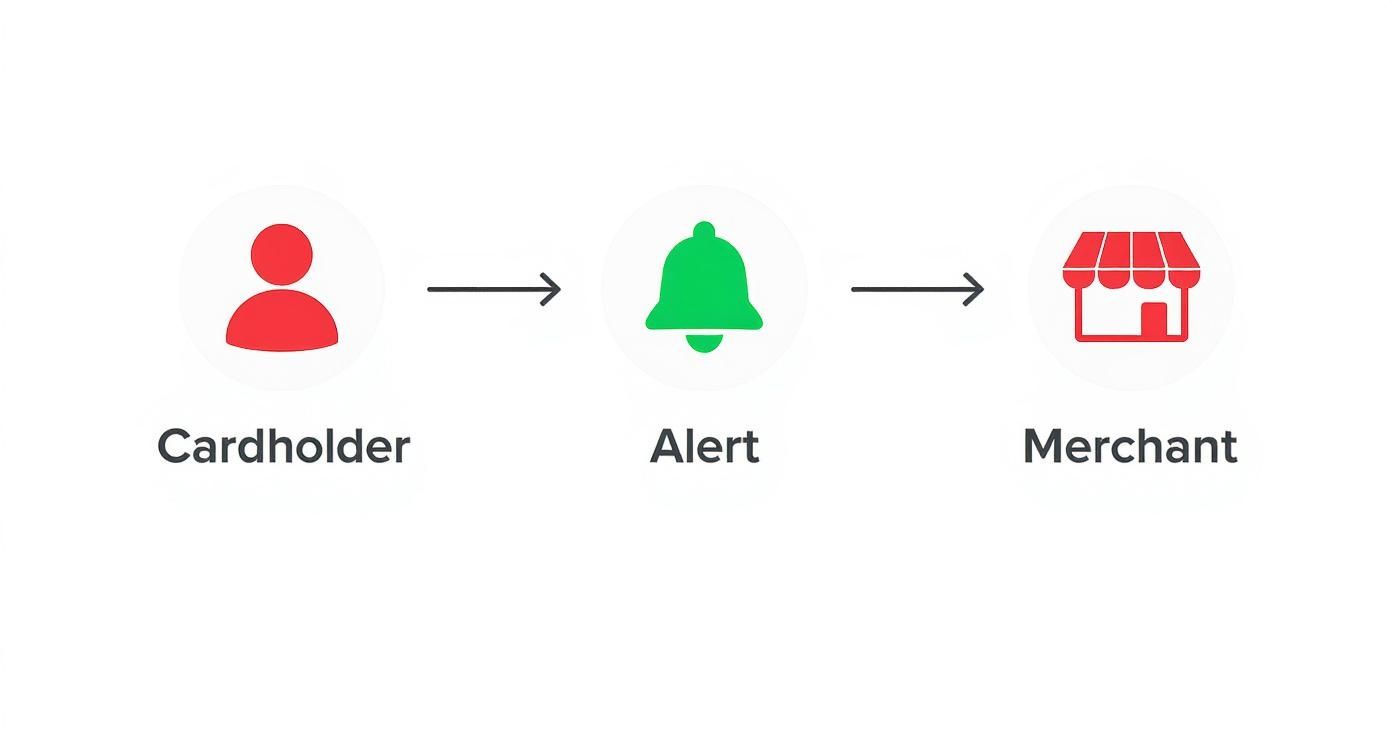

The Journey of an Alert from Bank to Merchant

So, how does a chargeback alert actually get to you? It’s a fascinating little journey that starts the second a confused or unhappy customer picks up the phone to call their bank.

Let's say someone sees a charge on their Chase or Bank of America statement they don’t recognize. Their first instinct is to report it. In the old days, this would immediately trigger a formal, painful chargeback process. But now, the bank sends up a digital flare first. This is the "pre-dispute" alert, and it's the critical difference between a minor headache and a major, costly problem.

This alert doesn't just magically appear in your inbox, though. It travels through a specific pathway, almost like a central nervous system for payment disputes. The route it takes depends on the card used.

- For Visa transactions, the alert travels through a system called the Chargeback Dispute Resolution Network (CDRN), which is run by Verifi.

- For Mastercard transactions, the signal goes through the Ethoca alert network.

These two platforms are the heavy hitters in this space. They work with thousands of banks around the world to create this early warning system that gives merchants a fighting chance.

From Network Silos to a Single Dashboard

Here’s where things can get complicated for a business owner. Since you almost certainly accept both Visa and Mastercard, you now have two separate streams of time-sensitive alerts coming from Verifi and Ethoca. Trying to monitor both is a recipe for disaster—it’s just too easy to miss one, and the window to act is tiny.

This is why third-party providers are so crucial. A service like Disputely plugs directly into both the Verifi and Ethoca networks, acting as a central hub that catches every single alert meant for your business.

An integrated alert system pulls all your dispute notifications into one place. This transforms a chaotic, multi-channel problem into a single, manageable workflow, ensuring you never miss the 24-72 hour window to act.

For any business, but especially those with a high volume of sales, this unified view is a game-changer. No more logging into separate portals or trying to make sense of different data formats. Everything you need is in one spot. It's a proactive step that helps you avoid the kind of issues that can lead to a dreaded Shopify payment hold.

This diagram breaks down the journey, showing how an alert flows from the cardholder all the way to you, the merchant.

As you can see, the system is designed to intercept a potential chargeback before it happens. It turns a formal dispute into a simple notification, putting you back in control of the situation.

By the time that alert hits your dashboard, it’s already been received from the network, identified, and matched to the exact transaction. And that’s when the clock officially starts ticking, giving you a brief opportunity to issue a refund and avoid the chargeback entirely.

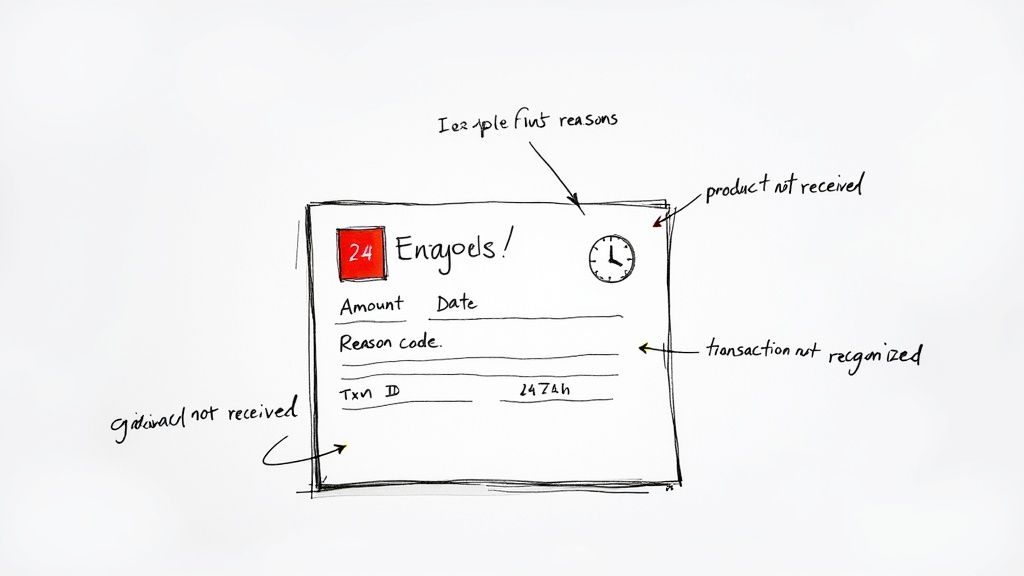

What’s Actually Inside a Chargeback Alert?

When an alert lands in your system, it’s more than just a red flag. It’s a complete case file on a specific transaction that's gone sideways, giving you a chance to fix things before they escalate into a full-blown chargeback. Learning to read these alerts is your first and best defense.

The whole point of an alert is to give you just enough information to find the original order and understand what the customer is claiming. The clock is ticking, though. You usually have just 24 to 72 hours to act before the window closes and the dispute automatically becomes a chargeback, dinging your record.

The Key Pieces of Information

Think of an alert as a snapshot of the transaction dispute. Every alert, regardless of the provider, will contain a core set of details to help you connect the dots.

Here’s what you can expect to find:

- Transaction Details: This is the basic stuff—the exact transaction amount, the purchase date, and typically the last four digits of the credit card. It’s everything you need to pull up the original order in your CRM or e-commerce platform.

- Customer Information: You’ll get the cardholder’s name, which helps you match the transaction to a customer account and review their order history.

- Dispute Reason Code: This is the most critical piece of the puzzle. The reason code tells you why the customer initiated the dispute in the first place.

That reason code is everything. It's the difference between a customer saying, "I never got the package," and, "I don't recognize this charge on my statement." Each reason points to a totally different problem—one might be a shipping issue, the other could be potential fraud—and dictates how you should respond.

An alert isn't just a signal to issue a refund. It's raw customer feedback. The dispute reason code gives you a direct look into a flaw in your customer's experience, offering a golden opportunity to fix not just this one order, but your entire process.

For example, if you suddenly see a lot of alerts with a "product not as described" reason code, it might be time to review your product photos or a specific supplier. This is how understanding what a chargeback alert is can turn a negative event into a powerful business insight.

A platform like Disputely organizes all this crucial information so you can see the whole picture at a glance.

Laying the data out clearly like this means you can make a quick, informed decision without losing valuable time hunting for information. You immediately know the reason, the amount at stake, and all the details needed to resolve the problem before that 24-hour deadline hits.

Automating Your Response to Protect Your Revenue

Getting a chargeback alert is just the first domino to fall. How you respond—and how quickly—is what really matters. In almost every case, the best move is to issue a fast refund to stop a formal chargeback from ever happening.

But let's be realistic. Manually reviewing every single notification is impossible, especially if you're dealing with any real volume. This is where automation becomes your secret weapon.

Smart merchants don't just react to alerts; they build intelligent, automated workflows to handle them. This hands-off approach guarantees the speed and consistency you need to act within that tight 24 to 72-hour window. It also frees up your team from mind-numbing, repetitive tasks so they can focus on the tricky customer issues that actually require a human touch.

This is the key to understanding how chargeback alerts work: they aren't just notifications. They're actionable triggers for an automated revenue protection system.

Setting Up Rules-Based Workflows

The most straightforward way to automate your response is with simple, rules-based logic. Think of it as creating a playbook for your system to follow. You set specific conditions, and if an alert meets them, it triggers an automatic refund. No questions asked.

This lets you build a custom defense strategy that fits your business model and risk appetite like a glove.

For instance, you could set up some really practical rules:

- Refund by Transaction Value: Automatically refund any alert for a transaction under a set dollar amount, say $30. When you factor in the alert fee and the lost revenue, it’s often cheaper than getting hit with a formal chargeback fee.

- Refund by Product Type: If you sell digital goods with virtually no fulfillment cost, you might create a rule to automatically refund all alerts tied to those products.

- Refund by Dispute Reason: Set up auto-refunds for specific reason codes, like "product not received," to sidestep drawn-out investigations into shipping problems.

These kinds of rules make sure that low-value or clear-cut disputes get resolved instantly, without anyone on your team lifting a finger.

Automation transforms your chargeback management from a reactive, time-consuming chore into a proactive, efficient system. It’s about making strategic decisions in advance so your platform can execute them flawlessly in real-time.

The Next Level: AI-Powered Decisions

While rules-based systems are a fantastic start, platforms like Disputely push things further by bringing AI into the mix. This unlocks a much more sophisticated and intelligent decision-making process that goes way beyond basic "if this, then that" logic.

An AI-driven system can look at a whole constellation of data points to make the best call in that moment.

Instead of just glancing at the transaction amount, an AI model might also weigh:

- Customer Lifetime Value (CLV): Is this a one-time buyer, or is this a loyal customer who has been with you for years? A strategic refund for a high-value customer is often a smart long-term play.

- Past Dispute History: Does this person have a habit of filing disputes? A recurring pattern could be a red flag for friendly fraud.

- Transaction Attributes: AI can sift through dozens of variables in seconds, from the card's BIN to the customer's location, to get a much clearer picture of the situation.

This level of analysis helps you sidestep refunding bogus claims while still taking great care of customers with legitimate problems. Because while alerts are great for preventing chargebacks, some disputes are actually worth fighting. Learning more about the chargeback representment process can help you figure out when it's time to stand your ground.

Ultimately, this smarter automation does more than just protect your revenue—it protects your valuable customer relationships, too.

5. Measuring the Real-World Benefits of an Alert System

Putting a chargeback alert system in place isn't just about managing a few annoying disputes. It’s a genuine investment that pays you back in very real, measurable ways. The benefits ripple across your business, touching everything from your bottom line and operational workload to your long-term stability.

The most immediate win? A dramatic drop in your chargeback-to-sales ratio. This is the one number that payment processors watch like a hawk. If that ratio starts creeping up—usually past the 0.9% mark—they start seeing you as a high-risk merchant. That’s when the trouble starts, from frozen funds to outright account termination.

Protecting Your Profitability and Reputation

When you get an alert, you have the chance to refund the customer before their bank officially files a chargeback. This is a game-changer. Since the dispute never formally enters the system, it never hits your ratio, keeping you in the clear with your payment partners.

This proactive move has a huge financial upside, too. Think about all the costs packed into a single chargeback:

- Lost Revenue: The full sale amount is immediately pulled from your account.

- Chargeback Fees: Processors add insult to injury with fees ranging from $20 to $100 per dispute.

- Operational Costs: Don't forget the hours your team sinks into digging up evidence and fighting a battle they might not win.

An alert system wipes the chargeback fee off the board and slashes the time wasted on manual review. Yes, you still refund the sale, but the cost of an alert is a tiny fraction of the cost of a full-blown chargeback.

An investment in chargeback alerts pays for itself by transforming unpredictable, high-cost penalties into predictable, low-cost operational expenses. It’s about safeguarding your revenue and reputation one prevented dispute at a time.

The True Cost of Inaction

Letting your dispute rate climb is simply not an option. As chargebacks pile up, the penalties get steeper, creating a domino effect that can easily derail a growing business.

To put it in perspective, let’s look at a side-by-side comparison of a business with and without a robust alert system.

Impact Analysis of Chargeback Alert Implementation

This table shows the projected improvements a merchant can expect across key metrics after implementing a chargeback alert system.

| Metric | Before Alert System | After Alert System | Percentage Improvement |

|---|---|---|---|

| Chargeback Ratio | 0.95% (High Risk) | 0.45% (Safe) | 52.6% |

| Chargeback Fees (Monthly) | $2,375 (at $25/fee) | $0 (Replaced by alert fees) | 100% |

| Revenue Lost to Disputes | $47,500 | $22,500 (Refunded via alerts) | 52.6% |

| Team Hours on Disputes | 40 hours/month | 5 hours/month | 87.5% |

| Account Stability | At risk of termination | Secure processing relationship | N/A |

The data is clear: the right alert system doesn't just manage a problem—it creates a more stable, profitable, and efficient operation.

Ultimately, understanding how chargeback alerts work is the first step toward building a more resilient business. They act as your first line of defense, protecting your ability to process payments and grow your company without the constant fear of being shut down. The return on investment isn't just about the money you save; it's about giving your business the security it needs to thrive.

Weaving Chargeback Alerts into Your Business

Getting a chargeback alert system plugged into your daily operations is probably easier than you imagine. Today's platforms are built to play nicely with the tools you already use, so you don't have to worry about commissioning a massive, custom-built project.

The Technical Handshake: APIs and Webhooks

The magic behind this connection boils down to two key pieces of tech: APIs (Application Programming Interfaces) and webhooks.

An API is like a dedicated, secure translator that lets your alert provider talk directly to your CRM or order management system. When an alert pops up, a webhook acts as an instant notification, pushing that information to your other systems. This can automatically trigger a workflow, like creating a new case file in your support software or updating a customer's record.

This real-time communication is the bedrock of keeping your financial house in order.

Keeping the Books Balanced: Data and Reconciliation

One of the most important parts of this whole process is data reconciliation. Think about it: when your system fires off an automatic refund in response to an alert, that action has to be recorded correctly across the board. If it isn't, you're setting yourself up for a massive accounting headache down the line. Your sales records will say one thing, but your bank statements will tell a completely different story.

When you're connecting any new system, it's vital to follow essential data integration best practices. This ensures every refunded dollar is accounted for, preserving the integrity of your financial reporting.

A solid alert platform will handle this automatically. It matches the alert to the original transaction and confirms the refund was successfully processed, creating a clean, closed-loop system with a clear audit trail.

The real goal of integration isn’t just getting an alert. It’s building an automated ecosystem where a dispute notification is received, acted on, and reconciled across every business system you have, all without a human lifting a finger.

Platforms like Disputely are designed for this kind of simplicity, often letting merchants connect their payment processor in just a few minutes. You can get a feel for how the right tools can streamline your workflow by checking out different chargeback prevention pricing models to find something that fits your business. A smooth setup means you’re up and running fast, protecting your revenue from day one.

Common Questions About Chargeback Alerts

Even after you get the hang of how chargeback alerts work, a few practical questions always pop up. Let's tackle the most common ones we hear from merchants.

Do Chargeback Alerts Stop Every Single Chargeback?

In short, no. Think of them as a highly effective shield, not an impenetrable force field.

Alerts are designed to catch disputes from banks that participate in the Visa (through Verifi) and Mastercard (through Ethoca) networks. They won’t catch disputes from other card brands like American Express or Discover, or from non-participating banks.

That said, they stop a huge chunk of potential chargebacks right in their tracks, making them one of the best tools you can have to protect your merchant account.

What’s the Difference Between an Alert and Representment?

It really comes down to being proactive versus reactive.

- A Chargeback Alert is your offense. It's a heads-up that lets you step in and solve a customer's issue before it escalates into a formal, damaging chargeback. The go-to move here is to issue a refund and close the loop.

- Representment is your defense. This happens after the chargeback has already hit your account. You're now in a reactive position, scrambling to gather evidence to prove the transaction was valid.

Alerts help you sidestep the entire representment headache from the get-go.

What's the Cost of a Chargeback Alert Service?

Pricing can vary, but you'll typically pay a small fee for each alert you receive. The key thing to remember is that this fee is a drop in the bucket compared to the cost of a full-blown chargeback.

A chargeback doesn't just cost you the lost sale. It also comes with a painful penalty from your processor (usually $20 to $100 per chargeback) plus all the time your team spends dealing with it.

When you look at the numbers, alert services pay for themselves many times over. The ROI isn't just about saving money on fees; it's about protecting your merchant account from being flagged as high-risk.

If I Get an Alert, Can I Still Fight the Dispute?

Technically, yes, but it defeats the whole purpose of the alert. The goal of an alert is to refund the customer to prevent a formal chargeback from ever being filed.

If you get an alert and decide not to refund, the bank will almost certainly move forward and file the chargeback. At that point, you're back to the standard representment process, and that dispute will now count against your chargeback ratio.

Stop letting preventable disputes drain your revenue. Disputely connects directly with Visa and Mastercard to stop chargebacks before they ever happen, keeping your merchant account safe and your profits secure. Learn how you can reduce chargebacks by up to 91%.