How to Dispute a Credit Card Charge A Merchant's Guide to Winning

As a merchant, fighting a credit card dispute means you're going on the offensive to prove a transaction was legitimate. This isn't just a simple refund request—it's a formal chargeback, and you have a limited window, usually just 20-45 days, to build your case.

Winning requires you to gather compelling evidence, write a solid rebuttal, and get everything submitted to the card network before that deadline hits.

What's Your Role When a Dispute Hits?

When a customer disputes a charge, it kicks off a formal process. For you, this is much more than a single lost sale; it's a direct hit to your revenue and, if it happens too often, your business's reputation with payment processors.

You're a key player in how this unfolds. If you ignore a chargeback, you automatically lose the money. But throwing together a weak, disorganized response isn't much better. To protect your bottom line, you need to be ready with a proactive, evidence-based game plan.

The Different Flavors of Credit Card Disputes

Not all disputes are the same. As a business owner, you'll run into a few common types, and knowing what you're up against is the first step to building a strong defense.

To make it easier to spot what you're dealing with, here’s a quick breakdown of the most common dispute types.

Common Types of Credit Card Disputes

| Dispute Type | What It Means | A Real-World Merchant Scenario |

|---|---|---|

| Legitimate Dispute | The customer has a valid reason to complain. The product was broken, never arrived, or wasn't what you described. | A customer orders a blue coffee mug, but you accidentally ship a red one. They have a valid reason to dispute the charge if you don't resolve it. |

| Criminal Fraud | A classic case of a stolen credit card being used for an unauthorized purchase. | Someone finds a lost credit card and uses it to buy $500 worth of electronics from your online store before the real owner can report it stolen. |

| Friendly Fraud | A legitimate customer makes a purchase but disputes it later. This can be accidental (they forgot about a subscription) or intentional (they want the item for free). | A customer buys a dress for an event, wears it, and then files a chargeback claiming "product not as described" to get their money back. |

Understanding these categories helps you immediately focus your efforts. A claim for "product not received" requires a completely different set of evidence than a claim of "transaction not recognized."

The most frustrating and fastest-growing category by far is friendly fraud. This is where a real customer, not a thief, disputes a perfectly valid charge. It could be buyer's remorse, confusion over a recurring bill, or someone deliberately trying to get something for free.

This isn't a small problem. Friendly fraud (or first-party misuse) now drives 21% of all disputes globally. It's the single biggest threat merchants face, fueling a staggering 70-75% of all chargebacks and costing U.S. businesses over $170 billion a year. You can dig into the latest chargeback data in Mastercard's 2025 report.

Here's the bottom line: Most of the disputes you'll fight won't be from shadowy criminals using stolen cards. They'll be from your own customers. That's exactly why having a rock-solid system for collecting and presenting evidence is non-negotiable.

Once you identify the type of claim, you can instantly pivot to gathering the right documentation to build a winning case and protect the revenue you worked so hard to earn.

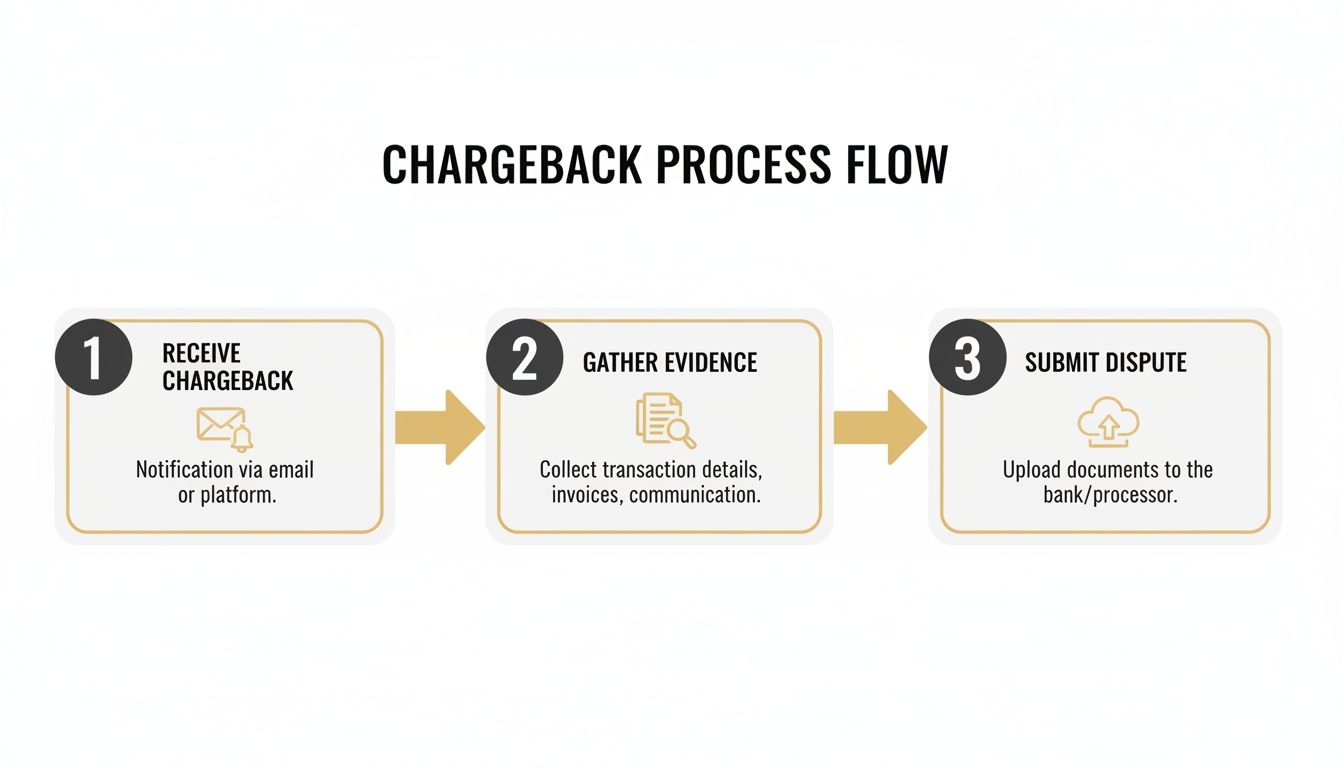

The Merchant Dispute Process from Start to Finish

That gut-punch feeling when a chargeback notification hits your inbox is all too familiar. But it’s not game over. A chargeback is just the beginning of a formal, time-sensitive process where you get to step up and defend the sale. Think of it as your chance to lay out the facts and prove the transaction was totally legitimate.

The whole thing kicks off the second that alert arrives. Your first move? Find the reason code. This little code, sent by the card network, is your roadmap. It tells you exactly why the customer is disputing the charge—maybe it's "product not received" or "transaction not recognized." Nailing down this code is everything, because it dictates the specific proof you need to start digging up.

This flowchart breaks down the basic flow from your side of the counter.

From that initial notification to submitting your evidence, every single step matters in building a rock-solid case.

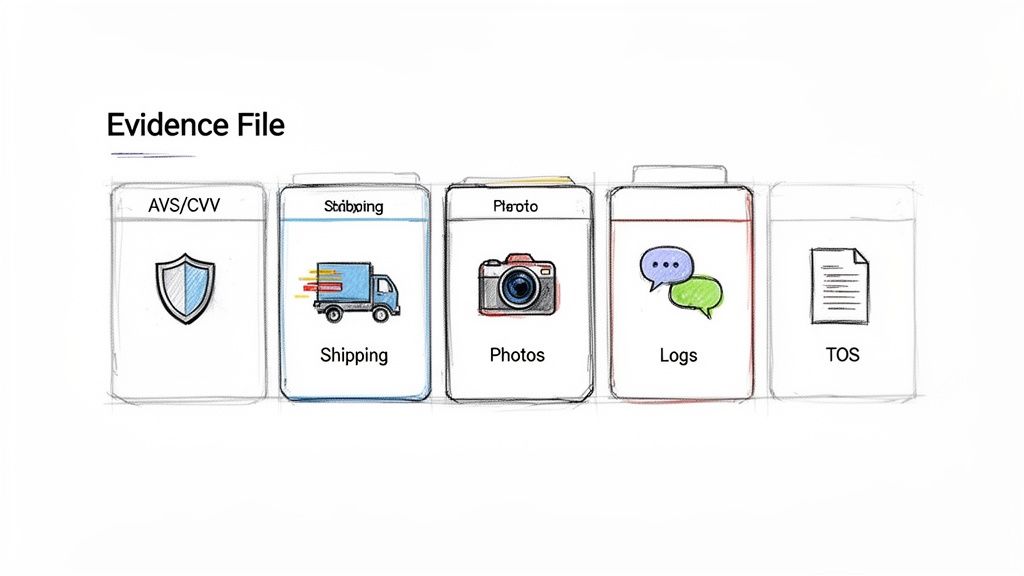

Gathering Your Compelling Evidence

Once you know the why behind the dispute, it's time to build your case file. This isn’t about just dumping every bit of data you have on the bank and hoping something works. It's about being strategic and collecting documents that directly punch holes in the customer’s claim.

For instance, if the reason code points to an unauthorized transaction, your best ammo will be:

- AVS and CVV Match Data: This shows the address and security code entered at checkout matched what the bank has on file. It's a huge validator.

- IP Address Geolocation: Can you show the purchase came from a location consistent with the cardholder's billing address? That's powerful.

- Customer Communication Logs: Pull any emails, chat transcripts, or call notes where the customer talked about their order before the dispute.

If the claim is "product not received," you’ll need a different set of evidence. Here, you have to prove the item got where it was going. You'll want time-stamped shipping confirmations, tracking numbers that clearly say "delivered," and if you have it, that golden delivery photo. Each piece should tell one clear, factual story: a valid purchase, successfully fulfilled.

Crafting a Winning Rebuttal Letter

Your evidence is the foundation, but the rebuttal letter is how you tell the story. This is your formal argument to the bank, and it needs to be clear, concise, and professional. You're guiding the reviewer through your proof, explaining exactly why the charge is valid. Leave emotion out of it; stick to the facts.

A solid rebuttal letter always follows a simple structure:

- Start with the basics: the chargeback case number and the disputed amount.

- Briefly summarize the transaction itself—date, time, what was ordered.

- Tackle the reason code head-on. Directly counter the customer's claim and explain how your evidence proves them wrong.

- Neatly list out your evidence, referencing each document you’ve attached.

Pro Tip: Write as if the person reading your letter has zero idea who you are or what this transaction was about. It needs to be so clear and well-supported that a complete stranger can follow the logic and agree with you.

Real-World Rebuttal Scenarios

Let's see what this looks like in practice.

Scenario 1: The DTC Fashion Brand A customer files a "product not received" chargeback for a $150 dress. Your rebuttal should lead with the shipping confirmation email. Follow that with the FedEx tracking info showing a "delivered" status with a timestamp. The knockout punch? A screenshot of the carrier's delivery photo showing the package sitting right on the customer's front porch.

Scenario 2: The SaaS Subscription Company A user disputes their $49 monthly fee, claiming they canceled. Your evidence package should include a screenshot of their original sign-up where they agreed to your terms, user activity logs showing they logged in after they claimed to have canceled, and a copy of your straightforward cancellation policy. Your letter will walk the bank through that timeline, proving the service was both active and used.

Meeting Critical Submission Deadlines

This entire process runs on a strict clock. Card networks like Visa and Mastercard typically give you a window of 20 to 45 days to get your response in. Miss that deadline, and you automatically lose. No exceptions.

That tight turnaround is where so many merchants trip up, especially if they’re handling disputes by hand. Success comes down to moving fast with detailed proof, like IP address matches or delivery confirmations.

For shops with any real volume, automation is a game-changer. Modern tools can connect to your payment gateway and use alert systems to stop disputes before they even turn into chargebacks. If you want to dive deeper into streamlining this, check out our insights on powerful representment strategies.

Staying organized and acting fast are your best weapons. The moment that dispute notice lands, the countdown begins. By having a clear, repeatable system in place, you can turn a frantic fire drill into a manageable workflow and drastically improve your odds of keeping your hard-earned revenue.

Building Your Irrefutable Evidence File

If you’re walking into a dispute with a weak or messy evidence file, you’ve already lost. You have to remember: the bank associate handling the case knows absolutely nothing about you, your business, or this specific order. Your goal is to hand them a file so clear, organized, and convincing that they can only come to one conclusion—the charge was legit.

This isn’t about just dumping every piece of data you have on them and hoping something works. A winning rebuttal is a surgical strike. Every single piece of evidence you provide needs to directly dismantle the customer's claim.

Tailor Your Evidence to the Dispute Type

The reason code is your road map. It tells you exactly what you need to prove. Let's dig into the essential documents you’ll need for the most common disputes you're likely to see.

When a customer claims "Product Not Received," your mission is straightforward: prove you delivered it. The more proof you have, the better. Your absolute must-haves are:

- Time-Stamped Shipping Confirmation: The email you sent the customer when the order shipped, clearly showing the date and the exact address it was heading to.

- Complete Tracking Information: A screenshot or PDF from the carrier (like USPS or FedEx) that details the package’s journey and, most importantly, shows a final "Delivered" status.

- Proof of Delivery Photo: This is your silver bullet. A photo from the carrier showing the package sitting on the customer's doorstep makes it nearly impossible for them to argue they never got it.

Without these core items, it's just your word against theirs, and banks almost always side with their cardholder in that scenario. A crucial part of your evidence file is always a detailed transaction record; learn how to create a flawless itemized receipt template to build a stronger case from the very beginning.

Proving a Transaction Was Authorized

When the claim is "unauthorized transaction" or straight-up "fraud," your focus shifts entirely. You're no longer proving delivery; you’re proving the right person made the purchase.

Your evidence needs to connect the dots between the person, their credit card, and the device they used to place the order.

- AVS and CVV Match Data: Show that the Address Verification System (AVS) and the three-digit Card Verification Value (CVV) they entered at checkout matched the bank’s records. This is one of the single strongest indicators of a legitimate purchase.

- IP Address Geolocation: Provide the IP address the order came from and show how it matches the customer’s billing or shipping city and state.

- Customer Communication: Did they email you? Use live chat? Open a support ticket? Include transcripts of any communication where they discussed the order before the dispute. If they asked a question about their product, they were implicitly acknowledging they bought it.

Key Takeaway: A mismatch in AVS data or an IP address from another country can be a red flag. But when you have a perfect match across AVS, CVV, and IP location, you’ve built a powerful defense against fraud claims.

Defending Subscription and Digital Good Disputes

Disputes over recurring charges and digital products are a different beast. For these, it's all about proving the customer agreed to your terms and actually used the service or product.

For a subscription business fighting a "canceled but still charged" claim, you'll need to show:

- Proof of Agreed Terms: A screenshot of your checkout page where the customer ticked a box agreeing to your subscription terms and cancellation policy.

- Usage and Login History: Data logs are your best friend here. Show that the customer logged into their account or used your service after the date they claim they canceled.

- Cancellation Policy: Include a clear copy of your cancellation policy that outlines the required steps, which the customer obviously failed to follow.

If you sell digital goods like an e-book or software, evidence of access is everything. Show records that the download link was clicked or that the user account logged in to get the product. These digital footprints are your version of a delivery confirmation.

Building a solid case takes time and diligence. For merchants looking to tighten up their process, our guide on how to https://disputely.com/campaign/q4-audit can help you spot patterns and strengthen your evidence-gathering strategy. When you methodically collect the right documents for each specific claim, you can turn a potential loss into a winnable case.

Why Prevention Is Your Most Powerful Strategy

Fighting individual disputes is a necessary evil, but it’s a defensive game you can’t always win. A truly resilient business knows the best way to handle a chargeback is to stop it before it even happens. It’s time to shift your focus from playing defense to going on offense—it’s not just a smarter move, it's essential for your long-term survival.

The real sting of a chargeback isn't just the lost sale. For every single dispute, you're hit with non-refundable fees from your payment processor, typically anywhere from $15 to $100. Worse yet, each one chips away at your merchant account's health by driving up your dispute ratio. If that number gets too high, you’re looking at account holds, steeper processing fees, or even losing your ability to accept credit cards altogether.

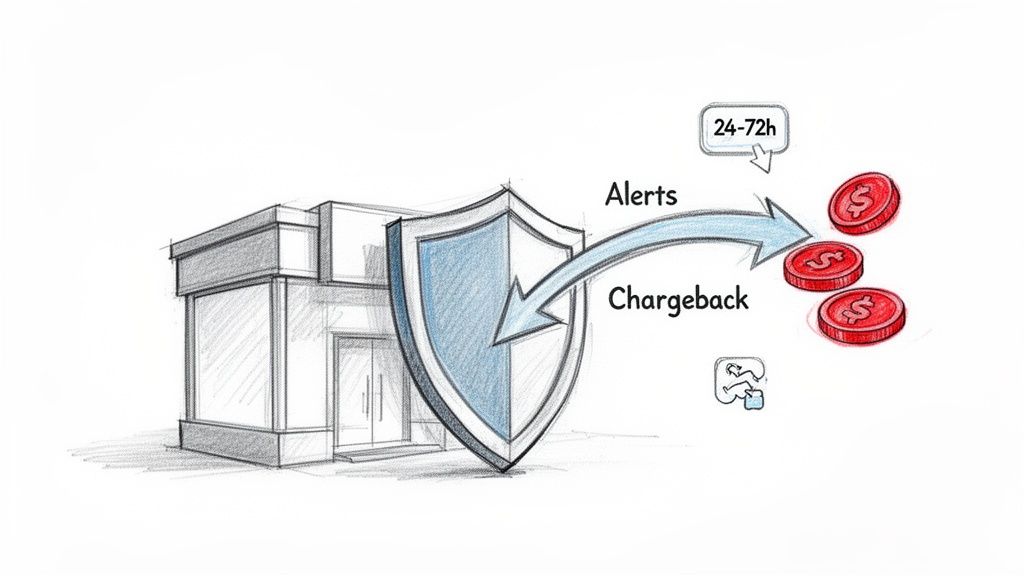

Unlocking the Power of Chargeback Alerts

This is where modern chargeback alert and deflection technologies completely change the game. Systems like Visa's Rapid Dispute Resolution (RDR) and Mastercard's Consumer Dispute Resolution Network (CDRN) are designed to give you a critical heads-up. Instead of being blindsided by a formal chargeback that's already in motion, these networks notify you the moment a customer contacts their bank.

This alert opens up a crucial 24-72 hour window to act before the issue escalates into a damaging chargeback on your record. Think of it as your chance to intercept the problem and solve it directly, completely sidestepping the formal, expensive dispute process.

The Takeaway: Chargeback alerts transform a lengthy, evidence-based battle into a simple, proactive fix. You’re no longer fighting to win back money; you're preventing the fight from ever starting.

This brief window is your most powerful tool. It allows you to issue a refund for the transaction, which immediately satisfies the customer's bank and stops the chargeback cold. While no one likes refunding a sale, it’s infinitely better than taking a hit from a chargeback fee, a mark against your dispute ratio, and likely losing the revenue anyway.

The Strategic Refund: A Proactive Defense

Issuing a refund through an alert system isn't admitting you did something wrong—it's a calculated business decision. You’re protecting your vital dispute ratio, dodging expensive fees, and keeping your payment processing relationships on solid ground. This is especially important for merchants on platforms like Shopify, where a high dispute rate can trigger frustrating and costly payment holds. If you're in that boat, our guide to resolving Shopify payment holds offers a deep dive.

The difference between a reactive and proactive approach is stark. Fighting chargebacks is a costly, time-consuming gamble with no guarantees. Preventing them saves money, protects your merchant account, and frees you up to focus on growing your business.

Reactive Disputing vs Proactive Prevention

| Factor | Reactive Disputing | Proactive Prevention |

|---|---|---|

| Cost | Lost revenue + chargeback fees ($15-$100 per dispute) | Cost of refund + alert service fee (usually much lower) |

| Dispute Ratio | Every chargeback increases your ratio, risking your account | Refunds via alerts do not count against your dispute ratio |

| Time Investment | Hours spent gathering evidence and writing responses for each case | Minutes to review an alert and issue a refund |

| Success Rate | Merchants win only about 45% of disputes on average | 100% success rate in preventing the chargeback from happening |

| Outcome | Potential win, but still a mark on your record and lost time | Protects merchant health, avoids fees, and maintains stability |

Ultimately, the numbers don't lie. A prevention-first mindset is becoming non-negotiable.

Global chargeback volumes are projected to hit a staggering 261 million in 2025 and continue climbing to 324 million by 2028. Considering merchants only win about 45% of their disputes, often due to weak evidence or slow responses, you can’t afford to just react.

Tools like Disputely integrate directly with Visa's RDR and Mastercard's CDRN, giving you those critical 24-72 hour alerts. This allows you to proactively refund and stop chargebacks dead in their tracks, potentially slashing your ratio by up to 99%. You can discover more insights about these chargeback trends and see just how big the problem is getting.

By adopting prevention as your primary strategy, you stop putting out fires and start building a firewall. It’s an investment that pays for itself over and over by protecting your revenue, cutting operational headaches, and securing the long-term health of your business.

A Pro-Level Playbook for High-Risk and High-Volume Merchants

When you're processing thousands of transactions a month or you're in what's considered a "high-risk" industry, the standard advice for handling disputes just doesn't cut it. The stakes are simply higher. For you, a sudden spike in chargebacks isn't just a minor headache; it's a direct threat that could land your business in a very expensive monitoring program with a card network.

For merchants at this scale, dispute management has to evolve from a reactive, case-by-case task into a full-blown data operation. The goal is to spot patterns, use your resources wisely, and protect the long-term health of your merchant account. It requires a much more sophisticated approach.

Keep a Hawk's Eye on Your Chargeback Ratio

Your chargeback-to-sales ratio is the single most important number for your payment processing health. It’s the metric Visa and Mastercard use to decide if you’re a risky business to work with. Once you cross their magic number—usually around 1%—you’re in the danger zone. That’s when you risk getting put into their monitoring programs, which come with painful fines and a whole lot of scrutiny.

Don’t wait for your monthly statement from your processor to see where you stand. High-volume merchants need to track this ratio in real-time. Use dashboards and analytics tools to see how your dispute rate is trending from one week to the next. This kind of vigilance means you can spot a problem, like a wave of friendly fraud targeting a new product, and jump on it before it gets out of hand.

Use Dispute Data to Find the Hidden Story

Think of every dispute you get as a clue. A single chargeback might not mean much, but what about 50 chargebacks from the same city with the same reason code? That’s not a coincidence; that’s a signal that something is fundamentally wrong.

Start digging into your dispute data to look for trends:

- Geographic Hotspots: Are you getting slammed with fraud claims from one particular country or state? You might be the target of a coordinated fraud ring.

- Problem Products: Is one specific SKU racking up "not as described" disputes? This could be anything from a misleading product description or a quality control problem to an entire defective batch.

- Subscription Confusion: If you run a subscription business, are most of your disputes happening around the first or second renewal? That's a classic sign that your customers don't understand your billing terms or find it too difficult to cancel.

By treating your chargebacks as business intelligence, you can go beyond just fighting them and start fixing the root cause. This not only helps you figure out how to dispute a credit card charge more effectively but also stops future ones from ever happening.

As you scale up and chase more sales, perhaps by optimizing your store with Amazon SEO services, managing disputes well becomes a cornerstone of your strategy. More visibility and more sales will naturally bring a higher risk of disputes, making this kind of data-driven prevention absolutely critical.

Get Smart with Filtering and Automation

At scale, you simply can't afford to fight every single battle. Having your team spend hours manually gathering evidence for a $10 dispute is a terrible use of their time. This is where intelligent filtering and automation can be a total game-changer.

The strategy is actually pretty simple: make automated decisions based on the dispute's value and your odds of winning.

- Auto-Refund the Small Stuff: Set up a rule to automatically refund any dispute below a certain amount, like $25. It stings to let it go, but you're saving money on the labor it would take to fight it, not to mention avoiding a potential chargeback fee if you lose.

- Flag the Big, Winnable Fights: On the flip side, automatically flag disputes over a higher threshold—say, $200—where you have solid evidence like delivery confirmation and AVS matches. These are the cases where your team should be spending their time and energy.

- Analyze the Middle Ground: For those disputes in between, let data guide you. If it's a claim from a repeat customer or a reason code you have a history of losing, a quick refund might be the smartest financial move.

This tiered approach ensures your resources are going where they'll make the biggest difference to your bottom line. It turns chargeback management from a chaotic, fire-fighting process into a streamlined, strategic part of your business.

Got Questions About Chargebacks? Let's Clear Things Up.

Even after you've got a game plan, a few questions always pop up about the chargeback process. It's a confusing world. Let's walk through some of the most common sticking points for business owners and get you some straight answers.

How Much Time Do I Really Have to Respond?

This is one of those deadlines you can't afford to miss. Officially, the card networks usually give you somewhere between 20 to 45 days to respond once a chargeback is filed. But let me be clear: treating this as your full window to work with is a huge mistake.

Waiting until day 44 to scramble for evidence is a recipe for disaster.

The quicker you can pull together a solid, evidence-backed response, the better your chances are. If you blow past that final deadline, you automatically lose. End of story. This is exactly why getting an early heads-up from an alert system is a game-changer—it buys you precious time.

Is a Chargeback Just a Fancy Word for a Refund?

Not even close. While the customer gets their money back in both scenarios, the impact on your business couldn't be more different.

- A refund is something you control. It's a customer service gesture, a direct agreement between you and the buyer.

- A chargeback is a forced reversal. It's initiated by the customer’s bank, and it's something happening to you, not by you.

Chargebacks are infinitely more damaging. They slap you with extra fees, ding your chargeback ratio, and can even put your entire merchant account at risk if your rate gets too high. By issuing a refund when you get an alert, you stop the dispute in its tracks before it ever becomes a damaging chargeback on your record.

Think of it this way: A refund is a cost of doing business. A chargeback is a penalty that tells your payment processor you're a risky partner. Grasping that difference is vital for staying in business long-term.

I Have Proof of Delivery. Can I Still Lose the Dispute?

Yes, and this is a tough one for many business owners to accept. Proof of delivery is your single best weapon against a "product not received" claim, but it’s completely useless against other types of disputes.

For instance, a customer can get their package and still file a chargeback claiming:

- Product Not as Described: They got the box, but argue the item inside wasn't what they thought they were buying.

- Defective Merchandise: The product showed up, but they say it was damaged or doesn't work.

- Transaction Not Recognized: They might not remember buying it, even if your product is sitting on their kitchen counter.

I’ve seen cases where merchants provide airtight evidence, and the issuing bank still sides with its cardholder. It’s frustrating, but it’s the reality of the system. This is why you need more than just one line of defense. You need clear product pages, responsive customer service, and a proactive system to head off disputes before they start. Winning the fight isn't just about knowing how to dispute a credit card charge—it's about preventing it from ever happening.

Ready to stop fighting fires and build a firewall against chargebacks? Disputely integrates directly with card network alert systems to notify you of disputes before they become costly chargebacks. Protect your revenue and your merchant account. See how much you can save at https://www.disputely.com.