How to Stop Chargebacks and Protect Your Revenue

If you want to get a handle on chargebacks, you have to think about prevention first.It’s a complete mindset shift—moving away from just reacting to disputes as they pop up and toward a more proactive strategy that stops them before they even start. This all begins with creating a crystal-clear and secure experience for your customers, from the moment they hit checkout to the second their package arrives.

The True Cost of a Single Chargeback

When you see a chargeback notification, that initial transaction amount is just the tip of the iceberg. The real damage runs much deeper, creating a ripple effect that touches almost every part of your operation.

For starters, every single dispute comes with a non-refundable administrative fee slapped on by your payment processor. These fees can sting, usually falling somewhere between $20 and $100 per incident.

On top of the fees, you're also out the physical product (if you've already shipped it), the money you spent on shipping and handling, and whatever marketing dollars it took to get that customer in the door. These costs stack up fast and can easily turn a profitable month into a loss.

The Hidden Operational Drain

The financial hit is bad enough, but what about the time suck? Think about the hours your team pours into fighting each dispute. Someone has to track down all the evidence, draft a compelling rebuttal, and navigate the whole representment process. That’s valuable time stolen from tasks that actually grow your business, like customer service or marketing.

A single $50 chargeback can easily cost over $200 when you factor in administrative fees, lost goods, shipping expenses, and the hours your team spends fighting it. It's a significant drain on resources that many merchants underestimate.

And this problem is only getting bigger. Global chargeback volumes are projected to skyrocket to 337 million cases by the end of 2025. This surge is fueled by the rise of card-not-present (CNP) transactions, which now make up 63% of all sales for merchants worldwide. For businesses here in the U.S., the math is brutal: for every $1 lost to chargebacks, the true cost averages out to a whopping $4.61 when you add up all the associated expenses.

To really bring this home, let’s look at the costs that aren’t immediately obvious.

The Hidden Costs Beyond a Single Lost Sale

This table breaks down the various direct and indirect financial impacts a merchant faces with every chargeback, illustrating why the true cost is much higher than the transaction amount.

| Cost Category | Description | Average Financial Impact (Example) |

|---|---|---|

| Transaction Amount | The original sale amount that is reversed. | $50.00 |

| Chargeback Fee | A non-refundable penalty from the payment processor. | $25.00 |

| Product Cost | The wholesale or manufacturing cost of the lost goods. | $20.00 |

| Shipping & Handling | The cost to pack and ship the item to the customer. | $10.00 |

| Operational Labor | Time spent by your team investigating and fighting the dispute. | $75.00 (e.g., 3 hours at $25/hr) |

| Marketing CAC | The prorated Customer Acquisition Cost for that one sale. | $30.00 |

| Total True Cost | The sum of all direct and indirect losses. | $210.00 |

As you can see, the expenses go far beyond the initial sale, turning a small dispute into a significant financial liability.

A Real-World Scenario

Imagine you run a subscription box company. Your dispute ratio has been hovering around a manageable 0.5%, but over one quarter, it creeps up to 1.2%. At first, you might not panic. But then you get an email from your payment processor. They're placing a hold on your account and threatening to shut you down completely. Suddenly, your entire business is at risk of not being able to process payments at all.

This scenario isn't just a hypothetical; it's the ultimate cost of unchecked chargebacks—losing your merchant account. Once your dispute ratio crosses the thresholds set by card networks like Visa and Mastercard, you can be forced into monitoring programs with hefty fines, and eventually, have your account terminated.

Understanding these financial realities is the first step toward building a more resilient business. Preventing disputes isn't just about saving a few sales here and there; it’s a critical part of sustainable growth. For any merchant trying to protect their bottom line, learning how to save money in business means getting serious about chargeback prevention.

Building Your First Line of Defense

The best way to win a dispute is to stop it from ever happening. Seriously. This isn't about fancy software; it’s about shoring up your business with proactive, common-sense tactics that build trust and leave no room for confusion.

Think about it: a lot of chargebacks, especially the "friendly fraud" kind, aren't born from malice. They often start with a simple misunderstanding. A customer scans their credit card statement, sees a charge from a name they don't recognize, panics, and calls their bank. That's a problem you can solve before it even starts.

Start with Crystal-Clear Communication

Your first job is to make sure every single piece of customer-facing information is precise, honest, and easy to find. Any vagueness is just asking for a dispute down the line.

Your product descriptions need to be brutally honest. Selling clothes? Include detailed sizing charts, fabric composition, and plenty of high-res photos from every angle. If you sell electronics, you have to be specific about the condition. For instance, clearly understanding refurbished phone standards and communicating that to your customers can head off "product not as described" claims before they're ever filed.

Next up is your return policy. Don't bury it. Link it clearly in your website’s header, footer, and on every single product page. Use plain English, not legalese, to spell out:

- The return window: How many days do they have to start a return?

- The required condition: Does the item need to be sealed, or is lightly used okay?

- The refund process: Will they get store credit, or will the money go back to their original payment method?

- Who pays for shipping: Make it obvious if the customer is on the hook for return shipping costs.

A transparent, easy-to-find return policy is a pressure-release valve. When customers see a clear path to a refund, they’re far less likely to hit the nuclear option—a chargeback—out of sheer frustration.

Finally, take a hard look at your billing descriptor. This is that little line of text that shows up on a customer's credit card statement, and it's one of the most underrated tools in your prevention toolkit. Ditch the generic legal company name nobody recognizes. A great format is YOURBRAND*PRODUCT CUSTSUPPORTPHONE#. It’s instantly recognizable.

Make Your Customer Support Easy to Find

When a customer runs into a problem, they need to reach a real person without having to go on a scavenger hunt. Hiding your contact info is a guaranteed way to send them straight to their bank. Make sure your customer service email, phone number, and a contact form link are prominently displayed on every page.

Speed matters, too. You should aim to acknowledge every single customer inquiry within 24 hours. Even a simple automated reply that says, "We got your message and we're on it," can completely de-escalate a tense situation. It tells the customer they've been heard and that help is on the way.

Implement Essential Fraud Detection Tools

While clear communication tackles customer confusion, you still need the right tools to weed out actual criminal fraud. These security checks are standard practice for a reason—they protect both you and your legitimate customers.

At a minimum, you should have the basics covered:

- Address Verification Service (AVS): This just checks if the billing address the customer entered matches what the credit card company has on file. A mismatch is a classic red flag.

- Card Verification Value (CVV): Always require the three- or four-digit code from the back of the card. This proves the customer physically has the card, stopping many fraudsters who only have a stolen card number.

For an even stronger defense, implement 3D Secure 2.0. This adds an extra authentication step where the bank asks the customer to verify themselves, usually with a one-time code sent to their phone. Here’s the best part: once a transaction is approved through 3D Secure, the liability for any fraud-related chargebacks often shifts from you to the card-issuing bank.

Getting these preventative measures right is crucial. When your operations are tight and transparent, you're much less likely to face issues that can get your account restricted. For merchants on Shopify, a sudden spike in disputes can trigger a payment hold. Knowing what causes a Shopify payment hold and how to resolve it really underscores why this first line of defense is so vital for keeping your business healthy.

Using Real-Time Alerts to Deflect Disputes

Moving from prevention to real-time interception is a massive leap forward in the fight to stop chargebacks. While your proactive measures are great for handling customer confusion, think of alert networks as your tactical response team—they jump in the second a customer starts a dispute with their bank.

These networks are essentially a direct line of communication between issuing banks and merchants like you. Instead of a dispute getting bogged down in the traditional, painfully slow chargeback process, these systems give you a critical heads-up. This allows you to resolve the customer’s issue on the spot, deflecting the dispute entirely before it ever blemishes your record as an official chargeback.

Understanding the Golden Window of Opportunity

Here’s how it works. When a customer calls their bank to question a charge, an alert gets fired off through networks like Visa’s Rapid Dispute Resolution (RDR), Mastercard’s Consumer Dispute Resolution Network (CDRN), or a third-party service like Ethoca. This alert opens up what we call the "golden window"—a tight timeframe of about 24 to 72 hours.

This window is your one and only chance to act. By pushing a refund through during this period, you satisfy the customer, and the bank closes the inquiry. The result? The dispute is gone, and no chargeback gets filed. Your dispute ratio stays clean, protecting your merchant account from painful penalties.

If you miss this window, the dispute goes down the old-fashioned path. It becomes a formal chargeback that hurts your processing relationship and costs you time and money, no matter who wins in the end.

How Alert Networks Actually Work

Think of these networks as an automated early-warning system. Instead of waiting weeks for a chargeback letter to show up, you get a notification almost instantly. When managed through a dedicated platform, the whole process is incredibly slick.

- A Dispute is Initiated: A cardholder contacts their bank about a transaction they don't recognize or agree with.

- An Alert is Created: The bank, which is plugged into an alert network, generates a notification about the potential dispute.

- The Merchant is Notified: Your chargeback management platform gets pinged with this alert in real-time.

- A Refund is Issued: Based on rules you’ve already set up, the system can automatically issue a refund to the customer.

- The Dispute is Closed: The bank sees the refund, considers the issue resolved, and stops the chargeback in its tracks.

This all happens behind the scenes, often without anyone on your team having to do a thing. For any merchant trying to figure out how to stop chargebacks at scale, this is a non-negotiable strategy.

By intercepting a dispute with a timely refund, you're not just giving money back. You're paying a small price to protect your most valuable asset: your ability to process payments without interruption.

Automating Your Defense with Smart Rules

The real magic of alert networks happens when you bring in automation. Trying to manage these alerts manually is a recipe for disaster for any business with decent sales volume. The smart move is to connect a platform to your payment processor—like Stripe, PayPal, or Shopify Payments—and set up some smart refund rules.

These rules give you total control over which disputes you deflect automatically. You can build them around all kinds of data points, for instance:

- Transaction Amount: Automatically refund any dispute under $50. The cost of the refund is almost always less than the chargeback fee and the time you'd spend fighting it.

- Product Type: You might decide to always refund disputes for digital products, since there’s no physical item to get back anyway.

- Customer History: Maybe you set a rule to immediately refund first-time customers to keep them happy, but flag alerts from someone who has disputed before for a manual review.

Once these workflows are in place, you can stop the majority of your chargebacks without lifting a finger. It frees up your team to focus on legitimate customer service issues and fight the high-value disputes that are actually worth your time.

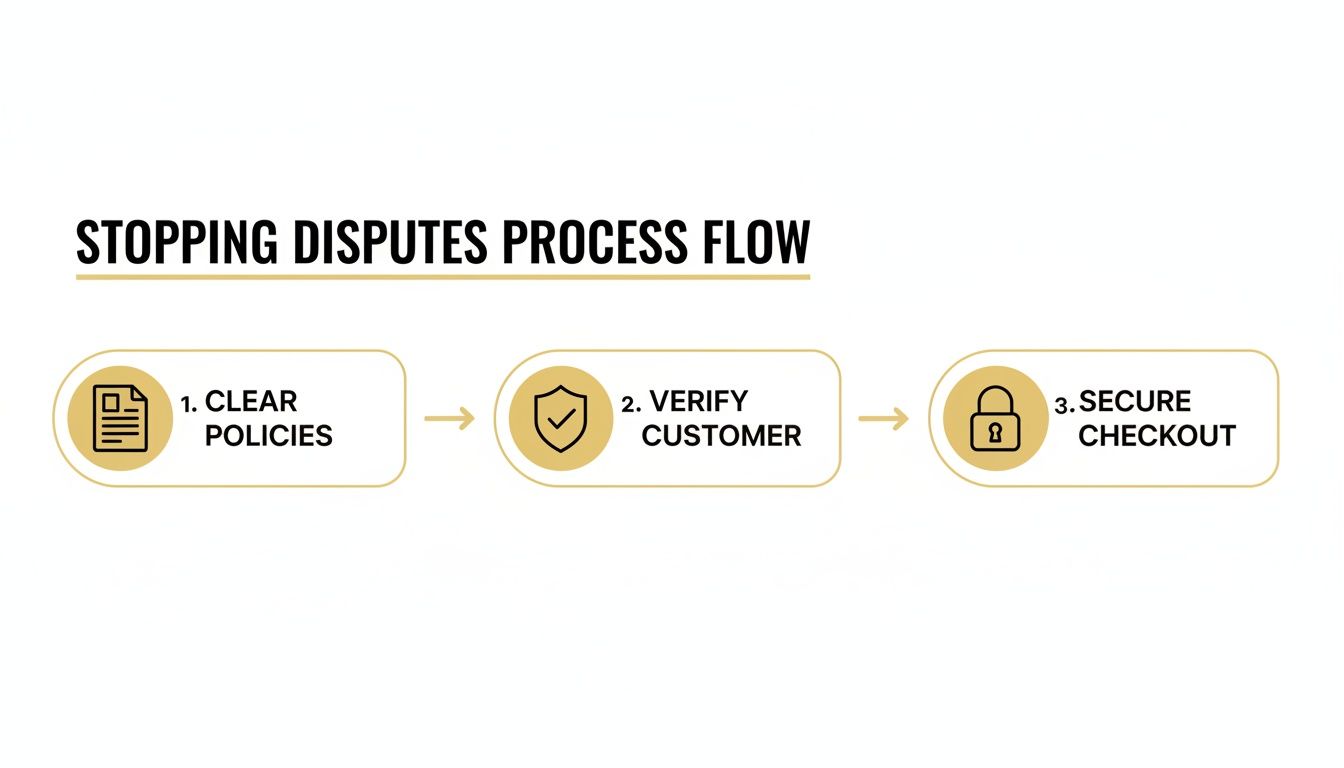

This three-step flow shows how all your proactive measures should work together to stop disputes before they ever get out of hand.

The key takeaway here is that a layered defense is always best. When you combine clear policies with solid customer verification and a secure checkout, you create the perfect foundation for advanced tools like real-time alerts to do their job effectively.

The Global Impact of Chargebacks and Alerts

The need for this kind of tech is obvious when you look at the global trends. Chargeback rates are all over the map; while the global average is around 0.65%, that number hides some wild regional differences. Brazil, for example, sees rates as high as 3.48%, while Japan sits at a tiny 0.18%. For any merchant, especially those in high-risk industries, letting your chargeback ratio creep over 1% can lead to big fines or even account termination.

The e-commerce boom has caused a 222% spike in chargebacks related to shipping delays and fraud. But the upside of prevention is huge. Alert systems are a direct counter to the rising tide of chargeback fraud, which is on track to cost businesses $28.1 billion by 2026. You can find more eye-opening chargeback statistics on Chargebacks911.

Fighting Back with Smart Representment

Even with the best prevention and alert systems in place, some disputes will inevitably slip through. When that happens, especially when you suspect friendly fraud, you have a choice to make: accept the loss or fight back.

This process is called representment. It’s your official rebuttal to a chargeback, where you present compelling evidence to the customer’s bank to prove the transaction was completely legitimate.

But let’s be clear—the goal isn't to fight every single dispute. Contesting a $15 chargeback almost never makes sense when you factor in the operational cost. The real key is developing a smart, data-driven strategy to pinpoint which disputes are actually winnable and worth your team's time.

Friendly fraud is a massive headache for merchants. It's now the second most common type of fraud, with merchants currently labeling a staggering 45% of their chargebacks as fraudulent. With global chargeback losses projected to surge by 23% to $41.69 billion by 2028, knowing when and how to fight back is more critical than ever. You can discover more insights about these dispute trends from Sift.

Gathering Your Compelling Evidence

To win a representment case, you need to build an airtight argument backed by clear, indisputable evidence. The issuing bank doesn't know you or your business; all they see is the information you provide. Your job is to paint them a crystal-clear picture of a valid transaction.

The evidence you'll need depends on what you sell and the specific reason code for the chargeback.

For Physical Products:

- Proof of Delivery: This is non-negotiable. You need shipping confirmation with a tracking number showing the package was delivered to the cardholder's verified address.

- Order Confirmation: Pull together the original receipt, email confirmations, and any other communication you had with the customer.

- AVS and CVV Matches: Show that the Address Verification Service (AVS) and Card Verification Value (CVV) checks passed during checkout.

For Digital Goods or Subscriptions:

- Usage Logs: This is your digital proof of delivery. Show IP logs, download records, or account activity that proves the customer accessed or used the service.

- Terms of Service Agreement: Provide proof that the customer checked a box agreeing to your terms, especially your cancellation and refund policies, when they bought it.

- Customer Communications: Include any support tickets, emails, or chat logs where the customer discusses the product. This proves they received it and engaged with it.

Think of your evidence packet as a legal brief. It should be so thorough and well-organized that it leaves the bank with no other option but to rule in your favor. Every piece of data strengthens your case.

Making Data-Driven Decisions on What to Fight

As you pull your evidence together, you also need a system for deciding which battles are worth picking. A good rule of thumb is to weigh the transaction value against your historical win rate for that specific type of dispute.

Start tracking your representment win rate. If you find you're consistently winning "product not received" disputes for items under $100 but always losing "not as described" claims, you know exactly where to focus your energy. This kind of data-driven approach stops you from wasting resources on lost causes and maximizes the revenue you can actually recover.

Building a solid strategy around representment can feel overwhelming, but it's a vital skill for protecting your bottom line. To go deeper, you can also explore our complete guide to mastering chargeback representment for more advanced tactics.

A Practical Checklist for Your Rebuttal Letter

When you submit your evidence, you’ll bundle it all with a formal rebuttal letter. This letter needs to be concise, professional, and easy for a bank employee to scan. It’s your chance to summarize your case and guide them through your evidence.

Your letter should always include these four things:

- A clear introduction stating your intent to challenge the chargeback.

- A point-by-point refutation of the cardholder's claim.

- A chronological list of the evidence you've attached.

- A concluding statement reasserting that the charge was valid.

By being selective and methodical, you can turn representment from a reactive headache into a proactive tool for revenue recovery.

Tracking the Metrics That Actually Matter

You can't fix what you don't measure. If you’re serious about getting chargebacks under control, you have to shift from just reacting to disputes to proactively managing them with a data-driven mindset. Instead of guessing what’s working, you need to track a few key performance indicators (KPIs) that tell the true story.

Think of these metrics as your command center dashboard. They give you the intel needed to spot dangerous trends, measure the ROI of your prevention tools, and make smarter decisions. This is how you transform chargeback management from a frustrating chore into a strategic function that actually protects your revenue. Flying blind without this data means you'll never know if your efforts are paying off.

Your Core Chargeback KPIs

To get a complete picture, you really need to keep an eye on three specific metrics. Each one tells a different part of the story, from how many disputes you're getting in the first place to how effectively you're deflecting and fighting them.

Let's break them down.

Chargeback Rate

This is the big one. It’s the primary metric that payment processors and the card networks (think Visa and Mastercard) use to judge the health of your merchant account. Simply put, it measures what percentage of your total transactions turn into a chargeback.

- How to Calculate It: (Total Chargebacks in a Month / Total Transactions in a Month) x 100

- What It Tells You: This is your main risk indicator. If your rate creeps above 0.9%, you risk landing in a monitoring program like the Visa Acquirer Monitoring Program (VAMP), which can come with hefty fines or even the threat of account termination.

Representment Win Rate

This KPI gets straight to the point: how good are you at fighting the chargebacks you decide to contest? It’s a direct reflection of your evidence quality and the strength of your representment cases.

- How to Calculate It: (Number of Chargebacks Won / Number of Chargebacks Fought) x 100

- What It Tells You: A healthy win rate, somewhere over 40-50%, shows you’re picking the right battles and presenting compelling evidence. If your rate is low, you might be wasting resources fighting unwinnable cases or need to seriously improve your documentation.

Alert Deflection Rate

If you're using chargeback alert services like RDR or CDRN, this is arguably your most important metric. It shows how many would-be chargebacks you’re successfully intercepting and resolving with a refund before they officially get filed.

- How to Calculate It: (Number of Alerts Refunded / Total Number of Alerts Received) x 100

- What It Tells You: This metric directly measures the ROI of your alert system. A high deflection rate—ideally 90% or more—is proof that you’re taking full advantage of that golden window to stop disputes from hurting your chargeback ratio.

Building Your Chargeback Dashboard

Tracking these numbers is just the start. The real power comes from plugging them into a simple dashboard—even a basic spreadsheet works—and watching for trends over time. This is where raw data turns into actionable insight.

Your dashboard isn't just a report card; it's a diagnostic tool. A sudden spike in your chargeback rate isn't just a problem—it's a symptom of an issue you can now pinpoint and solve.

Imagine you notice your chargeback rate jumped from 0.6% to 1.1% last month. By digging into the data, you might discover that a whopping 70% of those new disputes are tied to a single product you just launched. The reason code is always "Product Not as Described." Suddenly, you realize this isn't just a chargeback problem; it's a marketing problem. Your product page might be overpromising, and now you have the hard data to prove it and get it fixed.

To get started, here’s a simple framework for a dashboard that covers the essentials.

Chargeback Management KPI Dashboard

This table summarizes the most critical metrics to track. Monitoring these numbers will give you a clear, ongoing view of your chargeback management performance and overall business health.

| Metric (KPI) | How to Calculate It | What It Tells You |

|---|---|---|

| Chargeback Rate | (Total Disputes / Total Transactions) x 100 | Your overall account health and risk level. |

| Representment Win Rate | (Disputes Won / Disputes Fought) x 100 | The effectiveness of your evidence-gathering process. |

| Alert Deflection Rate | (Alerts Refunded / Alerts Received) x 100 | The ROI of your real-time prevention tools. |

By consistently reviewing this dashboard, you'll move from reacting to problems to anticipating them, allowing for strategic adjustments that save both time and money.

Using Data to Refine Your Strategy

With this data in hand, you can start making surgical adjustments. For instance, if you see that a particular shipping carrier is consistently linked to "Item Not Received" disputes, it might be time to find a more reliable partner. Or, if your representment win rate for transactions under $30 is practically zero, you can set up a rule to automatically refund those via an alert instead of wasting time fighting a losing battle.

This data-driven approach is the ultimate answer to stopping chargebacks. It takes you beyond treating individual disputes and empowers you to fix the root causes, turning your chargeback process into a source of business intelligence that strengthens your entire operation.

Common Chargeback Questions Answered

As you start getting deeper into managing disputes, you're bound to run into some specific questions. Getting the details right on how different systems and tactics work is what separates a good chargeback strategy from a great one. Let's tackle some of the most common challenges I see merchants face.

Can I Stop All Chargebacks Permanently?

Many merchants ask if it's possible to get their chargeback rate down to 0%. Realistically, that's not going to happen. Between sophisticated fraudsters and the occasional genuine customer issue, a few are always going to slip through.

The real goal isn't a perfect record; it's sustainable control. Your best defense always starts with the basics: clear billing descriptors and easy-to-find customer support. You'd be surprised how many disputes those two things can prevent right out of the gate.

But the most powerful tool in your arsenal is a real-time alert service. These systems catch a dispute the moment a customer calls their bank, giving you a critical 24-72 hour window to resolve it directly. By automatically refunding a low-value or high-risk transaction in that window, you stop it from ever becoming an official chargeback and dinging your merchant account health.

Think of it this way: You can't prevent every customer complaint, but you can control whether that complaint escalates into a costly, damaging chargeback. Alert systems give you that control.

What Is the Difference Between RDR, CDRN, and Ethoca?

These are the three big names in chargeback alerts, but they aren't interchangeable. They're tied to different card brands and work in slightly different ways.

Here’s a quick breakdown:

- RDR (Rapid Dispute Resolution) is Visa's system. It’s fantastic because it lets you set rules to automatically accept liability and refund a transaction. The dispute is stopped instantly, before it ever escalates.

- CDRN (Consumer Dispute Resolution Network) comes from Verifi (which is owned by Visa) and works with a network of major card issuers.

- Ethoca is owned by Mastercard and collaborates with thousands of card-issuing banks around the globe to provide its alerts.

A top-tier chargeback management platform will integrate with all three. This is non-negotiable if you want maximum coverage. It ensures that no alert slips through the cracks, no matter what kind of credit card your customer used.

Is It Always Worth Fighting a Chargeback?

Absolutely not. One of the biggest mistakes I see merchants make is trying to fight every single dispute. It’s a huge waste of time and money.

Think about it—for a low-value transaction, the staff time and operational cost of gathering evidence and writing a rebuttal will often cost more than the money you'd get back. This is where those automated refunds via alert systems become a financial lifesaver.

On the other hand, for high-value orders where you have rock-solid evidence—like a delivery confirmation with a signature to a verified address and matching AVS/CVV data—fighting is absolutely the right move. This approach lets you recover significant revenue and sends a clear message to would-be friendly fraudsters.

For more tips on building a smarter dispute strategy, check out the resources on the Disputely blog. The key is to use your own data to see which types of disputes you consistently win and focus your energy there for the best return on your effort.

Stop losing revenue to preventable disputes. Disputely integrates with RDR, CDRN, and Ethoca to deflect up to 99% of chargebacks before they happen. Protect your business today.