What Is a Merchant of Record and Why Does It Matter?

When a customer buys something from you online, who is legally on the hook for that transaction? The answer points to the merchant of record, or MoR.

Simply put, the merchant of record is the legal entity responsible for selling goods or services to a customer. It's the name that shows up on their credit card statement, and it's the party legally accountable for every single piece of that transaction, from payment processing to tax remittance.

The Hidden Engine of Your Ecommerce Sales

That simple "click to buy" button triggers a surprisingly complex chain of events. It’s not just a payment gateway zapping money from one account to another; it's a legal event that comes with a whole lot of responsibility. The entity that shoulders this entire load is the merchant of record.

Think of an MoR like the general contractor on a home build. The contractor doesn’t just hammer a few nails; they are legally responsible for the whole shebang—permits, plumbing, electrical, inspections, everything. In the same way, an MoR is accountable for every single facet of a customer's purchase, making sure it's all handled correctly and by the book.

Who Holds the Ultimate Responsibility

This isn't just some legal fine print. It's the core of your company's financial and legal liability. The merchant of record is the party officially recognized as the seller, making them accountable for a host of critical, often headache-inducing, tasks.

For any business, but especially for high-volume SaaS or direct-to-consumer (DTC) brands, getting a handle on this role is absolutely critical. The MoR is tasked with:

- Processing payments securely and staying compliant with tough standards like PCI DSS.

- Calculating, collecting, and sending off sales taxes and VAT in every single place you do business.

- Managing customer disputes, refunds, and messy chargebacks, while also eating the associated costs and risks.

- Assuming full liability for fraud and ensuring every transaction meets global and local regulations.

In essence, the merchant of record sells directly to the consumer and becomes the legally liable party for that sale. This is what makes it so much more than a simple payment processor, which just moves money around.

So, if you run your store on a platform like Shopify and use Stripe for payments, guess what? Your business is the merchant of record. You're not just moving products; you are the legally designated seller, on the hook for all the financial details.

Why This Matters for Your Business

For any online business looking to scale, the question of who serves as the merchant of record has huge consequences. When you act as your own MoR, you get complete control over your branding and the customer checkout experience. But the trade-off is massive: you take on the immense administrative and financial burden of global compliance and dispute management yourself.

Drop the ball on these duties, and the fallout can be brutal. We’re talking hefty fines for tax mistakes or even losing your ability to process credit cards entirely because of high chargeback rates. That name on your customer’s bank statement is a big deal—it’s a signal of who, ultimately, is carrying all the risk.

What a Merchant of Record Actually Does

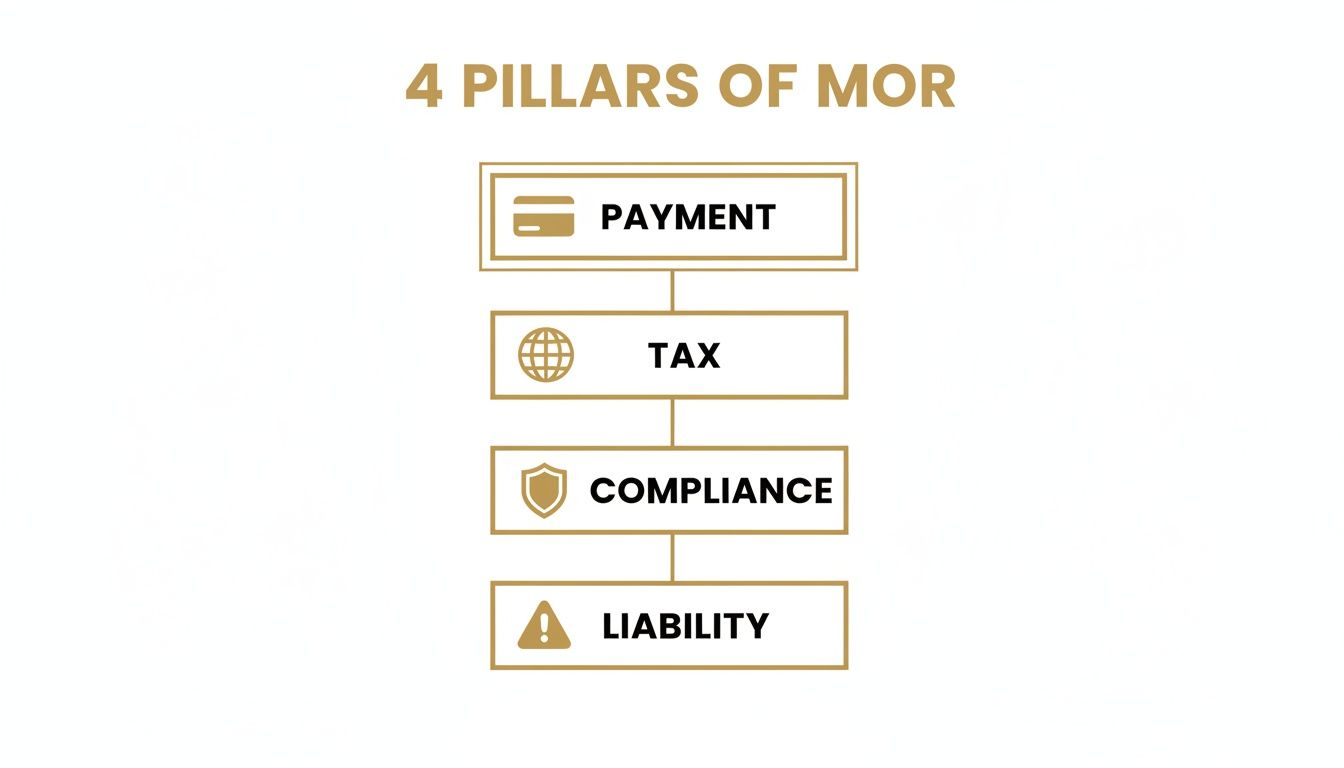

Stepping into the role of a merchant of record is a massive commitment. It’s not just about getting paid; it’s about taking on the full legal and financial weight for every single customer transaction, from the moment they click "buy" to long after the sale is complete.

This responsibility breaks down into four key areas. Think of them as pillars holding up the entire operation. If any one of them wobbles, the whole structure is at risk—we're talking hefty fines, legal headaches, and even getting blacklisted by payment processors.

1. Handling Payments and Keeping Them Secure

At its heart, the merchant of record owns the entire payment process. This means setting up a secure checkout, managing the relationships with payment gateways and banks, and, most importantly, making sure customer card data is locked down tight.

This isn't a "set it and forget it" task. It demands strict, ongoing compliance with the Payment Card Industry Data Security Standard (PCI DSS)—a notoriously complex set of rules designed to keep financial data safe. For any business that decides to be its own MoR, this is a heavy lift, requiring constant security audits, staff training, and rigorous data management.

2. The Nightmare of Global Sales Tax and VAT

Here's where things get really complicated. One of the biggest jobs for a merchant of record is figuring out global sales tax and Value-Added Tax (VAT). The critical thing to understand is that tax isn't based on where your business is; it's based on where your customer is. That means the MoR is on the hook for calculating, collecting, and paying the right tax in every city, state, and country they sell into.

And this isn't a static problem. Tax laws are constantly in flux, which turns compliance into a full-time job.

- Imagine a US-based e-commerce store: It has to track sales tax nexus across potentially dozens of states, all with their own quirky rules and rates for everything from t-shirts to digital downloads.

- Or think about a European software company: It must navigate the maze of EU VAT, applying different rates based on each customer's home country and filing complex cross-border returns.

The MoR is the one legally responsible for getting this right. One wrong calculation or a missed filing can trigger audits and painful penalties.

"The moment you sell across a border, you inherit that jurisdiction's tax and consumer protection laws. As the Merchant of Record, you are the one accountable for getting it right, every single time. There is no middle ground."

3. Staying on the Right Side of the Law

Beyond just taxes and payment security, the merchant of record has to play by a whole rulebook of local and international laws. We're talking about consumer protection regulations and data privacy acts like Europe's GDPR or California's CCPA, which have a huge say in how you collect, store, and use customer information.

The MoR's entire operation, from the wording on a checkout page to the fine print in the refund policy, has to align with the specific laws of every region they serve. It's a constant balancing act of monitoring legal changes and adapting business practices on the fly.

4. Taking the Hit on Chargebacks and Refunds

This might be the most direct and painful financial risk of being a merchant of record: you are 100% liable for every single chargeback and refund. When a customer disputes a charge with their bank, it's the MoR's name on the merchant account, and they are the one who has to deal with it.

This liability isn't just about losing the sale. The MoR is responsible for:

- The full disputed amount of the transaction.

- Punitive chargeback fees from the processor, which can run anywhere from $15 to $100 per dispute, win or lose.

- Potential fines from card networks like Visa and Mastercard if their chargeback rate gets too high.

The MoR absorbs every dollar of risk for every transaction, including those that turn out to be friendly fraud or outright criminal activity. This absolute liability is what truly defines the MoR model and sets it apart from other ways of processing payments.

Comparing MoR to Payment Processors and Marketplaces

In the world of online selling, a few key players help get money from your customer's wallet into your bank account. They might all look like they do the same thing, but their legal roles are worlds apart. Getting this wrong can leave you facing some serious legal and financial headaches you never saw coming.

The most common mix-up? Confusing your role as the merchant of record with simply using a payment processor. They are absolutely not the same thing.

Payment Processors Merely Move Money

Think of a payment processor like Stripe, PayPal, or Square as a high-tech armored truck for your money. Their one job is to securely grab a payment from a customer's bank, make sure the funds are there, and deliver it safely to your merchant account. They provide the rails the transaction runs on.

But that’s where their job ends. They're just the messenger.

When you use a payment processor on your own website—say, a store built on Shopify or WooCommerce—your business is the merchant of record. This means all the messy, complicated, and risky parts of the sale are still on your shoulders. The processor won't calculate your sales tax, file VAT returns in Europe, or eat the cost when a customer files a chargeback. All that liability is yours and yours alone.

If you're just getting started, understanding the setup is key. You can get a good overview of the initial steps by looking into a Stripe account signup.

Marketplaces Often Act as the MoR

Now, let's look at big online marketplaces like Amazon, Etsy, or the Apple App Store. These platforms play by a completely different set of rules. For most sales on their sites, the marketplace itself steps in and becomes the merchant of record.

Ever notice how when you buy something from a third-party seller on Amazon, your credit card statement still says "Amazon"? That’s the MoR model in action.

This is a huge deal. By acting as the MoR, the marketplace shoulders the massive burden of liability for you.

- Tax Compliance: Amazon figures out and pays the correct sales tax for the purchase.

- Payment Security: The marketplace is responsible for maintaining its PCI DSS compliance.

- Chargebacks: Disputes are filed against the marketplace's account, protecting you directly.

This is where the four pillars of the MoR role really come into focus. It’s a huge job, whether it's you or a marketplace handling it.

The MoR role is a massive undertaking, combining payment logistics, global tax laws, constantly changing regulations, and complete financial liability.

Of course, this service isn't free. Marketplaces charge for this peace of mind through higher fees or commissions. You're essentially trading a cut of your revenue for a massive reduction in administrative work and financial risk.

A Clear Breakdown of Responsibilities

To make this perfectly clear, let's put these three models head-to-head. This table breaks down who handles what, so you can see exactly where the responsibility falls in each scenario.

Merchant of Record vs Payment Processor vs Marketplace

| Responsibility | Merchant of Record (You) | Payment Processor (e.g., Stripe, PayPal) | Marketplace Facilitator (e.g., Amazon) |

|---|---|---|---|

| Payment Collection | ✅ Handled via your merchant account | ✅ Facilitates the transfer of funds | ✅ Handles the entire process |

| Sales Tax & VAT | 100% Your Responsibility | ❌ Not their liability | ✅ Handled by the marketplace |

| PCI DSS Compliance | 100% Your Responsibility | ✅ Provides compliant tools, but you're liable | ✅ Handled by the marketplace |

| Chargeback Liability | 100% Your Responsibility | ❌ Passes liability back to you | ✅ Handled by the marketplace |

| Refund Management | 100% Your Responsibility | ❌ Processes refunds you initiate | ✅ Often handled through their system |

| Customer's Statement | Your Company Name | Your Company Name | Marketplace Name |

This comparison shows the stark differences in liability and workload.

Here's the bottom line: A payment processor works for you, but a marketplace (acting as the MoR) sells things on behalf of you. One model leaves you exposed to all the risk; the other shields you from it.

For anyone running their own online store, this isn't just trivia—it's fundamental. Even though tools like Shopify Payments (which is powered by Stripe) make accepting money feel automatic, they don't change your legal status. You are still the merchant of record, and you’re on the hook for every tax law, every banking regulation, and every painful chargeback.

Why the MoR Is Ground Zero for Chargebacks

When a customer disputes a transaction, that chargeback doesn't just float in a void. It has to land somewhere. And it lands squarely on the shoulders of the merchant of record. Why? Because the MoR is the legally recognized seller whose name is on the merchant account tied to that sale.

Think of it this way: when a customer files a dispute, their bank isn’t looking for your payment processor or your e-commerce platform. They're looking for the business that legally sold them the product. As the MoR, that’s you. You are the final destination for every dispute, every fee, and every penalty that comes with it.

This direct liability turns your business into the financial battleground for customer disputes. The scale of this problem is immense. In 2023 alone, the global payment ecosystem saw a staggering 238 million chargebacks filed—a massive wave that directly hits merchants acting as the MoR. For businesses like high-volume eCommerce shops on Shopify or DTC brands using Stripe, this means fighting not just for lost revenue but against fees, reputational damage, and potential account freezes. You can dive deeper into the latest chargeback statistics to see the full picture.

The Rise of Friendly Fraud

One of the most frustrating parts of this liability is the explosion of friendly fraud. This isn't about stolen credit cards. It’s when a legitimate customer makes a purchase and then disputes the charge with their bank, often out of convenience or a simple case of buyer's remorse.

They might not recognize the charge, have forgotten about a recurring subscription, or simply want their money back without the hassle of your official return process. To the bank, though, it all looks like fraud, and the MoR is left holding the bag.

This issue is especially painful for:

- Subscription Businesses: Customers frequently forget about recurring payments and file a chargeback instead of just canceling their plan.

- DTC Brands: High transaction volumes and direct-to-consumer relationships create more opportunities for misunderstandings or post-purchase regret.

The odds are stacked against you. When you fight a chargeback, you have to provide compelling evidence to prove the transaction was legitimate—a process that is both time-consuming and, far too often, unsuccessful.

The Real Cost of High Chargeback Ratios

The financial sting of a chargeback goes far beyond the lost sale. For every single dispute, the merchant of record gets hit with multiple layers of costs that can quickly spiral out of control.

A chargeback isn't a simple refund. It's a forced reversal of funds that comes loaded with non-refundable penalty fees, administrative costs, and long-term damage to your payment processing relationships.

Each dispute you receive as the MoR costs you:

- The Original Transaction Amount: The revenue from the sale is immediately clawed back.

- A Non-Refundable Chargeback Fee: Payment processors charge a penalty of $15 to $100 per dispute, and you pay it whether you win or lose.

- Operational and Labor Costs: The time your team spends digging up evidence and fighting the dispute is a significant, and often overlooked, expense.

The Ultimate Penalty: Losing Your Merchant Account

The most severe consequence of unchecked chargebacks is the risk it poses to your ability to process payments at all. Card networks like Visa and Mastercard monitor your chargeback-to-transaction ratio very, very closely.

If your ratio creeps past their thresholds (typically around 0.9%), you can be placed into a monitoring program. This is a serious red flag for processors.

Being in one of these programs can lead to:

- Processor-Imposed Reserves: Your payment processor may start holding back a percentage of your revenue as a security deposit against future chargebacks.

- Higher Processing Fees: You'll be labeled a "high-risk" merchant, leading to much more expensive transaction rates.

- Account Termination: In the worst-case scenario, your merchant account can be shut down completely, leaving you unable to accept credit card payments.

For any business acting as its own merchant of record, this is the ultimate threat. It’s why managing chargeback liability isn't just about protecting revenue—it's about ensuring the very survival of your business.

How to Proactively Manage Chargeback Risk

If you're only dealing with chargebacks after they hit your merchant account, you're already behind. By that point, the fees are locked in, your chargeback ratio has taken a hit, and you're stuck playing defense. For any business serving as its own merchant of record, the only way to win is to stop disputes before they ever become official chargebacks.

This means shifting from a reactive stance to a proactive one. Instead of waiting for the damage report, you get ahead of the problem by catching customer disputes right as they start. This is exactly where chargeback prevention alerts come into play.

Intercepting Disputes at the Source

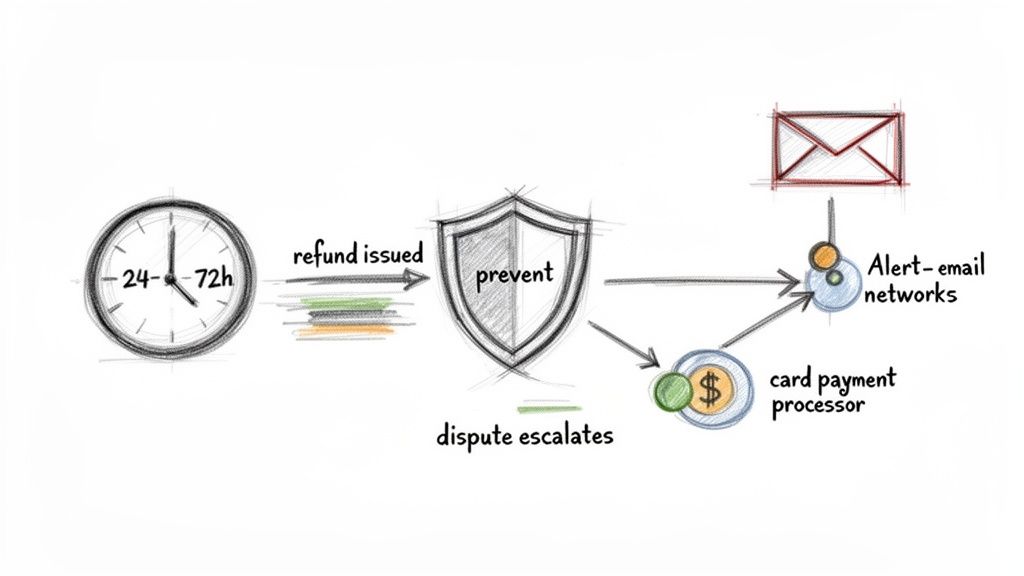

Think about what happens when a customer sees a charge they don't recognize. Their first move is usually to call their bank. In the old model, that phone call instantly kicks off a formal chargeback process. But what if you could get a heads-up the moment that customer made the call?

That’s precisely what chargeback alert networks do. The major card brands have systems designed to flag these initial inquiries:

- Visa's Rapid Dispute Resolution (RDR): A system built to automatically resolve disputes before they escalate.

- Mastercard's CDRN (Consumer Dispute Resolution Network): A collaborative network that provides merchants with early warnings of customer disputes.

When a cardholder at a participating bank initiates an inquiry, these networks send out an immediate alert. This gives the merchant of record a critical window—usually just 24 to 72 hours—to resolve the issue directly.

By getting an alert before the dispute is formalized, you have a golden opportunity. You can issue a direct refund to the customer, which satisfies their bank and stops the chargeback from ever being filed.

This simple, proactive refund keeps the dispute from damaging your chargeback ratio and saves you from paying steep penalty fees. It’s the single most effective tactic for protecting your merchant account's health.

Automating Your First Line of Defense

Trying to watch for these alerts manually is simply not feasible, especially for businesses processing a high volume of transactions. This is where a modern chargeback alert platform becomes an indispensable tool for any merchant of record.

These services connect directly with the RDR and CDRN networks, acting as your 24/7 watchdog. When an alert comes in, the platform can automatically trigger a refund based on rules you’ve set, all without needing you to lift a finger.

For example, a platform like Disputely plugs right into your payment processor, whether it's Stripe, Shopify Payments, or another provider. You can set rules to automatically refund any dispute under a certain dollar amount or for a particular product. The whole thing happens in real-time, effectively deflecting the chargeback before it can cause any harm.

This kind of automation gives a merchant of record the power to systematically neutralize one of their biggest operational risks. To see how this fits into a bigger picture, you can explore how to get started with a chargeback representment strategy.

The Financial Impact of Prevention

Let's be clear: a proactive strategy isn't just a nice-to-have; it's essential. The threat of disputes is only growing. Acting as your own merchant of record exposes you to skyrocketing chargeback volumes, which are forecasted to jump from 261 million in 2025 to 324 million by 2028. That’s a 24% increase, set to cost businesses $41.7 billion worldwide.

Early intervention through integrated alerts can lead to up to 99% reductions in chargebacks. You can filter out the winnable disputes and automate refunds within that crucial 24-72 hour window. This approach protects your relationship with your payment processor without forcing you into hefty reserves or restrictive contracts. For a deeper dive into these numbers, you can read the full research about chargeback statistics.

Ultimately, managing chargeback risk as an MoR isn't about winning every fight. It’s about choosing which battles are worth fighting. By using automated alert systems, you can strategically refund the unwinnable or low-value disputes, saving your time and resources to fight clear-cut cases of fraud. This balanced approach is the key to long-term stability and growth.

Choosing Your Path: When to Be Your Own Merchant of Record

For most businesses striking out on their own, becoming the merchant of record isn't a deliberate choice—it's just what happens when you set up shop online. The real question isn't if you'll be the MoR, but how you're going to juggle all the responsibilities that come with the title.

Taking on this role puts you firmly in the driver's seat. You get total control over your branding, how you interact with customers, and your pricing. But with great power comes great liability. You're the one on the hook for figuring out complex global tax laws, staying PCI compliant, and taking the financial hit from every single chargeback and fraudulent purchase. It all comes down to balancing that control against what your company can realistically handle today and where you want to go tomorrow.

Are You Ready for the Responsibility?

Before you push for serious growth, you need to take a hard, honest look at your capabilities. This isn't about shying away from being the MoR; it's about being smart and preparing to do it well. A big part of this evaluation involves understanding the strategic implications of choosing platforms such as Shopify vs. Amazon, since each one handles liability in a fundamentally different way.

Ask yourself these questions:

- Transaction Volume: Do we have the infrastructure to handle a massive number of transactions, each with its own paper trail and compliance rules?

- International Sales: Are we truly ready to manage the complexities of VAT, GST, and all the other taxes that come with selling across borders?

- Risk Tolerance: What would a sudden jump in chargebacks do to our cash flow? Could we weather the storm?

- Internal Resources: Does anyone on our team actually have the expertise to manage payment disputes, fraud prevention, and global compliance?

Just look at the travel and hospitality industry for a stark example. They face the highest average chargeback value, a whopping $120 per dispute, compared to retail's $84. For travel companies with high sales volume, 52% of unhappy customers don't even bother contacting them for a refund—they go straight to their bank. And a staggering 75% of those cases are fueled by friendly fraud.

At the end of the day, being your own merchant of record is completely manageable, and even a competitive advantage, if you have the right tools in your corner. Proactive tools, like a chargeback alert platform that stops disputes before they officially start, aren't just a "nice-to-have" anymore. They are essential for any business that's serious about scaling.

You can see how this works by checking out Disputely's transparent alert pricing to understand how it can protect your bottom line.

Common Questions About the Merchant of Record Model

When you start digging into payment processing and liability, a few questions always pop up. Let's tackle some of the most common ones to give you a clearer picture of the merchant of record role.

If I Use Stripe or Shopify Payments, Am I the MoR?

Yes, almost always. If you're running your own store and using a payment gateway like Stripe, Shopify Payments, or PayPal, your business is the merchant of record.

Think of these platforms as payment service providers (PSPs). They're experts at securely handling the transaction and moving money from your customer's bank to yours. But they aren't taking on the legal or financial liability for the sale itself. That means you're still on the hook for sales tax, PCI compliance, and any chargebacks that come your way.

What's the Difference Between a Merchant of Record and a Seller of Record?

Honestly, not much. For most practical purposes, the terms "Merchant of Record" (MoR) and "Seller of Record" (SoR) are used interchangeably.

Both titles refer to the one entity that's legally responsible for the entire customer transaction. "Merchant of Record" is just the more popular term you'll hear in payment and e-commerce circles, while "Seller of Record" might pop up in broader legal or tax discussions. The core duties are exactly the same.

The bottom line is this: whether you call it MoR or SoR, it’s the name on the dotted line. It’s the party that owns the financial and legal liability for every single sale, from processing the payment to handling the inevitable dispute.

Can a Chargeback Platform Get Rid of All My MoR Risk?

No, and it's important to understand why. A chargeback platform can't eliminate all the risks that come with being the merchant of record, but it provides a massive defense for one of the most painful parts.

A service like Disputely is a specialist tool. Its job is to tackle the high-stakes, revenue-draining problem of chargebacks head-on. By alerting you to disputes before they escalate, it drastically cuts down on the financial damage and operational headaches.

However, it doesn't take over your other fundamental MoR duties, like:

- Calculating and paying sales tax and VAT

- Maintaining strict PCI DSS compliance

- Following local consumer protection laws

Think of it this way: a chargeback alerts platform is like having an elite security detail for your revenue. It protects you from the most aggressive and immediate threats, freeing you up to manage the other essential responsibilities of being the MoR.

Stop letting preventable disputes drain your revenue. Disputely connects directly with card networks to warn you about chargebacks before they even happen. This gives you a crucial window to issue a refund and protect your merchant account health. See how much you could be saving and get started in under five minutes at Disputely.com.