No refund policy: Protect Your Business with Clear, Fair Terms

A no refund policy is exactly what it sounds like: a company’s official stance that once a sale is made, it's final. No take-backs, no monetary reimbursements. It’s the business equivalent of saying, “All sales are final,” a move designed to lock in revenue and keep operations straightforward.

What a No Refund Policy Really Means for Your Business

On the surface, a no refund policy seems like a simple tool for managing your bottom line and setting clear boundaries with customers. You can think of it like the final clearance rack in a department store—once an item is in your bag, it's yours for good. This approach is especially common for businesses selling things that can't easily be "returned," like digital downloads, custom-made furniture, or consulting services.

But here’s the thing: in the world of online business, this policy isn't the ironclad shield many merchants think it is. It has to exist within a much larger framework of consumer protection laws and the rules set by credit card networks. So, while it can definitely help ward off some return requests, it doesn't give you a free pass to reject every single refund claim that comes your way.

The Intersection of Policy and Reality

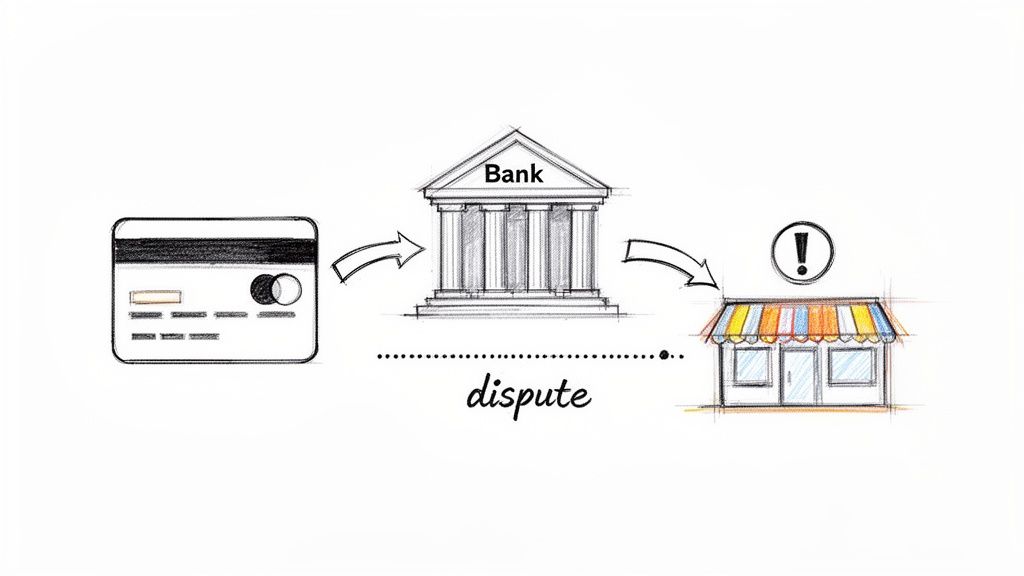

The words "no refunds" don't really end the conversation for a determined customer. It just changes where the conversation happens. When you shut the door on a direct refund, a frustrated customer's next move is often a call to their bank to file a chargeback. And just like that, what was a simple internal policy has mushroomed into a costly, formal dispute that you’re not guaranteed to win.

A rigid no refund policy can accidentally become your number one source of chargebacks. When customers feel like they've hit a brick wall with you, they'll just go around you and straight to their card issuer.

This is the real-world challenge for any online business. Your policy might stop someone with a simple case of "buyer's remorse," but it can also backfire spectacularly when a customer has a legitimate problem. Think about someone who received a broken item or a service that was never rendered. They aren't just going to walk away.

Understanding the Financial Stakes

The pressure to get returns under control is very real, especially as the volume keeps climbing. In 2025, global retail refund volumes shot up by a massive 18.1% year-over-year, with the total dollar value of those refunds increasing by 12.7%. This kind of growth puts an incredible strain on ecommerce merchants of all sizes. And with the holiday season accounting for roughly 20% of all yearly refunds, a weak policy can sink your profits. You can dig deeper into these numbers in ACI Worldwide's ecommerce report.

In the end, having a no refund policy is a delicate balancing act. It can shield your business from fraudulent returns, but it can also alienate honest customers and send your chargeback rate through the roof. The trick is to realize that your policy is just the opening line—it’s not the final word. We’ll get into the legal fine print, the pros and cons, and smarter strategies to make this policy work for you, not against you.

Navigating the Legal Landscape of Returns

It’s a common belief among business owners: post a “no refund policy,” and that’s the end of the story. But in reality, that sign on your website isn't an impenetrable legal shield. Consumer protection laws across the globe often have the final say, and they can easily override your store’s policy.

Think of it this way: your policy is your set of house rules, but consumer law is the city ordinance. If your rules clash with the law, the law wins—every single time. This is especially critical for e-commerce brands and subscription services selling to a global audience, as you’re instantly subject to the regulations wherever your customers live.

Statutory Rights and What You Owe Your Customers

In most developed countries, customers have what are called statutory rights. These are baseline protections baked into the law that can't be signed away, no matter what your terms and conditions say. These rights generally ensure that products are of satisfactory quality, fit for the purpose they were sold for, and match the description you provided.

If you sell something that's defective or wildly different from what you advertised, your no refund policy is legally out the window for that sale. You’re legally on the hook to provide a solution, whether that’s a repair, a replacement, or a full refund.

A no refund policy is meant for discretionary returns—like when a customer just changes their mind. It offers no legal protection against non-discretionary issues, such as selling faulty goods or not delivering a service as promised.

This is a crucial distinction. A customer with a simple case of buyer's remorse? You can probably hold them to your policy. But a customer who receives a broken item? They’re protected by law, and ignoring that can lead to forced refunds, legal trouble, and a tarnished reputation.

Regional Laws You Absolutely Cannot Ignore

The rules for returns and refunds change dramatically from one place to another. What’s perfectly fine in one country could get you into hot water in the next. To get a feel for how these terms are formally structured, it's often helpful to review a well-drafted Terms of Service.

Here’s a quick look at how different major markets handle it:

United States: There’s no federal law that forces businesses to offer refunds, which gives sellers a lot of leeway. But state laws can and do apply, and the Uniform Commercial Code (UCC) implies warranties that goods must be "merchantable," meaning they work as expected.

United Kingdom: The Consumer Rights Act 2015 is a big one. It gives customers a firm 30-day right to reject faulty goods and get a full refund. This right is non-negotiable and trumps any store's no refund policy.

European Union: The EU’s Consumer Rights Directive gives online shoppers a 14-day "cooling-off" period. During this window, a customer can return an item for any reason at all—or for no reason—and you are required to give them a full refund.

Ignoring these regulations isn't just a customer service misstep; it can lead to hefty fines and legal battles. Your policy needs to be firm where it can be but flexible enough to meet these legal requirements. At the end of the day, consumer law sets the baseline, and your refund policy has to be built on top of that foundation.

Weighing the Pros and Cons for Your Business

Deciding to implement a no refund policy is a huge call for any ecommerce business. Think of it as a double-edged sword: it can guard your revenue stream, but it can just as easily drive away your customers. Before you go all-in on a policy that will define your relationship with buyers, you need to understand both sides of the coin.

On one hand, the upsides are pretty tempting. A strict policy is a great defense against return fraud and "wardrobing"—that classic move where someone buys an outfit, wears it once, and sends it back. This kind of abuse costs retailers a fortune every year. A no-refund rule also makes your financial planning a lot easier and cuts down on the hours your team spends processing returns and restocking inventory.

But the downsides can be just as serious. A rigid stance on refunds can spook potential customers right out of your checkout, leading to a drop in sales. It’s also a fast track to getting slammed with negative reviews, which can do lasting damage to your brand’s reputation and the trust you’ve worked so hard to build.

The Upside: Financial Stability and Fraud Reduction

Let's start with the good stuff. The most obvious win from a no refund policy is how it protects you from common return scams. For anyone selling digital goods, it stops people from downloading your product and then immediately demanding their money back.

This firmness translates directly into a more stable business. When you lock in sales and minimize returns, your cash flow becomes much more predictable. This is a game-changer for small businesses, companies with tight margins, or anyone selling custom-made or perishable items where a return is a complete loss. The operational perks are clear, too: less time spent on reverse logistics and fewer resources tied up in handling refund requests.

The Downside: Alienating Customers and Sparking Chargebacks

Now for the other side of the story. You really can't overstate the potential damage a no refund policy can do to your customer relationships. In a crowded online marketplace, a generous return policy is often seen as a sign that a business stands behind its products. Take away that safety net, and shoppers—especially new ones—are going to hesitate. In fact, studies show that a huge chunk of online buyers check the return policy before even adding an item to their cart, and a strict one is often an instant deal-breaker.

The biggest, most immediate danger of a strict no refund policy? A massive spike in chargebacks. When a customer feels like they've hit a wall and have no other option, they won't think twice about calling their bank. And just like that, a customer service issue escalates into a costly, damaging payment dispute.

This is the critical trade-off. In trying to shut down refund requests, you might accidentally open the floodgates to chargebacks. Card networks like Visa and Mastercard almost always side with the consumer in these disputes, especially if your policy wasn't crystal clear at checkout. Every single chargeback hits you with hefty fees and dings your dispute ratio, putting your entire merchant account at risk.

To really see this in action, let's break it down side-by-side.

Pros vs Cons of a No Refund Policy

This table lays out the core trade-offs you'll be making when deciding whether a no refund policy is the right fit for your business.

| Potential Benefits (Pros) | Potential Risks (Cons) |

|---|---|

| Reduces Return Fraud: Deters dishonest customers from abusing your return system. | Lower Conversion Rates: Scares off cautious buyers who want a risk-free purchase. |

| Predictable Revenue: Creates more stable and reliable cash flow forecasting. | Increased Chargebacks: Frustrated customers will dispute charges with their bank. |

| Lower Administrative Costs: Frees up resources from managing returns and refunds. | Negative Brand Reputation: Leads to poor reviews and damages customer trust. |

| Protects Perishable/Digital Goods: Prevents losses on items that cannot be resold. | Loss of Customer Loyalty: Discourages repeat business and positive word-of-mouth. |

Ultimately, whether a no refund policy makes sense depends entirely on your business model, the products you sell, and how much risk you're willing to take on. While it can be a shield against fraud and operational headaches, it also leaves you vulnerable to losing customers and getting buried in payment disputes.

When Your Policy Sparks a Chargeback

This is where the rubber really meets the road. A strict no refund policy might feel like the final word on a sale, but it often ends up being the starting pistol for a much bigger headache—the chargeback.

When a customer's request for a refund hits a brick wall, their next move usually isn't to just give up. Instead, they reach for the most powerful tool they have: their bank.

This pivot from a simple refund request to a formal payment dispute is where so many businesses get tripped up. Once a customer files a chargeback, your carefully crafted policy is no longer the deciding factor. The power shifts entirely from you to the card networks, like Visa and Mastercard, and their rulebook is written to protect the consumer.

The chargeback process essentially bypasses your authority. The customer’s bank initiates the dispute, yanks the funds right out of your account, and puts them on hold while they investigate. Your "no refund" statement suddenly becomes just one piece of evidence in a process that’s heavily weighted against you.

Why Your Policy Is Not an Iron Shield

Think of the chargeback system as a consumer court of appeals. Your no refund policy is your initial ruling, but the card networks are the judges, and they play by their own set of laws. They’re going to look at the entire situation from the cardholder's point of view.

For instance, was the policy displayed clearly before the purchase? Did the customer have to actively agree to it, maybe by checking a box at checkout? If your policy was buried in the fine print or tucked away on a hard-to-find page, the bank will likely dismiss it out of hand.

A no refund policy is only as strong as its visibility. If a customer can plausibly claim they never saw it, card networks will almost always side with them in a dispute, making your policy completely ineffective.

Even with a perfectly displayed policy, you’re not shielded from chargebacks filed for legitimate reasons. These include claims that a product wasn't as described, arrived defective, or never showed up at all. In these cases, the bank sees it as a failure to deliver on your end of the deal, which completely overrides any refund restrictions you have in place.

The Escalating Costs of Disputes

This is more than just a customer service annoyance; it's a direct threat to your bottom line. U.S. retailers dealt with an incredible $743 billion in merchandise returns in 2023, with return fraud making up a staggering $101 billion of that figure. It’s no wonder merchants are tightening their policies. But as these retail return statistics from the NRF show, that move can backfire by pushing otherwise legitimate return requests straight into the dispute process.

Every single chargeback comes with a price tag:

- Non-refundable fees: You get hit with a penalty fee for every dispute, usually between $20 to $100, and you pay it whether you win or lose.

- Lost revenue: The original sale amount is reversed, so you lose the income.

- Lost product: In many disputes, the customer keeps the item. You're out the product and the payment.

The most dangerous consequence, though, is the hit to your dispute ratio. This is the percentage of your transactions that turn into chargebacks. If that number climbs above a certain threshold (typically 0.9%), the card networks will flag your business and place it in a monitoring program. This can trigger higher processing fees, frozen funds, or even the termination of your merchant account—effectively shutting down your ability to accept credit cards.

If you find yourself in this situation, it's crucial to have a plan. You can learn more about how to navigate these challenges by exploring effective chargeback representment strategies.

How to Write a Policy That Actually Works

Let's be blunt: a poorly written no refund policy is often worse than having no policy at all. If your terms are buried on some forgotten page or loaded with confusing legal jargon, they won't do you any good when a customer files a dispute. A policy that actually protects your business boils down to two things: clarity and visibility.

Think of your policy less like a legal document and more like a simple, direct conversation with your customer. You need to use plain English and leave zero room for interpretation. Ambiguity is your worst enemy—it’s the loophole customers (and their banks) will use to win a chargeback.

The goal is to completely remove the possibility of a customer claiming, "I didn't know" or "I couldn't understand." Your policy has to be straightforward, concise, and impossible to miss.

Core Elements of an Enforceable Policy

To hold up under pressure, your no refund policy needs a few key ingredients. If you miss one, you're weakening your entire defense. Think of it as the foundation of your terms of sale.

Here’s a quick checklist of the must-haves:

- A Clear Statement of Final Sale: Start with a bold, unambiguous line right at the top. Something like "All sales are final" or "We do not offer refunds or returns" works perfectly.

- Specific Timeframes (If Applicable): If you make exceptions for things like exchanges or store credit, define the timeline. For example, "Exchanges must be requested within 14 days of delivery." Be specific.

- Defined Conditions for Exceptions: Clearly spell out the rare cases where you will step in, such as for items damaged in transit or if you sent the wrong product. It’s a good idea to require photo evidence to back up these claims.

- Instructions for Legitimate Issues: Give customers a clear, step-by-step process for reporting a valid problem. Provide a dedicated support email or a link to your help portal. Don't make them hunt for it.

- An Explicit List of Non-Returnable Items: Get granular. List exactly which products are not eligible for return. This is absolutely critical for digital downloads, personalized items, sale products, and anything perishable.

Visibility Is Your Best Defense

A brilliantly crafted policy is completely useless if nobody sees it. To make it enforceable—especially in the eyes of a payment processor—you have to prove the customer saw and agreed to it before they paid. This makes strategic placement a non-negotiable part of your strategy.

Your policy needs to show up in a few key places:

- Website Footer: A permanent link here ensures it's always accessible from any page on your site.

- Product Pages: For any item that is final sale, a clear notice right on the product description is a must.

- Checkout Page: This is the most important spot. You need a checkbox that forces the customer to actively agree, with text like, "I have read and agree to the no refund policy."

The checkout confirmation checkbox is your single most powerful piece of evidence in a chargeback dispute. It proves the customer actively acknowledged and accepted your terms before paying.

This multi-pronged approach builds a rock-solid defense, making it almost impossible for a customer to credibly claim they weren't aware of your terms. You can find more details about structuring these kinds of agreements in our general Disputely Terms.

Offering Alternatives to a Hard "No"

A strict, no-exceptions policy can sometimes feel aggressive and might even scare off potential buyers, leading to more abandoned carts. Smart merchants often soften the blow by offering alternatives. This protects your revenue while still giving the customer a good outcome, which can stop a frustrated buyer from heading straight for the chargeback button.

Consider these powerful alternatives:

- Store Credit: This is usually the best-case scenario. The money stays in your business, and the customer gets the freedom to pick something else they’ll be happy with.

- Exchanges: A perfect solution for physical goods. Offering a swap for a different size, color, or a similarly priced item can solve the problem instantly without you losing a sale.

- Partial Refunds: If an item has a minor flaw but is still perfectly usable, a partial refund can be a great compromise. It shows good faith, satisfies the customer, and prevents a full return.

The retail world is tough, with returns in the U.S. expected to hit an eye-watering $890 billion in 2024. This reality is pushing more merchants toward stricter policies, especially since 93% of retailers see fraud and policy abuse as major threats. By offering fair alternatives, you can protect your bottom line without alienating the 76% of shoppers who check the return policy before they even think about buying. To fully understand how to write a policy that actually works, it is essential to consider the broader framework of commercial contracts.

Enforcing Your Policy with Chargeback Alerts

Let's be real: a no refund policy is just words on a page until you have a smart way to enforce it. And true enforcement isn't about digging your heels in and fighting every single customer complaint. That’s a fast track to a suspended merchant account. The real goal is to stop disputes before they ever turn into damaging chargebacks.

This is where chargeback alert systems come into the picture. Think of them as an early-warning alarm for your business. They add a critical layer of defense, transforming your rigid policy into a dynamic, flexible shield that actually protects your bottom line.

How Chargeback Alerts Empower Your Policy

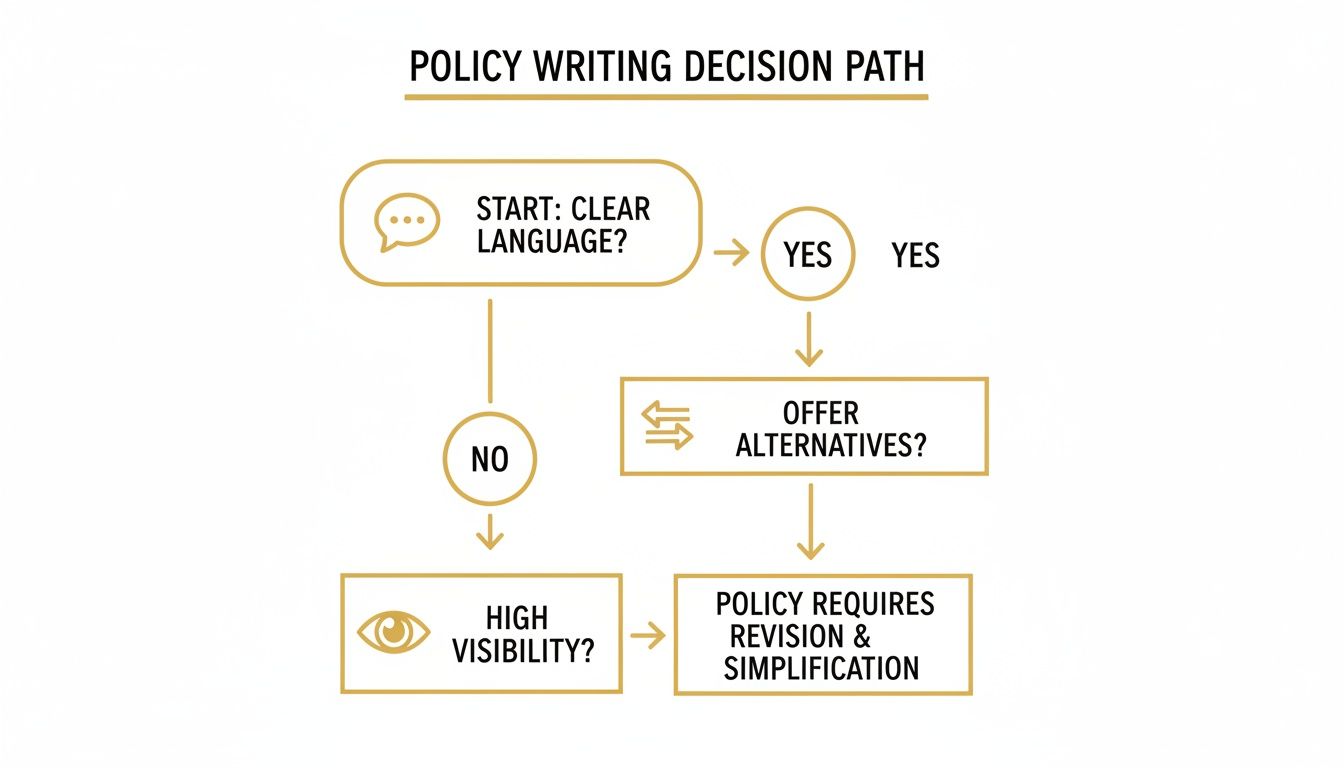

Chargeback alert networks, like Visa’s Rapid Dispute Resolution (RDR) and the systems from Ethoca and CDRN, give you a heads-up the second a customer calls their bank to complain. Instead of being blindsided weeks later when a formal chargeback hits, you get an alert almost instantly.

This notification gives you a crucial window—usually 24 to 72 hours—to do something before the bank officially files the dispute. It’s a game-changing opportunity to make a strategic call instead of being thrown into a reactive fight you're probably going to lose anyway. This is where you can decide how to best handle the situation, as the flowchart below illustrates.

As you can see, a successful strategy starts long before the dispute, with a clear policy and smart alternatives that prevent many complaints from happening in the first place.

With an alert in hand, you can automate your response based on rules you set. For instance, you could automatically refund any dispute under $25. It might sound strange for a "no refund" business to issue a refund, but it's a purely strategic move. You prevent a small-dollar issue from becoming a chargeback that costs you more in fees and hurts your all-important dispute ratio.

From Rigid Rule to Dynamic Defense

By plugging into an alert system, you get granular control over when and how you enforce your policy. You can filter the incoming alerts and decide which battles are actually worth fighting.

Is it a high-value order from a customer with a sketchy history? That's a dispute you might want to fight with strong evidence. Is it a small, ambiguous claim from a first-time buyer? A strategic refund is often the smarter financial decision.

This approach lets you stand firm on your no refund policy where it truly matters—against blatant fraud or clear abuse—while strategically giving in on others to keep your payment processor happy. For merchants on platforms like Shopify, this proactive stance is crucial for avoiding nightmares like a Shopify Payments account hold.

Ultimately, chargeback alerts are what make a no refund policy viable in the real world. They shift the power dynamic, so you're no longer at the mercy of the chargeback system. You're back in control, making sure your business stays profitable and protected.

Common Questions About No Refund Policies

When you're running a business, figuring out the details of a "no refund" policy can feel like walking a tightrope. Let's break down some of the most common questions merchants ask.

Can I Have a "100% No Exceptions" Policy?

You can write it, but you probably can't enforce it. A completely rigid no refund policy is a risky move and, frankly, often doesn't hold up in the real world. Many consumer protection laws legally require you to offer refunds for things like defective products or items that weren't as described, no matter what your policy says.

Beyond the legal headaches, a hardline "no exceptions" rule is practically an invitation for customers to file a chargeback. A much smarter play is a firm-but-fair policy. Spell out clear, legally sound exceptions for specific cases, like when an item arrives damaged.

Where Do I Need to Display My No Refund Policy?

Visibility is everything. If you want your policy to stick, you have to make sure customers see it before they buy. Hiding it in the fine print won't cut it.

Your best bet is to place it in several can't-miss spots:

- Put a clear link in your website's footer so it's on every page.

- Add a required checkbox at checkout, forcing customers to acknowledge they've read and agree to the terms.

- Include a quick note on product pages, especially for anything you're marking as final sale.

- Pop it into your order confirmation emails for good measure.

How Do Chargeback Alerts Help If I Don't Offer Refunds?

This is where you get to be strategic. Chargeback alerts are your early-warning system, giving you a chance to act instead of just reacting. When an alert comes in, you get to choose your next move instead of being blindsided by a dispute you'll probably lose anyway.

An alert system lets you stand firm on your no-refund stance against obvious fraud, while strategically giving in on others to keep your merchant account in good standing.

Think of it this way: you can set up rules to automatically refund small-dollar disputes to protect your chargeback ratio. At the same time, you can flag the bigger, more suspicious claims to fight, saving you real money where it counts.

Stop letting preventable disputes drain your revenue. Disputely works directly with Visa RDR, Ethoca, and CDRN, giving you the power to resolve customer issues before they turn into costly chargebacks. Protect your merchant account and your bottom line—learn more at Disputely's official website.