Your Guide to the Payment Processing Fee

A payment processing fee is the price you pay to accept electronic payments like credit and debit cards. It’s not a single charge, though. Instead, it’s a bundle of different fees paid to the various players who help move money securely from your customer’s bank account to yours.

For most businesses, these fees add up to somewhere between 1.5% and 3.5% of each transaction.

What Exactly Is a Payment Processing Fee

I like to think of it as a toll for using the "digital highway" of commerce. When a customer taps their card or types in their details online, a complex process kicks off behind the scenes. Multiple financial institutions are involved, and each one takes a small slice of the transaction for their role in making the sale happen instantly and securely.

What you see as a single fee is actually made up of three separate costs. Getting a handle on these components is the first real step toward managing and, hopefully, reducing your payment expenses.

The Three Core Parts of Every Fee

Every single payment processing fee you pay can be broken down into the same three pieces. It doesn't matter which payment provider you use or what pricing plan you're on—these costs are baked into every transaction.

- Interchange Fee: This is the big one, often accounting for 70-80% of the total cost. This money goes straight to the customer's card-issuing bank (think Chase or Bank of America). It’s their compensation for taking on the risk of the transaction and for funding all those customer perks like cash-back rewards and airline miles.

- Assessment Fee: This is a much smaller, non-negotiable fee that goes directly to the card networks themselves, like Visa, Mastercard, or Discover. It's what they charge for building and maintaining the massive, secure payment networks everyone relies on.

- Processor Markup: This is the slice your payment processor (like Stripe, Square, or Authorize.net) keeps as their profit. It's the fee for their service—facilitating the transaction, providing the payment gateway, offering reporting tools, and handling customer support.

A common mistake is thinking your payment processor sets the entire fee. The reality is, they only control their own markup. Interchange and assessment fees are set by the card brands and issuing banks, so for most businesses, they’re not up for negotiation.

These three parts are added together to create the final processing fee that gets deducted from your revenue on every single sale. While you can't do much about interchange and assessment fees, the processor's markup is where you have some wiggle room to compare providers and find savings. We'll dig into exactly how these fees are calculated and what you can do about them next.

The Three Core Components of Every Transaction Fee

Every time a customer buys from you, the fee you pay isn't just one single charge. It’s actually a bundle of three distinct costs, each going to a different party in the payment chain. Think of it like a restaurant bill that includes the cost of the food, a service charge, and a tip.

Let's break down exactly what you're paying for. Understanding these three layers is the first step to figuring out where your money is going and where you might be able to save.

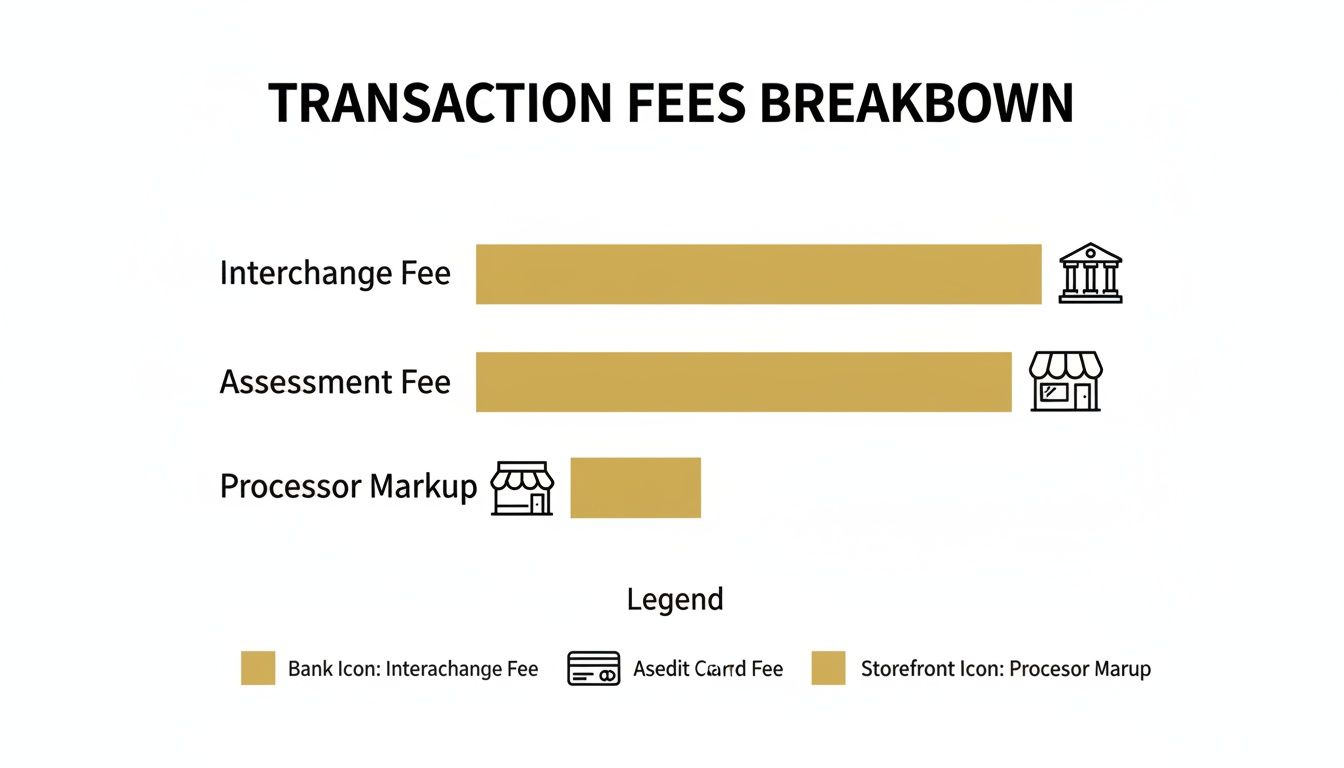

The Breakdown of a Typical Online Transaction Fee

Here's a look at how a single transaction fee is constructed, showing who gets paid and what a typical cost range looks like for an online sale.

| Fee Component | Paid To | Typical Cost Range (Online Transactions) |

|---|---|---|

| Interchange Fee | Customer's card-issuing bank (e.g., Chase, Bank of America) | 1.5% - 2.5% + $0.10 |

| Assessment Fee | Card network (e.g., Visa, Mastercard) | 0.13% - 0.15% |

| Processor Markup | Your payment processor (e.g., Stripe, Adyen) | Varies by provider and pricing model |

As you can see, the bulk of the cost is entirely out of your processor's hands. Now, let's dive into what each of these fees actually covers.

Interchange: The Big Slice

The first and by far the largest piece of the pie is the interchange fee. This typically accounts for a whopping 70-80% of your total processing cost.

This money doesn't go to your processor. Instead, it goes directly to the bank that issued your customer’s credit or debit card (think Capital One, Chase, etc.). Interchange is essentially their fee for taking on the risk of the transaction, covering potential fraud, and funding all those juicy rewards programs like airline miles and cash back.

The rates themselves are set by the major card networks, like Visa and Mastercard, and they're updated twice a year. They aren't one-size-fits-all, either. A transaction's risk level is a huge factor—an online payment where the card isn't physically present is riskier, and thus costs more, than an in-person chip-and-PIN purchase.

Even the type of card used matters. That fancy premium rewards card your customer just used? It costs you more to process than a standard debit card. This is why your "effective rate" can seem to jump around from month to month.

Assessment Fees: The Toll for Using the Highway

Next up is the assessment fee, sometimes called the card brand fee. This is a much smaller, non-negotiable fee paid directly to the card networks themselves—Visa, Mastercard, Discover, and American Express.

Think of it as their charge for building and maintaining the massive, secure payment highways that let money move around the globe instantly. It’s a small but necessary cost, usually hovering around 0.14% per transaction.

Processor Markup: The Only Part You Can Control

Finally, we have the processor markup. This is the only part of the fee that your payment processor—be it Stripe, PayPal, or someone else—actually pockets.

This is what you pay them for their technology, gateway services, customer support, and security features. It’s their business model. And most importantly, it's the one part of the entire fee structure that you can actually negotiate or shop around for.

Key Takeaway: You can't negotiate interchange or assessment fees; they're fixed costs set by the banks and card networks. Your real power lies in controlling the processor's markup by choosing the right partner and pricing model for your business.

When you add it all up, the total fee for a single transaction usually lands somewhere between 1.5% to 3.5%. For online "card-not-present" sales, you can expect your total costs to be in the 2.25%–2.50% range. This is after combining all the components, including interchange rates from Visa (up to 2.40% + $0.10) and Mastercard (up to 2.50% + $0.10).

Of course, transaction fees are just one piece of the puzzle. If you're using a platform like Kickstarter, you also have to consider their cut. It's helpful to understand what percentage Kickstarter takes from creators to see how different fees can stack up.

How Processing Fees Are Calculated with Real Examples

Theory is one thing, but seeing how these fees chip away at a real transaction is what really matters. Let's make these abstract costs tangible by running the numbers on the same $100 online purchase through two common pricing models. You'll see just how much the final cost can swing.

Example 1: The Flat-Rate Model

You've likely seen this model from processors like Stripe and Square. It's popular for a reason: it's incredibly simple. All three fee components—interchange, assessments, and the processor’s cut—are bundled into a single, predictable rate.

Let's use a standard flat rate of 2.9% + $0.30.

- Percentage Fee: $100.00 x 2.9% = $2.90

- Fixed Fee: + $0.30

- Total Fee: $3.20

The big appeal here is predictability. You know exactly what you'll pay every single time, no matter what card your customer uses. But that convenience can come at a premium, especially as your transaction volume grows.

Example 2: The Interchange-Plus Model

Now, let's process that same $100 sale using an Interchange-Plus model. This approach is more transparent because it breaks out each fee component, so you can see precisely where your money is going.

For this example, let's plug in some competitive, real-world rates:

- Interchange: 1.8% + $0.10 (a typical rate for a standard consumer credit card, not a fancy rewards card)

- Assessment: 0.14% (a blended estimate for Visa and Mastercard network fees)

- Processor Markup: 0.20% + $0.10 (a fairly competitive markup)

Here’s how the calculation unfolds:

- Interchange Fee: ($100.00 x 1.8%) + $0.10 = $1.90

- Assessment Fee: $100.00 x 0.14% = $0.14

- Processor Markup: ($100.00 x 0.20%) + $0.10 = $0.30

- Total Fee: $1.90 + $0.14 + $0.30 = $2.34

The Bottom Line: On the exact same $100 sale, the Interchange-Plus model was $0.86 cheaper. It might not sound like much, but multiply that by hundreds or thousands of transactions a month, and the savings start to look very real.

This chart really drives home how those separate fees—the interchange going to the customer's bank, the assessment for the card network, and your processor's markup—stack up.

What this shows is that the lion's share of your fee isn't even going to your processor; it's passed through to the bank that issued your customer's card. This is why Interchange-Plus pricing is so powerful. While flat-rate offers simplicity, Interchange-Plus hands the control back to you, often leading to a much lower effective rate once you're ready to handle a little more detail on your statements.

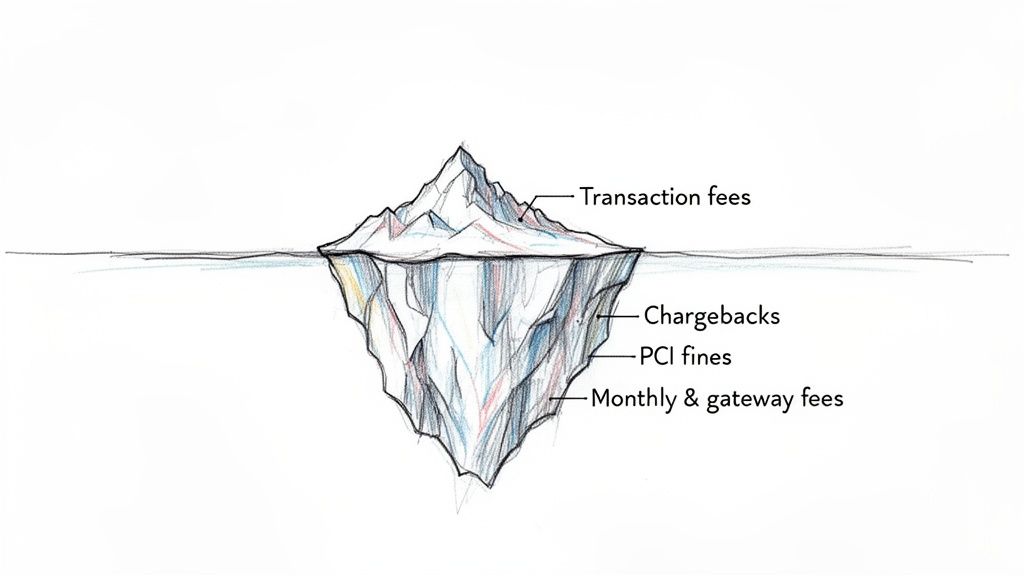

The Hidden Costs Quietly Sinking Your Profits

When you look at your payment processing statement, the transaction fees you see are just the tip of the iceberg. What’s lurking beneath the surface are the less obvious costs that can seriously erode your profit margins, turning a seemingly small expense into a major financial headache.

These hidden costs aren't just about the simple percentage and per-transaction rates. We're talking about monthly account fees, payment gateway charges, and steep penalties if you fall out of PCI DSS compliance. It's a reminder to always dig deeper, especially when evaluating tools that seem too good to be true, and understand the high cost of 'free' event software.

Why Chargebacks Are So Damaging

Of all the hidden costs, chargebacks are by far the most destructive. A chargeback isn't just a refund; it’s a triple-threat penalty.

First, you lose the revenue from the sale. Then, you're out the product you already shipped. And to top it off, your processor smacks you with a separate chargeback fee, which typically runs from $15 to $100 per incident. The worst part? You pay that fee even if you win the dispute.

These penalties add up fast, but the real threat is your dispute ratio—the percentage of chargebacks you get compared to your total transactions. Once that ratio creeps over the 0.9% threshold set by Visa and Mastercard, your business is in hot water.

A high dispute ratio is a huge red flag for payment processors. It screams "risk," and they react accordingly. This can lead to hefty monthly fines, having your funds frozen in a reserve account, or even losing your merchant account entirely.

You Can’t Afford to Be Reactive

The financial fallout from disputes is massive. For many ecommerce businesses, chargebacks and their associated costs can tack on an extra 1–2% to their total cost of sales. That’s on top of the 1.5%–3.5% you’re already paying in direct transaction fees.

Think about it: for a merchant on a platform like Shopify or Stripe, a single chargeback can easily cost over $250 when you factor in lost revenue, the cost of goods, and the administrative time spent fighting it. This is why proactive management isn't just a nice-to-have; it's a critical survival strategy. Getting hit with a payment hold can be devastating, a problem we cover in detail here: https://disputely.com/shopify-hold.

Luckily, you're not helpless. Modern alert systems from providers like Ethoca and CDRN give you a crucial 24-72 hour heads-up, allowing you to refund a transaction before it officially becomes a chargeback.

By using these tools, you can stop disputes from ever tainting your record and slash your chargeback rate by up to 99%. This proactive approach is the single most effective way to protect your profits and maintain a healthy relationship with your payment processor.

Actionable Strategies to Lower Your Payment Processing Fees

Okay, so you understand the fees. Now what? Just accepting them as a fixed cost of doing business is a mistake. The good news is you have more control than you think.

With a few smart moves, you can start chipping away at what you pay on every single transaction, and that money goes straight back to your bottom line. It’s not about finding some magic bullet; it’s about being proactive. Let’s walk through the most effective ways to cut your processing costs.

Negotiate Your Processor's Markup

This is your biggest opportunity. The one part of your bill that isn't set in stone by the card networks is your processor's markup. As your sales grow, so does your negotiating power. Processors want to keep high-volume merchants happy, which gives you the leverage you need to ask for a better deal.

Don't go into that conversation empty-handed. First, calculate your current "effective rate"—just divide your total monthly processing fees by your total monthly sales. Then, get quotes from a couple of competitors. With that data in hand, call your current provider and ask them to match or beat the other offers. You’ll be surprised how often they’re willing to play ball to keep your business.

Optimize for Lower Interchange Rates

While you can't directly change the interchange rates Visa and Mastercard set, you can influence which rate bucket your transactions fall into. This is called interchange optimization, and it’s all about sending more detailed transaction data to the customer's bank.

By passing along this extra info—known as Level 2 and Level 3 data—you're essentially proving the transaction is legitimate and low-risk. The bank rewards you with a lower interchange fee.

- Level 2 Data: This goes beyond the basics to include things like sales tax amount and a customer code.

- Level 3 Data: This is even more detailed, including all Level 2 info plus specific line-item details like product descriptions, quantities, and shipping data.

This is a game-changer for B2B and B2G businesses, where the savings can be massive. Talk to your payment gateway or processor to make sure your system is set up to pass this data through automatically.

The most overlooked strategy for cost reduction isn't about shaving fractions of a percent off transaction fees. It's about eliminating the massive, unpredictable penalties that come from chargebacks.

Proactively Eliminate Chargeback Fees

Chargebacks are silent profit killers. Each one slaps you with a non-refundable fee of $15-$100 on top of the lost revenue and product. Honestly, the single best way to lower your total payment costs is to stop these disputes before they even start.

This is where chargeback alert services are indispensable. These tools plug into networks like Ethoca, CDRN (Cardholder Dispute Resolution Network), and RDR (Rapid Dispute Resolution) to give you a heads-up the moment a customer complains to their bank.

This alert opens a crucial 24-72 hour window for you to issue a refund and resolve the issue directly. By doing so, the dispute never escalates into a formal chargeback. You completely avoid the penalty fee, protect your merchant account’s health, and keep your dispute ratio low.

Of course, preventing them is step one. For businesses looking to reclaim lost revenue, exploring strategies for effective chargeback representment is the essential next step to fight and win disputes that couldn't be prevented.

Time for a Payment Processor Audit: Your Checklist

Think of this as a financial health checkup for your business. You wouldn't just accept a doctor's bill without looking at the line items, right? The same goes for your payment processing statement. Instead of just paying it every month, it's time to dig in and see if you're leaving money on the table.

This simple audit will help you decode your current setup, understand what you're really paying, and find those hidden savings.

Step 1: Grab Your Last Three Monthly Statements

Your statement is a treasure map, but you need to know how to read it. Let's break it down.

What's Your Pricing Model? First, figure out what kind of plan you're on. Is it flat-rate, tiered, or Interchange-Plus? If you see a laundry list of different interchange codes and tiny percentage rates, you’re almost certainly on Interchange-Plus. If you just see a single, predictable rate on every transaction (like 2.9% + $0.30), that’s the signature of a flat-rate model.

Calculate Your "Effective Rate": This is the single most important number to know. It cuts through all the noise. Just divide your total processing fees for the month by your total sales volume. For example, if you paid $1,200 in fees on $40,000 in sales, your effective rate is 3.0%. Do this for the last three months to see if it’s consistent or creeping up.

Hunt for Hidden Fees: Scan for any line items that aren't tied directly to transactions. Are you getting hit with monthly account fees, PCI compliance fees, gateway fees, or batch fees? These little charges can add up to a big problem over time.

The global payment processing world is massive, expected to reach $147 billion by 2032. With that growth comes more transactions, but also more risk. In 2023 alone, fraud and disputes hit a staggering 71% of businesses. It's a reminder that these "small" costs are a major part of the industry's bottom line—and yours.

Step 2: Ask Yourself These Key Questions

With your statements in front of you, it's time for an honest assessment. The answers will tell you everything you need to know about your current deal.

- If I'm on Interchange-Plus, what is my processor’s actual markup?

- What is my true effective rate, and how does it stack up against industry averages?

- How much did I lose to chargeback fees over the last three months?

- Is my chargeback ratio staying safely below the 0.9% danger zone?

- Am I paying for bells and whistles in my plan that I never actually use?

Once you've answered these, you'll have a crystal-clear picture of where you stand. This information is your leverage—either to negotiate a better deal with your current processor or to shop around for a new one with confidence.

To get an idea of how specialized services can tackle these costs head-on, you can see how we handle it with our straightforward pricing.

Got Questions About Payment Fees? We've Got Answers.

Diving into payment processing fees can feel like you're trying to read a foreign language. It's confusing, but getting a handle on the common questions is the first step to controlling your costs and keeping your business financially healthy.

Let's break down a few of the questions we hear all the time from merchants. No jargon, just straight answers to help you make smarter decisions.

Can I Get Rid of Processing Fees Completely?

The short answer is no. If you want to accept credit or debit cards, processing fees are just part of the deal. Think of them as the cost of admission for using the secure, global infrastructure built by card networks like Visa and Mastercard and the banks behind them. The core components—interchange and assessment fees—are non-negotiable.

But that absolutely does not mean you're stuck with the rate you have now. You can (and should) take steps to reduce your total costs. The real savings come from negotiating your processor's markup, making sure your transactions qualify for the lowest possible interchange rates, and aggressively fighting costly chargebacks.

What's a Good Payment Processing Rate, Anyway?

This is the million-dollar question, and the answer is: it depends. A "good" rate for a brand new coffee shop is very different from a good rate for a high-volume subscription box.

- If you're just starting out or have lower sales volume: A simple flat-rate plan (like the common 2.9% + $0.30) is often your best bet. It's predictable and easy to understand.

- If you're processing a lot of transactions: You should be on an Interchange-Plus plan. A competitive markup here might look something like 0.20% + $0.10 on top of the base interchange cost, which almost always results in a lower overall rate.

Forget the advertised rate. The only number that truly matters is your effective rate—your total fees divided by your total sales volume. For most e-commerce businesses, getting that number below 2.5% is a great sign that your fees are well-managed.

How Do Chargeback Alerts Actually Lower My Fees?

This is a fantastic and often overlooked way to cut costs. Chargeback alerts from services like RDR, CDRN, and Ethoca are your early-warning system. When a customer disputes a transaction with their bank, these alerts give you a crucial 24-72 hour window to simply refund the customer before the bank finalizes it as a formal chargeback.

By issuing that refund, you completely sidestep the punishing $15-$100 penalty fee that processors slap on every single dispute—a fee you have to pay even if you win. It's a proactive way to stop the financial bleeding before it even starts, protecting both your revenue and your relationship with your processor.

Stop letting preventable disputes drain your bank account. Disputely connects directly to your payment processor to resolve these alerts automatically, eliminating up to 99% of chargebacks before they ever become a problem. See how much you could be saving.