Processing Recurring Payment: Master Subscriptions & Reduce Failures

Think of processing a recurring payment as the automated financial heartbeat of any subscription business. Instead of having to chase down customers with an invoice every single month, it's a 'set-it-and-forget-it' system that automatically handles charges for ongoing services, from software access to a monthly gym membership.

What Is Recurring Payment Processing and Why It Matters

At its simplest, processing a recurring payment is what lets a business automatically charge a customer on a regular schedule—be it weekly, monthly, or yearly. The customer provides their payment details once, and the system takes care of the rest. This single, automated handshake is the quiet engine behind giants like Netflix and Spotify, and it's what makes your favorite subscription box show up on time.

This isn't just a niche convenience; it's a fundamental shift in how commerce works. The global subscription economy, built on this very process, was already worth $650 billion back in 2020. Projections show it rocketing to an incredible $1.5 trillion by 2025. That kind of growth tells you everything you need to know about where consumer habits and business models are headed. You can read more about why merchants are shifting their focus in these insights on recurring payments.

The Core Benefits for Your Business

Moving to a recurring payment model does a lot more than just make getting paid easier. It fundamentally changes the financial stability and scalability of your business. The ripple effects go far beyond simply collecting revenue on schedule; they can reshape your entire operational outlook.

For any company looking to build something that lasts, getting this process right isn't optional. It’s the first real step toward turning unpredictable, one-off sales into a reliable financial foundation you can build on.

At its core, recurring billing is about creating a predictable and frictionless financial relationship with your customers. It removes manual effort, reduces payment failures, and ultimately builds a more resilient revenue stream.

Key Benefits of Recurring Payments for Merchants

Let's break down the tangible benefits of setting up a solid recurring payment system.

| Benefit | Impact on Business | Example |

|---|---|---|

| Predictable Revenue | Creates a stable, forecastable income stream, making budgeting and strategic planning far more accurate. | A SaaS company knows it will have a baseline of $50,000 in revenue at the start of each month, allowing it to confidently hire a new developer. |

| Improved Customer Retention | Automating payments removes a major point of friction, reducing involuntary churn from expired cards or forgotten bills. | A meal-kit service avoids losing customers just because they forgot to manually pay their monthly invoice. The service just continues. |

| Lower Administrative Costs | Frees up your team from the manual, time-consuming work of invoicing, sending reminders, and chasing late payments. | Instead of spending hours on billing, your support team can focus on helping customers and improving the product experience. |

These advantages work together to create a much healthier and more efficient business model.

Key Advantages Explained

When you get this system dialed in, you unlock some powerful improvements that directly affect your bottom line and how your team spends its time. The most important wins are:

Predictable Revenue Streams: This is the big one. Recurring payments give you a consistent, forecastable flow of cash. That stability means you can budget accurately, plan for the future with confidence, and make smarter investments in your company's growth.

Enhanced Customer Retention: A smooth, invisible payment process keeps customers happy and subscribed longer. You eliminate the "accidental churn" that happens when a customer has to manually pay an invoice and simply forgets. This directly boosts their lifetime value (LTV).

Reduced Administrative Workload: Think of all the time spent sending invoices, following up on late payments, and manually keying in charges. Automation wipes that off your team's plate, freeing them up for work that actually grows the business, like customer support or product development.

By setting up this automated framework, you're not just collecting money more efficiently—you're building a more scalable and resilient business. Of course, protecting that revenue means understanding how to handle risks like chargebacks, a topic we cover in detail on the Disputely blog.

The Complete Lifecycle of a Recurring Payment

To really get a handle on your recurring revenue, you need to peek behind the curtain and see what happens when a subscription renews. A recurring payment isn't a one-and-done event; it's a series of automated handoffs that move money from your customer's bank to yours.

Think of it like an automated assembly line. Each station performs a specific job before passing the task to the next. If any part of that line breaks down, the whole process grinds to a halt. It all starts the moment a customer signs up for your service.

The Initial Handshake and Tokenization

The journey kicks off when a new customer subscribes. They punch their credit card details into your checkout page, and that information is securely zipped over to your payment gateway.

This is where a crucial step called tokenization happens. Instead of holding onto the actual, sensitive card number (a major security risk), the gateway swaps it for a unique, meaningless string of characters—the "token." This token is like a secure alias for the card. It lets you charge the customer again without ever storing or handling their raw credit card data, which is a must-have for PCI compliance.

Your system saves this token, not the card number, and uses it for every future charge.

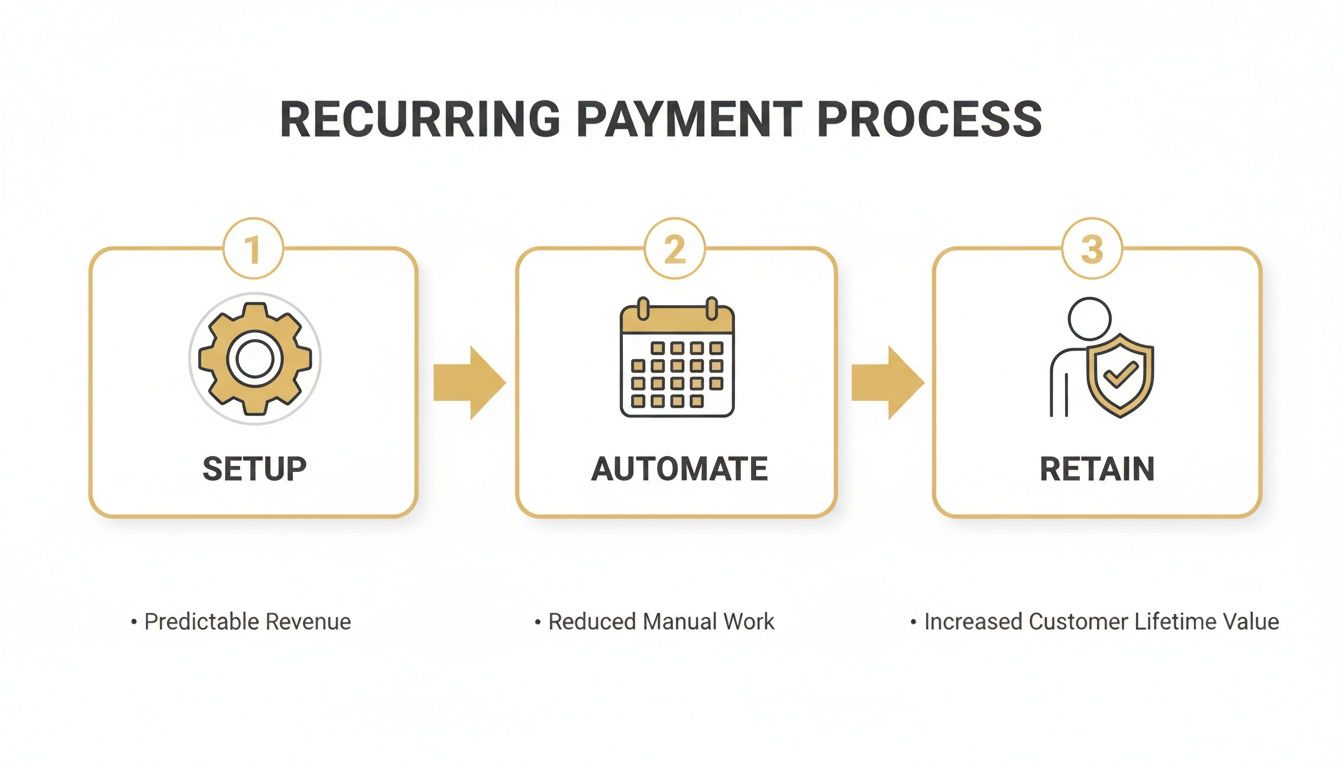

This diagram breaks down the core flow: setting up the subscription, automating the charges, and ultimately, retaining your hard-won customers.

As you can see, this isn't just about the technical nuts and bolts; it’s a strategy for building a predictable, sustainable business.

The Automated Billing Cycle in Action

When a customer's renewal date rolls around, your subscription software automatically wakes up and gets to work. This is where the real magic of processing recurring payment happens.

Here’s the play-by-play:

- The Trigger: Your system pings your payment gateway, sending a payment request using the customer's stored token.

- Gateway to Processor: The gateway securely forwards this request to your payment processor, who acts as the go-between connecting you to the global banking networks.

- Authorization Request: The processor routes the transaction to the right card network (think Visa, Mastercard, or Amex). The card network then knocks on the door of the customer's issuing bank (like Chase or Bank of America).

- The Bank's Decision: The customer's bank is the final gatekeeper. It quickly checks for sufficient funds, confirms the card isn't expired or reported stolen, and runs its own fraud analysis. It then sends back a simple "approved" or "declined" message.

- Communication Back: The approval or decline message travels all the way back up the chain—from the bank to the card network, to the processor, and finally back to your system.

The wild part? This entire round trip, from your system's trigger to the bank's final decision, usually takes just 1-3 seconds. It’s this lightning-fast communication that makes modern subscriptions feel so effortless.

Settlement and Completion

Once a charge gets the green light, the final step is settlement. This is where the money actually moves. The customer's bank sends the funds to your merchant account, a special bank account for receiving card payments.

This transfer typically takes 24-72 hours. After the funds have settled in your merchant account, you can move them into your main business bank account.

Of course, if the payment is declined, that’s a different story. Your system will get a specific decline code, which is your first clue for figuring out what went wrong—a topic we’ll dive into next.

Understanding Why Recurring Payments Fail

A failed recurring payment is more than just a missed transaction; it's a potential crack in the foundation of your customer relationship. In fact, these failures are the single biggest driver of involuntary churn—when you lose a customer not because they wanted to leave, but because their payment simply didn't go through.

Getting a handle on why these payments fail is the first step to building a more resilient revenue model. Most payment declines fall neatly into one of two buckets.

Hard Declines: The Permanent Roadblocks

Think of a hard decline as a permanent "No." The customer's bank is sending a clear signal: this transaction won't work, and trying it again with the same card information is a waste of time. These are show-stopping issues that can only be resolved by the customer.

Common causes of hard declines include:

- Closed Account: The bank account or credit card account linked to the payment is no longer active.

- Invalid Card Number: The card number you have on file is just plain wrong, maybe from a typo during the initial signup.

- Stolen or Lost Card: The card has been flagged as stolen or lost, so the issuing bank has put a hard stop on all transactions.

When you encounter a hard decline, retrying the charge is futile. Your only real move is to reach out to the customer and ask them to update their payment method.

Soft Declines: The Temporary Hurdles

A soft decline, on the other hand, is more like a temporary hiccup. The bank isn't saying "never," it's just saying "not right now." The underlying issue is often fixable, and this is where a smart strategy for processing recurring payment can salvage a ton of otherwise lost revenue.

Soft declines represent a critical opportunity. While a hard decline is a definitive stop, a soft decline is often just a temporary glitch. A smart retry strategy can turn many of these potential losses back into successful payments.

These temporary failures are far more common and usually come down to simple, everyday problems.

Here’s what’s typically behind a soft decline:

- Insufficient Funds: This is the big one. The customer just doesn't have enough money in their account when you try to run the charge.

- Expired Card: The card on file has simply passed its expiration date. This alone accounts for a huge slice of involuntary churn.

- Suspected Fraud: The bank's fraud detection algorithms got a little too aggressive and flagged a perfectly legitimate transaction.

- "Do Not Honor": This is a generic, catch-all decline from the customer's bank. It can mean anything from the customer hitting a daily spending limit to the bank just being overly cautious.

With every soft decline, your payment processor gives you a decline code. Learning to read these codes is the key to recovering the payment. An "Insufficient Funds" code tells you to wait a few days—maybe until after payday—and try again. An "Expired Card" code is your cue to fire off an automated email asking the customer to update their details. This kind of targeted response is what effective dunning and revenue recovery are all about.

How to Reduce Payment Failures and Prevent Disputes

Protecting your revenue stream isn’t just about getting that first transaction to go through. It’s about building a defense system that anticipates and stops failures and disputes before they ever happen. A proactive strategy doesn't just save a sale—it strengthens customer trust and keeps your merchant account in good standing.

Let's move past the theory. Smart merchants use a layered approach to fight back against involuntary churn and those dreaded, costly chargebacks. This means automating the right communications, being strategic about retrying failed payments, and keeping customer payment details up-to-date without making them do all the work.

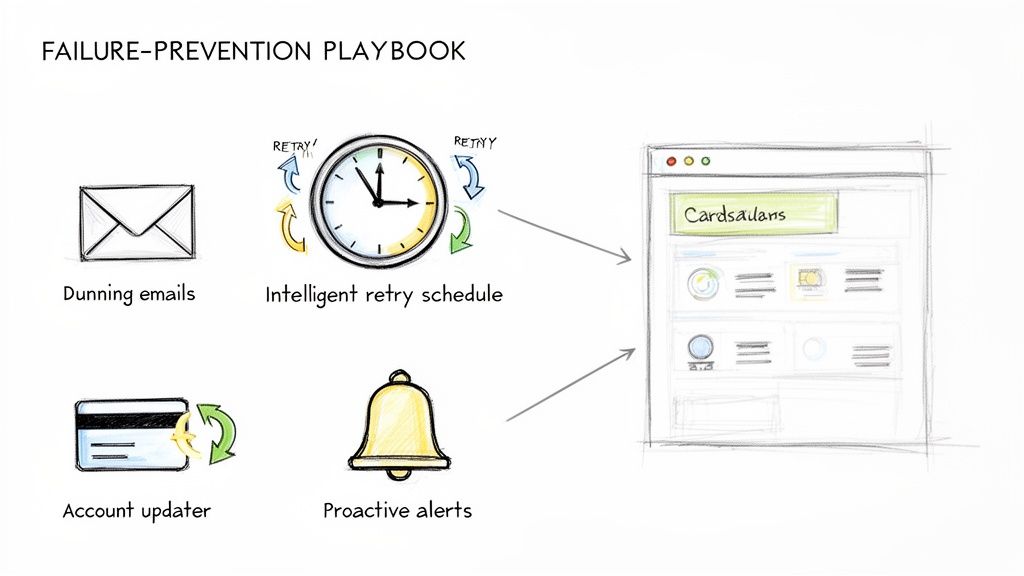

Implement Smart Dunning Management

At its core, dunning is just the process of communicating with customers about payments. A smart dunning strategy, however, turns these communications into friendly, automated reminders that solve problems ahead of time. Forget the generic "your payment failed" email.

Instead, you can tailor your outreach to the specific situation:

- Pre-Dunning: Send a helpful heads-up a few days before a card is about to expire, giving the customer a gentle nudge to update their info.

- Payment Failure Notices: The moment a soft decline happens, an instant notification with a direct, secure link for the customer to update their payment method can resolve the issue in minutes.

This approach feels helpful, not accusatory, which goes a long way in keeping your customers happy.

Use Intelligent Retry Schedules

When a payment fails with a soft decline, hitting the "retry" button over and over is a recipe for disaster. It’s inefficient and can even get you flagged by payment networks. An intelligent retry schedule, on the other hand, uses the specific decline code to decide when and how often to try again.

Think about it: a charge declined for "Insufficient Funds" probably won't go through an hour later. A smart system knows to wait a few days, maybe even timing the next attempt to line up with common paydays. This data-driven logic dramatically boosts your chances of recovering the sale. For membership-based businesses like gyms, having the right software in place is crucial to avoid the headache of chasing failed payments.

Key Takeaway: An intelligent retry strategy doesn't just hammer the payment gateway. It analyzes the reason for the failure and makes a calculated decision on when to try again, turning likely losses into recovered revenue.

Leverage Account Updater Services

A massive number of soft declines come from a simple, unavoidable problem: expired or replaced cards. This is where Account Updater services become a complete game-changer. Offered by major card networks like Visa and Mastercard, these services work behind the scenes to automatically check for and update the card details you have on file.

If a customer’s bank issues them a new card with a new expiration date or even a new number, Account Updater can refresh that information in your system automatically. No action is needed from you or your customer. It’s a seamless process that prevents a huge chunk of payment failures before they even get a chance to happen.

Stop Disputes with Proactive Alerts

Your final line of defense is stopping disputes before they escalate into full-blown chargebacks. As subscriptions become the norm, customers are more focused on security than ever—in fact, 91% of customers consider payment security essential. This is huge, especially as the recurring payments market is expected to hit $198.5 billion by 2030.

Tools from networks like Ethoca and Verifi can give you real-time alerts the second a customer initiates a dispute with their bank. This opens up a critical 24-72 hour window for you to step in and issue a refund directly. By doing so, you prevent the issue from becoming a formal, damaging chargeback on your merchant record.

Choosing the Right Recurring Payment Processor

Picking a partner to handle your recurring payments isn't just about choosing a vendor. It's a major strategic decision that will directly shape your company's growth. Think of your processor as the engine driving your revenue; the right one does more than just move money—it helps you protect and grow your bottom line.

This decision is more important than ever. The global payment processing market is expected to manage a staggering $157 trillion in transactions by 2025. This explosion in volume really highlights the need to find a partner who can securely and reliably manage your slice of that pie.

Core Features for Subscription Businesses

Here’s the thing: not all payment processors are created equal, especially when it comes to subscriptions. A generic processor might be fine for one-off sales, but it will fall short when you need specialized tools to manage recurring revenue and keep churn low.

For any serious subscription business, these features are non-negotiable:

- Smart Dunning Management: This is all about automated, intelligent communication. It handles everything from reminding customers about upcoming payments to alerting them when a transaction fails, all without you lifting a finger.

- Intelligent Retries: Instead of just retrying a failed payment over and over, this uses data-driven logic. It looks at why a payment failed and retries it at the most optimal time, dramatically increasing your recovery rates.

- Account Updater Services: This is a lifesaver. It automatically updates expired or replaced card details in the background, tackling one of the biggest causes of involuntary churn before it even happens.

Evaluating Security and Integration

Beyond the subscription-specific tools, you need to look at the processor's technical foundation. Top-notch security and smooth integration are the bedrock of a solid payment system. They keep customer data safe and your operations running efficiently.

Your payment processor should act as a fortress for your customers' data and a seamless bridge for your developers. Prioritizing robust security like tokenization and a well-documented API isn't just a best practice—it's essential for building trust and scaling effectively.

As you evaluate potential partners, keep your focus on these two pillars:

- Rock-Solid Security: PCI compliance is just the starting point. Make sure the processor uses tokenization to protect sensitive card data. This shields you from a massive security and compliance headache.

- Developer-Friendly API: A well-documented, flexible API is a gift to your tech team. It lets them integrate the payment system into your website, app, or CRM with minimal friction. Before you commit, check out our guide to getting started with Stripe.

Finding a processor that aligns with your specific niche is key. For example, specialized solutions like online giving platforms for churches offer features designed specifically for managing donations. This just goes to show how critical it is to find a partner whose capabilities are a perfect match for your business model.

Weaving in Chargeback Alerts to Safeguard Your Revenue

While your payment processor is the engine driving every transaction, a dedicated chargeback alert system is your safety harness. These platforms don't actually process any payments. Instead, they plug into your current setup with one laser-focused mission: to stop chargebacks in their tracks.

Think of it this way: your processor is the cashier handling all the money coming in. An alert service is the friendly store manager who steps in to resolve a customer's issue before they feel the need to escalate it. This is an absolutely vital layer of protection when you're processing recurring payment transactions, which are notorious for causing customer confusion and disputes.

How Real-Time Alerts Give You a Heads-Up

Platforms like Disputely integrate directly with the big card networks, like Visa and Mastercard. The second a customer calls their bank to question a charge, that network pings the alert platform.

This opens up a precious window of time—usually just 24-72 hours—for you to jump in and fix things. Instead of getting blindsided by a formal chargeback weeks down the road, you get an immediate notification.

This brief window is everything. It flips the script from a reactive, expensive chargeback battle to a proactive, customer-focused resolution. You get a chance to solve the problem directly, saving both the sale and the customer relationship.

Within that window, you can issue a refund straight to the customer. This simple action satisfies their bank and stops the dispute from ever becoming a full-blown chargeback. It’s an automated intervention that can mean the difference between keeping a happy subscriber and getting a black mark on your merchant account.

For businesses dealing with payment holds, preventing these disputes is non-negotiable. If you're struggling with this, you can learn more about what to do if you have a Shopify Payments account hold in our guide. By proactively stopping chargebacks, you're ultimately protecting your ability to do business.

Frequently Asked Questions About Recurring Payments

Even with the best strategy laid out, you're bound to run into specific questions once you start processing recurring payments. Getting straight, practical answers is key to running your subscription model with confidence and sidestepping those common, costly mistakes.

Let’s tackle some of the most common questions we hear from merchants.

What Is the Difference Between a Payment Gateway and a Payment Processor?

It helps to think of it like a secure mail service.

The payment gateway is the digital equivalent of an armored truck. It securely picks up your customer's sensitive card details from your website and transports them. The gateway itself never actually touches the money.

The payment processor is the central sorting facility. It takes that secure package of data, talks to the customer's bank (the issuing bank) and your bank (the acquiring bank) to get the transaction approved, and makes sure the money actually moves from their account to yours. For recurring billing to work, you absolutely need both of them operating in lockstep.

How Does Strong Customer Authentication Affect Subscriptions?

Strong Customer Authentication (SCA) is a security measure, primarily in Europe, that requires customers to provide two forms of verification for many online payments. It can sound scary for subscription businesses, but it's usually less of a headache than you'd think.

For most subscription models, SCA only applies to the very first transaction when the customer signs up.

Once they've authenticated that initial payment, the subsequent charges you initiate are typically exempt. The key is ensuring your payment processor is set up to flag these follow-up transactions correctly as "merchant-initiated" to prevent them from being declined. Get this right, and the renewal process stays smooth for your European customers.

Why Is Tokenization Essential for Subscription Businesses?

Tokenization isn't just a "nice-to-have"; it's a foundational security practice for any business that bills customers on a recurring basis.

Here's how it works: instead of storing a customer's actual credit card number, the system replaces it with a unique, randomly generated string of characters—the "token."

By storing this token instead of the raw card data, you can initiate future charges without ever holding sensitive information on your servers. This dramatically reduces your PCI compliance burden and protects your business and your customers from data breaches. It's the standard for secure recurring billing.

Stop losing revenue to preventable chargebacks. Disputely integrates with your payment processor to provide real-time alerts, giving you the chance to refund a dispute before it becomes a costly problem. Protect your merchant account and secure your revenue today.