Real-Time Transaction Monitoring Explained

Picture a security guard at your checkout, giving every single payment a split-second inspection before it goes through. That's the essence of real-time transaction monitoring. It’s a system designed to analyze transactions as they’re happening to shut down fraud, head off chargebacks, and ultimately, protect your bottom line.

Understanding Real-Time Transaction Monitoring

Real-time transaction monitoring is all about automation that kicks in the exact moment a customer hits "buy." It's a world away from older, batch-based reviews that might look at transactions hours or even days later. Think of it as having a bouncer at the door instead of just reviewing security tapes after the fact.

For any e-commerce or subscription business, this speed isn't just a nice-to-have; it's a necessity. Fraudsters move at the speed of the internet. If you're waiting minutes to spot a sketchy transaction, you're already too late. The money is gone, the product is shipped, and an expensive chargeback is already in the mail.

The Core Purpose of Instant Analysis

At its heart, the goal is to spot and block fraud before you lose any money. The system sifts through hundreds of data points for every single transaction, looking for tell-tale signs of trouble. But the benefits run much deeper than just catching thieves.

A solid real-time monitoring setup is foundational for a healthy payment operation. It empowers your business to:

- Prevent Revenue Loss: You stop fraudulent payments cold, avoiding not just the direct financial loss but also the painful chargeback fees that come with it.

- Protect Your Merchant Account: Payment networks like Visa and Mastercard keep a close eye on chargeback rates. Staying on top of fraud keeps your dispute ratio low, ensuring you don't risk your ability to process payments at all.

- Improve Customer Experience: A smart system is surgical. It declines only truly high-risk orders, letting legitimate customers sail through checkout without a hitch. This prevents the frustration of false declines and builds genuine trust.

Simply put, real-time transaction monitoring is your business's immune system. It’s constantly on patrol, identifying and neutralizing threats before they can do any real harm, moving you from a reactive cleanup mode to a proactive defense.

Why Every Millisecond Matters

Think about how fast an online purchase happens. A customer clicks, and they expect an immediate "thank you" page. Your monitoring system has to make its decision within that incredibly brief window, before the payment is even finalized.

This instant verdict is what makes modern fraud prevention so powerful. It’s analyzing a constant stream of transaction data, catching anomalies as they fly by. Maybe it's a purchase coming from a known high-risk location, or a brand-new account trying to place a dozen orders in a minute. By catching these red flags instantly, you stop the entire domino effect of a successful fraudulent transaction: lost goods, lost revenue, and a black mark on your processing history.

The Dangers of Delayed Fraud Detection

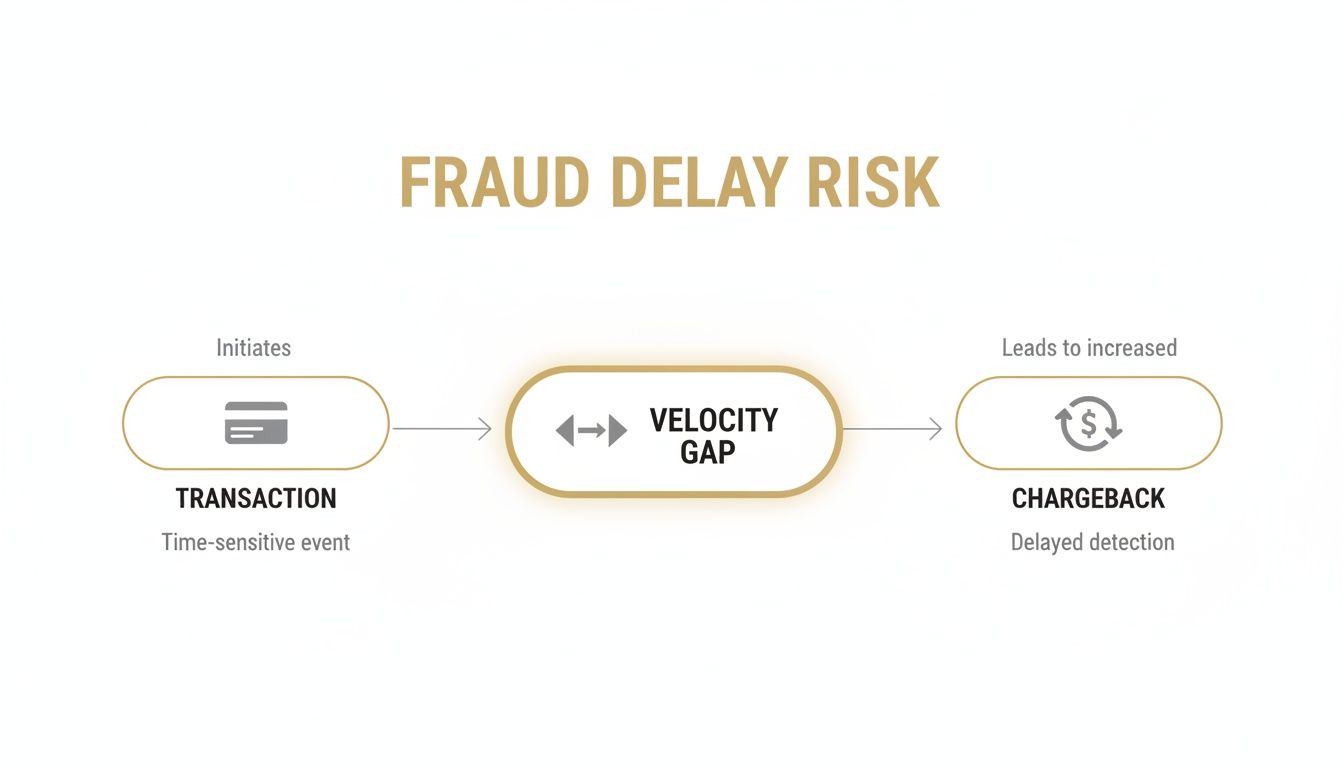

In e-commerce, speed is the name of the game. Faster checkouts, instant downloads, next-day shipping. But that relentless focus on speed creates a dangerous blind spot for merchants: the Velocity Gap.

This is the critical window of time between when you approve a transaction and when you actually realize it was fraudulent. It’s like a bank vault with a time-delayed lock. Once a fraudster is inside and has the cash, the door is wide open, and getting it back is next to impossible.

While you're processing a "sale," a criminal could be long gone with your merchandise and the actual cardholder's money. From the moment a stolen card is used to the instant a digital good is delivered or a package is shipped, the entire heist often happens before older, slower fraud systems even raise an eyebrow.

How Fraudsters Exploit The Delay

Fraudsters are all about speed and automation. They build their entire strategy around exploiting any delay in your detection process, knowing that the faster they can get in and out, the higher their chances of success. That gap gives them the cover they need to scale their attacks without being noticed.

They don't just use brute force, either. Their methods are often designed to look legitimate on the surface:

- Account Takeovers (ATO): Why steal a credit card when you can steal a whole customer account? By getting into a real customer's profile, they use the saved payment info and purchase history to make fraudulent orders look completely normal.

- Rapid-Fire Attacks: Using bots, criminals can run thousands of stolen credit card numbers across countless websites in just a few minutes. They're just looking for the ones that work before the real cardholder even knows their information has been compromised.

- Social Engineering Scams: These attacks are trickier. Fraudsters manipulate legitimate customers into authorizing payments, making the transaction appear completely authentic to a simple, rule-based system.

The Velocity Gap isn't just a delay; it's an open invitation for criminals. Every minute your system waits to connect the dots on a suspicious transaction gives them a massive head start, turning your payment gateway into their personal exit ramp.

The Cascading Consequences For Merchants

When a fraudulent transaction slips through, the damage goes way beyond the cost of the lost product. It sets off a painful and expensive chain reaction that can seriously harm your bottom line and your reputation.

The first domino to fall is the chargeback. The legitimate cardholder spots the charge, calls their bank, and the money is clawed back from your account—plus a hefty fee for your trouble. Get too many of these, and things get serious, fast. You can dive deeper into this topic in our guide on chargeback representment strategies.

This problem is only getting worse as payments get faster. Global Real-Time Payment (RTP) volume jumped by a massive 42% in 2023 alone, but this innovation has made the Velocity Gap even wider. A recent survey found that 21% of firms now admit that a lack of immediate risk visibility is the single biggest weakness in their financial crime prevention. To learn more, discover key insights on closing the velocity gap in real-time payments.

Once your chargeback rates start to climb, the card networks like Visa and Mastercard will notice. If your chargeback-to-transaction ratio creeps over their thresholds (usually around 0.9%), you risk being placed into one of their costly monitoring programs. These programs bring steep monthly fines and intense scrutiny, putting your entire ability to process payments on the line. This is exactly why "real-time" monitoring isn't a luxury anymore—it's an absolute necessity for survival.

How Real-Time Monitoring Technology Works

So, how does a system actually decide to approve or deny a transaction in less time than it takes to blink? It’s not one single piece of technology, but a powerful combination of tools working together in a split second. Think of it like a sophisticated security checkpoint at an airport, where each station inspects for different things.

It all starts with a constant, live feed of information. The entire system is built on streaming data. Instead of waiting to dump all your transaction data into a big database to analyze later, real-time monitoring inspects every event as it happens. It's like having a security expert watch a river of transactions flow by, examining every single one the moment it appears—be it a login attempt, a purchase, or a password change.

This live-stream approach is a game-changer for catching the kind of rapid-fire fraud attacks where criminals slam your system with thousands of stolen cards in just a few minutes. By analyzing the stream, the system spots the overall pattern of the attack instantly, not just a bunch of disconnected failed payments. It’s the difference between catching one shoplifter and shutting down an organized ring hitting multiple stores at once.

The diagram below shows exactly what’s at stake. Any delay between the transaction and the analysis—what we call the "velocity gap"—is a window of opportunity for fraud that leads directly to more chargebacks.

As you can see, every moment you’re not monitoring in real-time is a moment you’re exposed to risk.

The Role of Rules Engines

The first line of defense analyzing this data stream is usually a rules engine. You can think of a rules engine as your digital bouncer. It works off a very clear set of "if-then" instructions you give it, looking for obvious red flags.

These rules are your first filter, designed to catch the low-hanging fruit of the fraud world. For instance, a merchant might set up rules like:

- IF a transaction comes from a high-risk country AND the shipping address is different from the billing address, THEN flag it for manual review.

- IF more than 3 transactions are attempted from the same IP address in less than a minute, THEN block that IP.

- IF an order is over $1,000 and it’s a customer’s very first purchase, THEN trigger an extra verification step.

This rigid, logical approach is fantastic for stopping basic, unsophisticated attacks. The downside? Rules engines can be a bit of a blunt instrument. They can sometimes block legitimate customers or be easily outsmarted by clever fraudsters who know how to stay just inside the lines.

The Power of Machine Learning and AI

This is where machine learning (ML) and artificial intelligence (AI) come into play, acting as your team of expert fraud detectives. While a rules engine looks for known threats you’ve explicitly defined, an AI model does something far more sophisticated: it learns the unique rhythm of your business. It builds a deep understanding of what "normal" looks like for your store, from average order values to the typical times of day your real customers shop.

When a new transaction appears, the AI compares it against this learned behavior in milliseconds. It’s searching for subtle inconsistencies that a fixed set of rules would completely miss. For example, an AI can tell the difference between a stolen card making a weird purchase and a loyal customer who just happens to be on vacation buying something from a new device. It sees that other behavioral patterns are consistent and lets the good order through, preventing a false decline.

A rules engine is like a checklist, but an AI model is like an experienced investigator with gut instinct. It understands context, connecting thousands of data points to see the bigger picture and make a more accurate judgment call.

Let's look at how these two approaches stack up.

Traditional Rules-Based vs Modern AI-Powered Monitoring

| Feature | Traditional Rules-Based System | AI-Powered Real-Time Monitoring |

|---|---|---|

| Logic | Fixed "if-then" statements set manually. | Dynamic learning based on historical and real-time data. |

| Adaptability | Slow to adapt; requires manual updates for new fraud tactics. | Self-adapting; automatically identifies new and emerging patterns. |

| Accuracy | Prone to high false positives (blocking good customers). | Significantly lower false positives by understanding user behavior. |

| Detection | Catches known, pre-defined fraud patterns. | Uncovers subtle, unknown, and complex fraud schemes. |

| Maintenance | Requires constant manual tuning and rule management. | Largely self-maintaining and continuously improves over time. |

| Scalability | Becomes complex and difficult to manage as rules multiply. | Scales effortlessly with transaction volume and data complexity. |

This evolution from static rules to intelligent learning is what makes modern real-time transaction monitoring so effective. The biggest complaint with older systems has always been the high rate of false positives—good sales you lose because your system was too cautious. AI tackles this problem head-on.

While 61% of firms are now prioritizing real-time monitoring, a whopping 55% say that managing false positives is their number one headache. AI offers a solution by analyzing behavior with context, not just following a script. This leads to far greater accuracy, happier customers, and a lot less manual work for your team. You can learn more about how businesses are choosing the right AML tools for 2026 to stay ahead of these challenges.

Getting Your Monitoring System Hooked Up

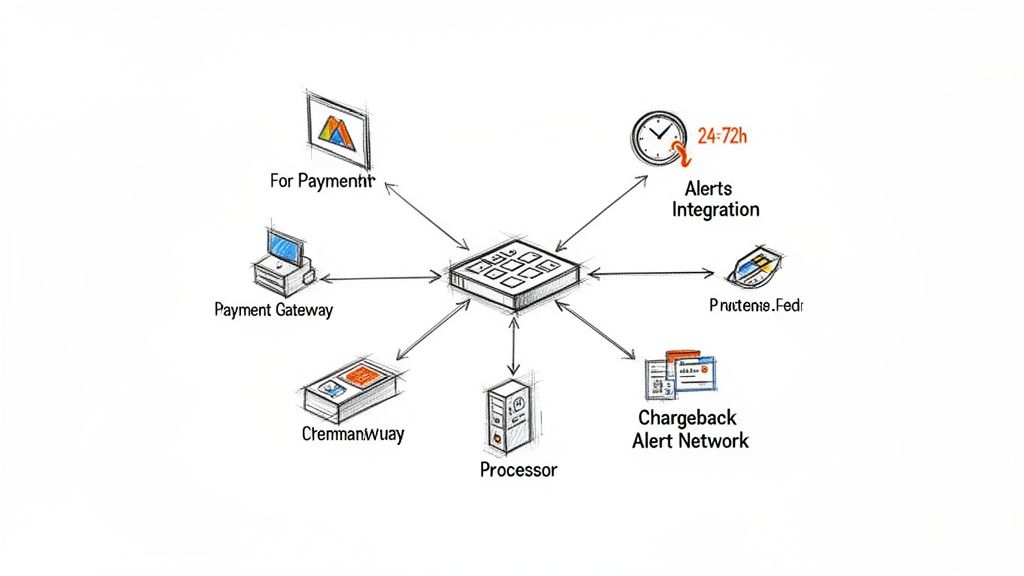

Knowing how the tech works is one thing, but actually plugging it into your business is what really matters. Thankfully, most modern monitoring platforms are built to be plug-and-play, acting as a kind of universal adapter between your payment gateway and the alert networks that stop chargebacks in their tracks.

Think of the monitoring platform as the central nervous system for your payments. On one end, you connect your payment processor—Stripe, PayPal, Shopify Payments, you name it. This gives the system eyes on every single transaction flowing through your checkout. It's like putting a high-tech security camera on your digital front door.

On the other end, you connect to the dispute alert networks. These are your direct lines to the card brands, giving you a critical heads-up before a customer complaint turns into a full-blown, damaging chargeback.

Connecting Your Payment Processor

First things first: you need to give your monitoring system access to your transaction data. This usually happens through a secure API connection that you can set up in just a few minutes. For this to really work, you need solid integration with the platforms you already use, like a Stripe integration.

Once it’s linked, the system sees everything—every purchase attempt, every decline, every approval—as it happens. This constant stream of data is the lifeblood of the whole process, feeding the rules engines and machine learning models the raw information they need to spot trouble. For Shopify merchants, this kind of integration can be a lifesaver for sorting out frustrating issues like sudden payment holds. We've got a whole guide on how to https://disputely.com/shopify-hold if that's a problem you've faced.

This direct connection leaves no room for blind spots. Every bit of data, from the card BIN down to the customer’s IP address, is fed into the analysis engine for an instant risk assessment.

Integrating with Chargeback Alert Networks

Connecting your payment gateway is only half the battle. The real magic happens when you integrate with chargeback alert networks. This is what transforms your monitoring system from a passive observer into an active defender of your revenue.

These networks are essentially collaborative programs set up by the card brands to help everyone reduce chargebacks. The big ones you need to know are:

- Visa RDR (Rapid Dispute Resolution): This system can automatically resolve disputes based on rules you set up beforehand. For instance, you could create a rule to automatically refund any flagged transaction under $25, no questions asked.

- Mastercard CDRN (Consumer Dispute Resolution Network): Run by Verifi, this network pings you with an alert the moment a Mastercard holder disputes a charge, giving you a window to handle it directly.

- Ethoca Alerts: Owned by Mastercard, Ethoca does something similar but taps into a massive network of card-issuing banks, covering a huge range of card types.

Tying into these networks is like getting a text from a customer's bank the instant they raise an eyebrow over a charge. This gives you a crucial 24-72 hour window to issue a refund and stop the problem from becoming an official chargeback, which is absolutely vital for protecting your merchant account and keeping your dispute ratio low.

Your Practical Integration Checklist

Getting this set up is a high-impact project that starts protecting your bottom line almost immediately. Here’s a straightforward checklist to get you through it:

- Choose a Central Platform: Pick a monitoring solution that already has pre-built connections for both your payment processor and the major alert networks. This will save you from a world of custom development headaches.

- Connect Your Payment Gateway: Just follow the platform’s instructions. It usually involves authorizing the connection to your Stripe, PayPal, or other processor account with a secure API key.

- Enroll in Alert Networks: Your monitoring provider will almost always handle the enrollment paperwork with Visa, Mastercard, and Ethoca for you.

- Configure Your Refund Rules: Decide on the specific conditions for automatic refunds. You can get pretty granular here, setting rules based on the transaction amount, the type of product, or even the reason for the dispute.

- Go Live and Monitor Results: Once it's all switched on, the system will start watching transactions and handling alerts on its own. All you have to do is keep an eye on your dashboard to see your chargeback rate drop and watch the ROI roll in.

So, you've invested in a real-time transaction monitoring system. That’s a great first step, but how do you really know if it's paying off? Proving its worth goes way beyond simply counting blocked transactions. To get the full picture, you need to dig into the numbers that directly affect your bottom line and your standing with payment processors.

Tracking the right metrics is what separates guessing from knowing. It helps you shift the conversation from a vague "we're stopping fraud" to a powerful "we've boosted our profit margin by X percent" by showing the real-world financial impact of your efforts.

The Metrics That Matter

If you're going to understand the true value of your monitoring system, you can't afford to fly blind. You have to track the right data. Start with these crucial indicators that reveal the health of your payment processing and show just how well your fraud prevention strategy is working.

Think of these as the non-negotiable stats for your dashboard:

Chargeback Ratio: This is the big one, the metric that payment processors watch like a hawk. It's simply the number of chargebacks you get in a month divided by your total number of transactions for that same month.

False Positive Rate: How many good, legitimate transactions are you accidentally declining? A high rate here is a serious problem—it means you're turning away real customers and leaving money on the table.

Alert-to-Prevention Rate: When you get an alert from a network like Ethoca or Visa's RDR, how often are you successfully stopping the chargeback by issuing a refund in time? This number shows how effective your response is.

Why the 0.9% Rule is Crucial Across the industry, a chargeback ratio of 0.9% is the magic number you never want to cross. If you go over this threshold, you’ll find yourself in costly monitoring programs run by Visa or Mastercard. This can lead to massive fines and, in worst-case scenarios, even getting your merchant account shut down. A good system keeps you well clear of that danger zone.

To get a clearer view of what you should be tracking, here’s a breakdown of the most important KPIs.

Essential Metrics for Monitoring Success

This table outlines the key performance indicators (KPIs) every merchant should have on their radar. Tracking these will give you a clear, data-backed view of how your transaction monitoring and chargeback prevention efforts are performing.

| Metric | What It Measures | Industry Benchmark/Goal |

|---|---|---|

| Chargeback Ratio | The percentage of transactions that result in a chargeback. | Keep it well below 0.9% to avoid penalties. Aim for <0.5%. |

| False Positive Rate | The percentage of legitimate transactions incorrectly declined as fraud. | Aim for <1-2%. A high rate hurts revenue and customer experience. |

| Alert-to-Prevention Rate | The success rate of resolving chargeback alerts before they become disputes. | Strive for 95% or higher. This shows you're making the most of the alerts. |

| Manual Review Rate | The percentage of transactions that require human review. | Goal is to minimize this. A low rate means your automated rules are effective. |

| Fraud Block Rate | The percentage of all incoming transactions blocked due to suspected fraud. | Varies by industry, but should align with known fraud attempt rates. |

Keeping a close eye on these numbers doesn't just tell you if your system is working—it gives you the insights you need to fine-tune your rules and maximize your profitability.

Calculating Your System's True ROI

The return on investment (ROI) from a top-notch monitoring system isn't just about the fraudulent orders you block. The real value comes from a combination of direct savings, operational efficiencies, and penalties you avoid.

To figure out your true ROI, the math is pretty straightforward: add up all your savings, then subtract what you paid for the solution.

Total ROI = (Chargeback Fees Saved + Manual Review Costs Saved + Avoided Processor Fines) – Cost of Monitoring Solution

Let's break that down piece by piece:

Chargeback Fees Saved: This is your most obvious win. Just multiply the number of chargebacks your system prevented by the average fee your processor hits you with for each dispute (this is usually somewhere between $15 and $100).

Manual Review Costs Saved: How many hours did your team used to burn manually checking flagged orders? Figure that out, multiply it by their hourly wage, and you’ll see exactly how much you're saving in labor.

Avoided Processor Fines: This one can be a little harder to pin down, but it’s huge. If your monitoring system keeps you out of a card network’s high-risk program, you're dodging thousands of dollars in monthly fines. That’s a massive saving.

By tracking these specific numbers, you can clearly show the financial upside of real-time monitoring. This data gives you the power to make smarter decisions, justify the cost, and prove that being proactive about fraud is one of the most profitable moves your business can make.

To see how different pricing models might impact your own ROI, you can explore the various plans available for alert-based systems.

Why Proactive Monitoring Is A Business Necessity

In the world of online business, the line between a defensive tool and a core operational function has completely dissolved. Real-time transaction monitoring isn't some niche security add-on anymore; it's a fundamental part of staying in business and growing. The sheer volume and velocity of online payments mean that trying to analyze problems after they’ve happened is a surefire way to fall behind.

This shift is a direct result of the explosion in digital sales and the increasingly sophisticated threats that come with it. Simply put, proactive and instant monitoring is your best defense for protecting your merchant accounts. It's what keeps your relationships with payment processors healthy and your dispute rates low, building a stable foundation for growth.

Navigating A Landscape of Growth and Risk

The digital payments ecosystem is expanding at a dizzying pace, which brings a ton of opportunity—and just as much risk. With all this growth, you can bet that regulators and the major card networks are paying closer attention. They now expect every business to have solid systems in place to combat financial crime.

This isn't a friendly suggestion; it’s the new cost of doing business. Meeting standards like PCI DSS compliance makes proactive monitoring an absolute necessity for protecting sensitive payment data and earning customer trust. If you can't keep up, you're looking at steep fines, the potential loss of your payment processing, and a hit to your reputation that can be incredibly hard to bounce back from.

In modern commerce, waiting for a problem to happen is no longer a viable strategy. Proactive monitoring moves your business from a constant state of defense to a position of control, transforming security from a cost center into a powerful business enabler.

This intense environment is why we're seeing huge investments in protective tech. The global transaction monitoring market is expected to jump from USD 6.26 billion in 2025 to USD 25.48 billion by 2035. That’s not just random growth; it’s a direct response to the overwhelming number of flagged transactions happening worldwide, highlighting the urgent need for automated, real-time tools. You can dig into the full research on these fintech market projections if you want to see the numbers for yourself.

Gaining A Competitive Advantage

When it comes down to it, the most compelling reason to get on board with real-time monitoring is the competitive edge it gives you. This is about more than just stopping fraud and chargebacks; it fundamentally changes how you operate.

Imagine not having to operate in constant fear of high-risk orders. You can start confidently accepting more legitimate transactions that you might have otherwise declined. A smart system can tell the difference between a genuinely fraudulent attempt and a good customer who just happens to have an unusual buying pattern. This means fewer false declines and more money in your pocket.

By using this technology, you get more than just financial stability and brand protection. You unlock the full potential of your sales channels. Real-time monitoring isn't just about blocking bad transactions—it's about safely letting every single good one through.

Frequently Asked Questions

When you're looking into real-time transaction monitoring, it's natural to have a few questions. Let's break down some of the most common ones we hear from merchants.

What's The Real Difference Between Real-Time And Batch Monitoring?

The main difference is timing, and in the world of fraud, timing is everything.

Real-time transaction monitoring is like having a security guard standing right at your checkout. It scrutinizes every single transaction the moment it happens, giving a thumbs-up or thumbs-down in milliseconds, before the payment is finalized.

Batch monitoring, on the other hand, is like reviewing security footage at the end of the day. It gathers up all the transactions from a set period (an hour, a day) and then looks for problems. By the time it finds something suspicious, the payment has already cleared, and the fraudster is long gone. That delay just doesn't cut it against today's lightning-fast fraud attacks.

How Long Does It Actually Take To Get Set Up?

This is usually much faster than people expect. Most modern monitoring platforms are built to be plug-and-play, especially with the payment processors you’re already using. For most merchants, getting up and running is a simple, three-step process:

- Connect Your Payment Gateway: This is typically done with a secure API connection and often takes less than 10 minutes.

- Get Enrolled in Alert Networks: Your provider usually takes care of the paperwork to get you hooked into crucial networks like Visa RDR and Ethoca.

- Set Your Basic Rules: You’ll start by telling the system how to handle certain flags—for example, you might want to automatically refund any alerted transaction under $30.

From start to finish, most businesses can be fully protected within a few days, not the weeks or months you might be dreading.

Modern platforms are designed to get you protected without needing a team of developers. The whole point is to connect directly to your existing payment stack with minimal fuss.

Will This End Up Blocking My Good Customers?

This is probably the biggest fear merchants have, but a smart system actually does the opposite—it reduces false declines.

The key is that modern solutions don't rely on a clunky, rigid set of rules alone. They use machine learning and AI to see the bigger picture. A simple rule might block a good customer just because they're traveling. But an AI-powered model looks at dozens of other signals, recognizes the rest of their behavior as normal, and lets the purchase go through.

By analyzing the full context of every transaction, these systems have a much lower false positive rate. This means you stop more fraud without turning away real customers, which is a win for both your revenue and their experience.

What Should I Expect To Pay For A Service Like This?

Pricing has become a lot more merchant-friendly. Gone are the days of long, complicated contracts and hefty setup fees. Today, a popular model is pay-per-alert, where you only pay when the system successfully intercepts a chargeback alert for you.

This model makes a lot of sense because the provider only makes money when they save you money. It's a cost-effective approach that scales with your business—the cost is directly tied to the value it's delivering by preventing those expensive chargeback fees.

Ready to stop chargebacks before they happen? Disputely integrates directly with major alert networks to give you the power to refund disputed transactions before they hurt your business. Protect your merchant account and see your projected savings today.