Reason to Dispute a Charge: Why Customers Do It and How Merchants Respond

When a customer disputes a charge, it's usually because something went wrong with the transaction. They might see an unauthorized charge, spot a billing error, or receive a product that’s broken or not what they expected.

Instead of trying to sort it out with the merchant, they call their bank and ask for a forced reversal—what we know as a chargeback.

Why Customers Initiate Chargebacks

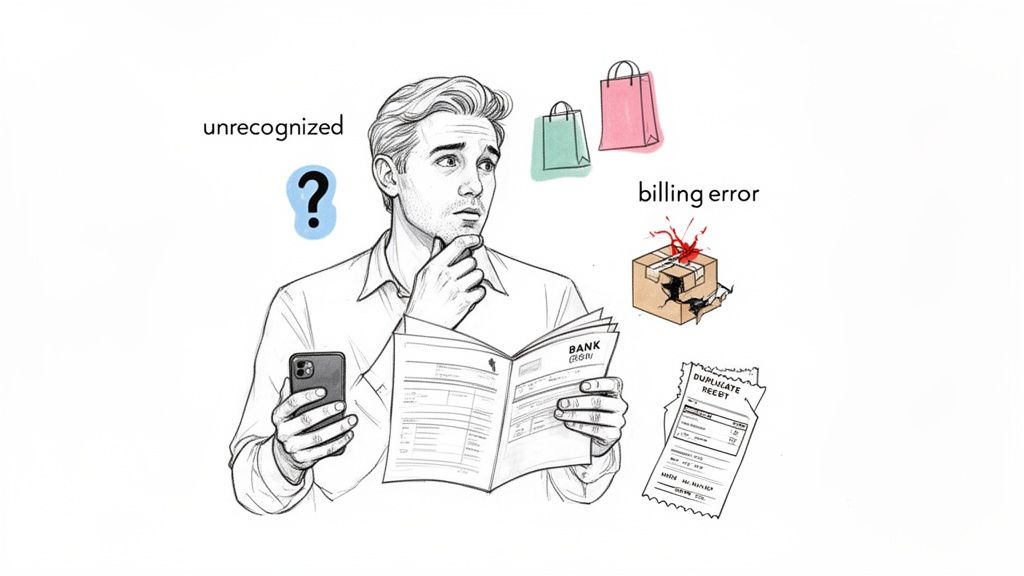

To get a handle on chargebacks, you first have to step into your customer's shoes. A dispute isn't always malicious. More often than not, it's a cry for help after a confusing or frustrating experience.

Think of it as a distress signal. When someone sees an unfamiliar company name on their bank statement or gets charged for a subscription they were sure they’d canceled, their first instinct is to protect their money.

This reaction is usually triggered by a handful of common problems:

- Confusion and Lack of Clarity: Unclear billing descriptors are a massive culprit. A charge from "SP *WEBSERVICES" instead of "Your Awesome Gym" looks suspicious and gets flagged as fraud.

- Product or Service Dissatisfaction: If a product shows up broken, turns out to be a fake, or just doesn't live up to the hype, the customer feels ripped off and wants their money back.

- Billing and Subscription Errors: Getting charged twice, for the wrong amount, or after a cancellation is a surefire way to trigger a dispute. These are clear, undeniable mistakes.

- Perceived Lack of Support: When a customer can't find your contact info or gets stuck in an endless email loop waiting for a refund, they’ll turn to their bank. It’s a fast, one-click solution for them.

The impulse to dispute a charge often begins when the customer feels unheard or powerless. The chargeback process gives them a direct path to a resolution, bypassing what they might perceive as a difficult or unresponsive merchant.

Understanding what makes customers unhappy is the first step. Addressing issues linked to the 7 Examples of Bad Customer Service can make a huge difference in cutting down disputes.

Once you truly grasp the "why" behind their actions, you can build smarter, more empathetic strategies to prevent chargebacks before they even happen.

Top Reasons Customers Dispute Charges

To help you diagnose potential issues in your own business, here’s a quick summary of common chargeback triggers from the customer's point of view.

| Dispute Category | What the Customer Says | Potential Merchant Cause |

|---|---|---|

| True Fraud | "I didn't make this purchase." | A stolen card was used; no fault of the legitimate cardholder. |

| Unauthorized Charge | "I don't recognize this charge." | Unclear billing descriptor or a forgotten recurring payment. |

| Billing Error | "I was charged the wrong amount/twice." | A system glitch, human error, or un-canceled subscription. |

| Product Not as Described | "This isn't what I ordered." | Damaged goods, wrong item shipped, or misleading product photos. |

| Services Not Rendered | "I never received the service I paid for." | Delivery delays, service outages, or failure to fulfill the promise. |

| Cancellation Issues | "I canceled, but you're still billing me." | Complicated cancellation process or a delay in processing it. |

Looking at this table, you can see how a simple misunderstanding can quickly escalate. The key is to close the gaps in communication and process before your customer feels like calling their bank is their only option.

What's Behind Most Customer Disputes?

Let's get real about why customers dispute charges. When a customer flags a transaction, their bank slaps a formal "reason code" on it. But for you, the merchant, those codes are just jargon. They don't tell you the real story.

To actually get ahead of chargebacks, you need to understand the human reason behind the code. Think of it like this: the reason code is the what, but the customer's experience is the why. Once you understand the why, you can start fixing the root problems in your business.

Fraud and Unauthorized Charges

This is the one everyone knows: a charge shows up on a statement that the cardholder flat-out didn't make. It’s straight-up theft, and it's a huge headache for both the customer and the merchant.

This usually plays out in one of two ways:

- True Fraud: The classic scenario. A thief gets ahold of stolen card details and goes on a shopping spree. The actual cardholder is a victim here, and they are completely justified in disputing the charge.

- Family Fraud: This one's a bit more awkward. It’s when someone in the cardholder's own family—often a kid who has access to a saved card on an iPad—makes a purchase without permission. It might not be malicious, but from the cardholder's point of view, it’s still an unauthorized transaction.

While you can't stop all criminal fraud, you absolutely need strong defenses. Things like Address Verification Service (AVS) and CVV checks are the bare minimum. They’re your digital bouncers, checking IDs at the door.

Billing and Subscription Errors

Mistakes happen. We get it. But when that mistake involves someone's bank account, it erodes trust fast. Billing errors are a massive, and often preventable, source of disputes because the customer feels like they've been wronged.

Here are the usual suspects:

- Duplicate Charges: The customer bought one thing but was charged twice.

- Incorrect Amount: The price they saw at checkout isn't what they were actually charged.

- Recurring Billing Issues: This is a big one. They got charged for a subscription they thought they canceled, or a free trial rolled into a paid plan without a clear warning.

A huge number of subscription chargebacks happen simply because the customer was surprised. If that recurring charge hits their account unexpectedly, they’re far more likely to call their bank than your support team.

These disputes are almost always a communication problem. A simple, automated email reminding a customer that their subscription is about to renew can save you a world of hurt. It's all about transparency.

Product and Service Issues

This category is all about mismatched expectations. The customer paid for something, but what they got wasn't what they were promised. For any e-commerce brand, this is where a lot of friction happens.

Think about these common scenarios:

- Product Not as Described: The sweater they ordered was supposed to be navy blue, but it showed up royal blue. Or worse, it was advertised as 100% cotton but feels like cheap polyester.

- Damaged or Defective Goods: The item arrived with a crack in it, or it just stopped working after a week.

- Services Not Rendered or Canceled: The customer paid for a service they never received or put down a deposit for an appointment that was canceled.

- Product Never Received: This is the ultimate delivery failure. They paid, waited, and the package simply never arrived.

Fixing these problems comes down to being buttoned up on the operational side of things. It starts with writing accurate product descriptions and having good quality control. It ends with using shipping partners you can actually count on. Every single step in your fulfillment process is a chance for things to go wrong and turn into a costly dispute.

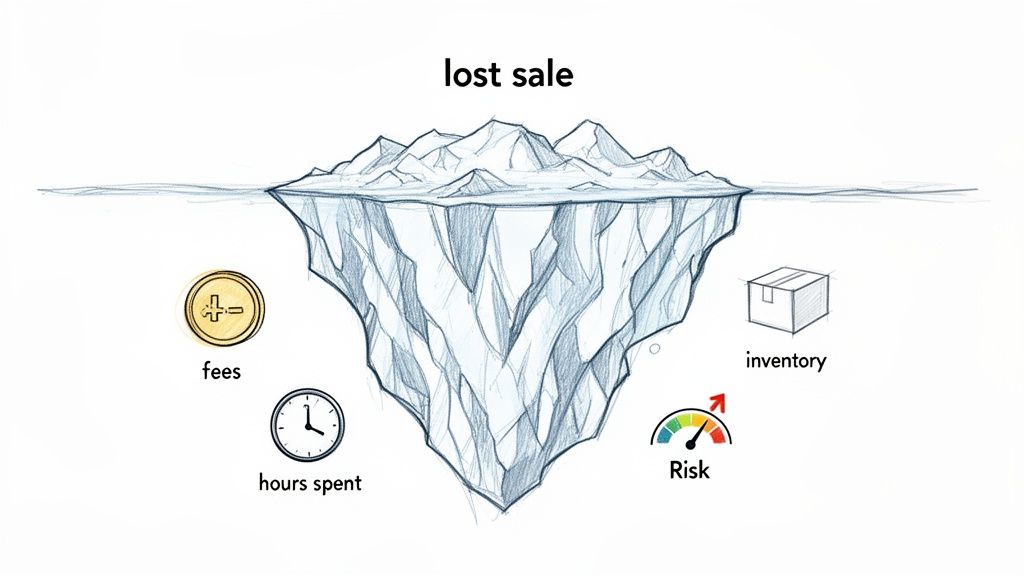

The True Cost of a Single Chargeback

Most business owners think a chargeback is just a lost sale. A customer disputes a $50 transaction, so you lose $50. Simple, right? Not even close. That initial lost revenue is just the tip of the iceberg; the real damage is what's lurking below the surface.

When you really dig into the numbers, the true financial hit from a single dispute is staggering. In fact, research shows the total cost can be up to 250% of the original transaction amount. A $50 sale doesn't just evaporate—it multiplies into a much larger loss.

This happens because one dispute sets off a chain reaction of costs that go way beyond the price tag of the item. Once you understand these hidden expenses, it becomes crystal clear why preventing even one chargeback is so incredibly important.

The Financial Multiplier Effect

The moment a customer files a dispute, your payment processor slaps you with a non-refundable chargeback fee. This fee, usually somewhere between $20 and $100, is yours to pay whether you win or lose the fight. All of a sudden, that $50 loss has ballooned to $70 or more.

But the bleeding doesn't stop there. Think about all the other direct and indirect costs that start piling up:

- Lost Inventory: The product you shipped is gone for good. Unlike a normal return where you can restock the item, a chargeback often means the customer keeps the product and gets their money back.

- Shipping and Fulfillment Costs: The money you spent on boxes, packing tape, and postage? Kiss it goodbye.

- Operational Hours: Your team has to drop what they're doing to dig up evidence, write compelling rebuttal letters, and navigate the dispute process. Every hour they spend fighting a chargeback is an hour they can't spend growing the business.

- Customer Acquisition Costs (CAC): All the marketing and ad dollars you spent to get that customer in the door are now completely wasted. You can bet you’ve lost that customer forever, too.

A chargeback isn’t just a transaction reversal; it's a punitive process designed to penalize merchants. Every dispute is a direct hit to your profit margin and operational efficiency.

Long-Term Account Health Risks

Perhaps the most dangerous cost of all is the damage done to your relationship with payment processors. Every single chargeback you receive, no matter the reason, chips away at your reputation by increasing your chargeback-to-transaction ratio. This is the single most important metric card networks like Visa and Mastercard use to decide if you're a risky business to work with.

If your ratio creeps above their threshold—typically around 0.9%—you’re in hot water. You can be forced into expensive monitoring programs that come with hefty monthly fines and a ton of scrutiny. If you can't get things under control, you risk having your merchant account terminated entirely. For an online business, that's the kiss of death.

It’s why preventing disputes is always, always more valuable than fighting them.

The Growing Problem of Friendly Fraud

While clear-cut cases of fraud and simple merchant mistakes are easy enough to understand, there's a much cloudier issue that's quickly becoming a major headache for online businesses: friendly fraud.

Also known as first-party misuse, friendly fraud is what happens when a customer disputes a charge that they or a family member actually made. It wasn't a stolen card; the transaction was real. The customer is simply using the chargeback system to get their money back, blurring the lines between a simple mistake and deliberate abuse.

And this isn't some minor annoyance. Industry data reveals that merchants label 45% of all their chargebacks as fraudulent. This figure is split almost evenly between classic third-party fraud (22%) and this tricky first-party misuse, or friendly fraud (23%). That makes friendly fraud one of the single biggest threats merchants are up against. You can dive deeper into the full report on chargeback trends to see just how this is playing out.

Why Does Friendly Fraud Happen?

The reasons a customer might file a friendly fraud chargeback can be complicated, ranging from genuine confusion to straight-up dishonesty. Getting a handle on these motivations is the first real step to protecting your revenue.

Here are the most common reasons it happens:

- Buyer's Remorse: The customer regrets their purchase but wants to avoid the hassle of a standard return, which might mean paying for shipping or a restocking fee. Filing a chargeback just seems easier.

- Billing Descriptor Confusion: They see a charge on their credit card statement with a company name they don't recognize. Instead of looking it up, they jump to the conclusion that it’s fraud and call their bank.

- Family Member Purchase: A spouse, partner, or child uses the saved card on file to buy something. The main cardholder later disputes the charge, either because they truly didn't know or because they don't want to pay for it.

- Intentional Misuse: In the worst cases, the customer knows perfectly well that the charge is valid. They dispute it anyway, hoping to get the product or service for free. This is just digital shoplifting.

Friendly fraud is so damaging because, from the merchant's perspective, everything looks perfectly legitimate. You received a valid authorization, you shipped the product, and you held up your end of the deal. Then, weeks later, you get hit with a chargeback penalty.

The Impact on Your Business

Every single friendly fraud case takes a direct bite out of your bottom line. You don't just lose the revenue from that sale—you're also out the cost of the product you shipped and get slapped with a non-refundable chargeback fee from your processor.

Even worse, each one of these disputes pushes your chargeback ratio higher. This nudges you closer to the "high-risk" category that card networks like Visa and Mastercard are always watching. It can put your entire ability to process payments in jeopardy, all because a customer decided your return policy was optional. It’s no wonder that fighting this has become such a critical priority for businesses.

How to Stop Chargebacks Before They Happen

Playing defense against chargebacks is a losing game. By the time a dispute hits your account, you’ve already lost the sale, you're on the hook for a fee, and your chargeback ratio has taken a hit. But what if you could get ahead of it? What if you could solve the customer's problem before it ever becomes a formal chargeback?

That's not just a hypothetical. There's a critical window of opportunity—usually between 24 to 72 hours—after a customer calls their bank to complain but before the bank officially files the chargeback. Think of this as a "pre-dispute" phase. It’s like the bank sending up a warning flare, giving you a small window to step in and make things right.

Intercepting Disputes with Chargeback Alerts

This is exactly where chargeback alert services shine. These platforms plug directly into the major card networks, like Visa and Mastercard, and listen for those early warning signals. So, instead of being ambushed by a chargeback notification weeks down the line, you get an alert in real-time, the moment your customer starts the dispute process.

This alert is your chance to act. The best move is almost always the most direct one: issue a full and immediate refund. When you refund the customer within this alert window, you resolve their core complaint. The bank sees the issue is settled and stops the dispute from ever becoming an official, damaging chargeback.

This simple, proactive step completely flips the script. You transform a potential financial and logistical nightmare into a simple customer service resolution. This strategy is absolutely essential if you're worried about your processor suddenly freezing your funds. To understand just how serious that can be, you can learn more about dealing with a Shopify Payments hold and see why prevention is everything.

A proactive refund isn't an admission of guilt—it's a smart, strategic business decision. You’re choosing to sacrifice a single sale to protect your entire merchant account from fees, penalties, and long-term damage.

Why Prevention Is Always Better Than a Cure

By catching a dispute early, you sidestep all the downstream pain. You don’t pay that hefty chargeback fee, your all-important chargeback ratio stays clean, and you maintain a healthy relationship with your payment processor.

This isn't just about good business hygiene; it's a critical defense against the kind of fraud that can sink a company's reputation. Bolstering your site's security is a foundational piece of this puzzle. Following established guidelines like these 8 Essential Website Security Best Practices for 2025 can help you filter out fraudulent orders from the start, dramatically reducing the odds of a dispute ever happening.

At the end of the day, a little prevention saves a ton of time, money, and the headache of fighting battles you're unlikely to win.

Building Your Proactive Prevention Strategy

If you're only fighting chargebacks after they happen, you're always going to be one step behind. The real key to protecting your revenue is to shift from a reactive mindset to a proactive one. Think of it less like putting out fires and more like fireproofing your entire business. The goal is to build a system that stops disputes before they even have a chance to start.

This doesn't have to be complicated. In fact, some of the smallest adjustments can have a massive impact.

Take your billing descriptors, for instance. If a customer sees a charge from "Your Brand Name," they know exactly what it is. But a cryptic charge like "SP*WEBSERVICESINC" screams fraud, making it a top reason to dispute a charge. It's a simple fix with a huge payoff.

Clear, consistent communication is another non-negotiable. Be upfront about shipping times. Send tracking information the moment a package goes out. Make sure your return policy is easy to find and even easier to use. A little transparency goes a long way in calming frustrated customers before they pick up the phone to call their bank.

Foundational Security and Support

Beyond clear communication, you need the right tools in place to weed out obvious fraud from the get-go. These are your first line of defense against someone using a stolen credit card, which is a guaranteed chargeback every single time.

- Address Verification Service (AVS): This is a basic but powerful tool. It simply checks that the billing address the customer enters matches what the credit card company has on file.

- Card Verification Value (CVV): Always require the three- or four-digit security code from the card. This proves the person making the purchase actually has the physical card in their hand.

Just as important is making sure your customers can actually reach you. If a customer can solve a problem with a quick phone call or email, they won't need to file a dispute. Hiding your contact info is one of the fastest ways to invite more chargebacks. If you want to get serious about this, a quarterly audit of your chargeback prevention efforts can help you pinpoint exactly where your weaknesses are.

The process of heading off a dispute is surprisingly simple when you have the right alerts in place.

This flow is your best friend. An alert gives you a chance to review the problem and issue a refund, stopping the dispute dead in its tracks. Each of these strategies—clear descriptors, open communication, and solid security—works together to build a powerful defense system that protects your bottom line and keeps your merchant account in good standing.

Frequently Asked Questions About Chargebacks

Jumping into the world of chargebacks can feel like learning a new language. Let's clear up some of the most common questions merchants ask so you can handle disputes with confidence.

What Is The Difference Between A Chargeback And A Refund?

Think of a refund as a friendly handshake. It’s a direct agreement between you and your customer to return their money for a purchase—a normal part of running a business.

A chargeback, on the other hand, is a forced reversal of a transaction that gets the banks involved. The customer goes to their bank, which then pulls the money from your account, completely bypassing you. This process comes with extra fees and hurts your reputation with payment processors. Offering a refund is always the better way to go; it solves the customer's problem without damaging your business.

How Long Do I Have To Respond To A Chargeback?

Once a formal chargeback is filed, you generally have 20-45 days to build your case and submit all your evidence. But the real magic happens in a much shorter window.

The most important timeframe is the 24–72 hour alert window. Chargeback alert networks give you this tiny heads-up before a dispute becomes an official chargeback. Acting fast in this period lets you issue a simple refund and stop the chargeback from ever hitting your record. It's the smartest move you can make.

Is It Possible To Prevent All Chargebacks?

Getting your chargeback rate to absolute zero is a tough goal, but you can definitely prevent the vast majority of them. Most disputes are completely avoidable and stem from simple misunderstandings or errors.

The key is a triple-threat approach: transparent business policies, amazing customer service, and a top-notch chargeback alert system. When a dispute is unavoidable, you still have options. Check out our guide on effective chargeback representment strategies to learn how to fight and win.

Stop letting preventable disputes eat into your profits. Disputely connects to your payment processor in just a few minutes, catching chargebacks before they do damage. We help you automatically resolve issues with refunds and keep your merchant account safe around the clock. See how much you could save and start protecting your business today at https://www.disputely.com.