Win More Chargebacks With Our Rebuttal Letter Template

When you're fighting a chargeback, your rebuttal letter is your single most important piece of ammunition. Think of a solid template not as a fill-in-the-blank form, but as a strategic framework that guides you in presenting your evidence clearly, professionally, and persuasively. Using a proven structure ensures you hit all the crucial points—from transaction details to a compelling narrative—which can dramatically swing a dispute in your favor.

Your Best Defense Against Rising Chargebacks

Chargebacks aren't just an annoying part of doing business; they're a direct and growing threat to your bottom line. What looks like a simple reversed sale on the surface quickly snowballs into a much larger financial hit. Each dispute has a hidden price tag that goes far beyond the original purchase amount.

The True Cost of a Single Dispute

Let's break down the real financial damage. When a chargeback is filed, you instantly lose the revenue from that sale. But the bleeding doesn't stop there. You're also out the non-refundable processing fees, you get hit with a separate chargeback penalty from your bank (typically $20 to $100 per incident), and you’ve already lost the cost of the goods and any shipping expenses.

On top of that, there's the operational cost. Your team has to drop what they're doing to dig up evidence, craft a response, and track the case. Those hours add up fast, turning one seemingly small dispute into a significant expense.

Why a Strategic Rebuttal Is Non-Negotiable

Simply ignoring chargebacks and writing them off as a cost of doing business is a losing game. The numbers are frankly intimidating. Chargeback volumes are projected to jump from 265 million cases in 2022 to an estimated 337 million by 2025. That's a massive 27% increase, driven largely by the explosion of card-not-present (CNP) sales online.

With the average chargeback costing a merchant around $190 when you factor in everything, you can't afford to be passive. This is precisely where a strategic, template-driven approach becomes your most powerful weapon. A well-structured rebuttal letter turns a chaotic, time-consuming reaction into a streamlined, effective defense.

Key Takeaway: A standardized rebuttal process isn't just about winning one dispute. It’s about protecting the long-term health of your merchant account and your ability to process payments smoothly.

By having a proven framework ready to go, your team can immediately:

- Respond Faster: No more starting from scratch every single time. A template helps you move quickly and confidently, ensuring you never miss a tight submission deadline.

- Maintain Consistency: Every response is professional and complete. You'll present all the critical evidence every time, leaving no holes for a bank reviewer to poke in your case.

- Improve Win Rates: Evidence presented in a clear, logical format is simply easier for a busy bank analyst to understand. When your argument is easy to follow, your chances of winning go way up.

For a truly powerful defense, you can pair your rebuttal strategy with a chargeback alert system. These services give you a heads-up about a potential dispute before it officially hits your account. This early warning gives you a critical window to either issue a refund and dodge the chargeback entirely or get a head start on gathering your evidence. When you look into the pricing for chargeback management solutions, you'll see how this proactive combination of alerts and templates forms the bedrock of any modern, resilient chargeback strategy.

Breaking Down a Winning Rebuttal Letter

A successful rebuttal letter isn't about simply telling your side of the story; it’s about constructing a clear, evidence-backed argument that’s impossible for a bank reviewer to ignore. You have to put yourself in their shoes. They’re swamped, looking at dozens of these cases every day, and searching for the quickest, most obvious path to a resolution. Your job is to make their decision to side with you an easy one.

This means your letter needs to be professional, factual, and surgically precise. Every single sentence should have a purpose. It should guide the reviewer through the transaction, systematically dismantle the cardholder's claim, and prove beyond a doubt that the charge was legitimate. Before you even start writing, it helps to understand the core principles of how to respond to a demand letter, because many of the same concepts about clarity and evidence apply directly here.

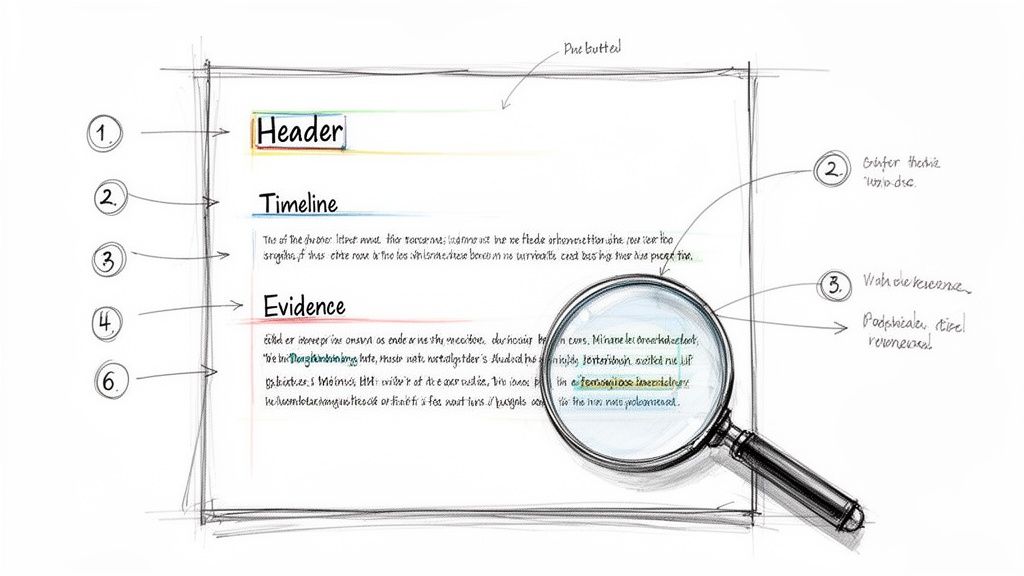

Key Elements of a Winning Rebuttal Letter

Before we dive into the narrative, let's look at the must-have components. Think of this table as your pre-flight checklist. Missing any of these pieces can seriously weaken your case before the reviewer even gets to your core argument.

| Component | Purpose | What to Include |

|---|---|---|

| Professional Header | Provides immediate context and all necessary identifiers. | Business name, address, case number, transaction date & amount, last 4 digits of the card, and cardholder's name. |

| Clear Opening Statement | Directly addresses and refutes the chargeback reason code. | A sentence stating you are disputing the chargeback and referencing the specific reason code (e.g., "Product Not Received"). |

| Chronological Timeline | Builds a logical, easy-to-follow narrative of the transaction. | Key events like order date, IP address, AVS/CVV results, shipping date, tracking number, and delivery confirmation. |

| Compelling Evidence | Provides the factual proof needed to invalidate the cardholder's claim. | All supporting documents, such as receipts, tracking info, delivery photos, customer communications, and terms of service. |

| Concise Summary | Briefly recaps your argument and requests a specific outcome. | A closing statement reiterating that you've proven the charge is valid and asking for the chargeback to be reversed. |

Getting these elements right sets a professional tone and makes it simple for the bank to see you've done your homework.

Start with a Professional and Comprehensive Header

The very top of your letter is prime real estate. It's the first thing the reviewer sees, and it should immediately give them all the case details without making them hunt for anything. A messy or incomplete header signals disorganization and can get your case started on the wrong foot.

Your header must clearly lay out:

- Your Business Information: Full business name, address, and contact details.

- Case Identifiers: The chargeback case number is non-negotiable.

- Transaction Details: Include the transaction date, amount, and the last four digits of the credit card.

- Customer Information: The cardholder's name and any other relevant identifiers you have.

This simple block of information frames the dispute perfectly and shows the reviewer you’re organized and ready. It’s a small detail that communicates professionalism from the very first glance.

Craft a Compelling Narrative

Right after the header, your opening paragraph needs to get straight to the point. State clearly that you are disputing the chargeback and immediately call out the specific reason code provided. This shows the bank you understand exactly what claim you need to disprove.

For instance, if the reason code is for "Product Not Received," your opening line could be, "We are writing to contest this chargeback, filed under the reason 'Product Not Received.' As the attached evidence confirms, the item was successfully delivered to the cardholder's verified address on [Date]."

This direct approach sets a confident, no-nonsense tone. From there, build a brief, chronological timeline of the entire transaction. Use short sentences or bullet points to walk the reviewer through the customer's journey from start to finish:

- Order Placed: The customer placed an order on [Date] from IP address [IP Address], which geolocates to [City, State].

- Payment Authorized: The payment was successfully authorized with correct AVS and CVV matches.

- Product Shipped: The order was shipped via [Carrier] with tracking number [Tracking Number] on [Date].

- Delivery Confirmed: The package was delivered and signed for on [Date] at the customer’s verified address.

This narrative structure isn't just a story; it's a logical argument. You are building a chain of events, each supported by evidence, that systematically invalidates the cardholder’s claim.

Maintain a Factual and Unemotional Tone

It’s completely normal to feel frustrated, especially when you suspect friendly fraud. But letting that emotion seep into your rebuttal letter is a critical mistake. Any language that sounds accusatory, defensive, or overly emotional will only undermine your credibility.

Stick to the cold, hard facts. Let your evidence do the talking for you.

Instead of saying, "The customer is obviously lying about not receiving the package," state, "The attached delivery confirmation includes a GPS location stamp and signature, verifying the package was delivered to the correct address." The first is an opinion; the second is a verifiable fact.

A professional, detached tone signals that your case is built on proof, not passion. This approach makes it far easier for the reviewer to agree with your conclusion and rule in your favor.

Gathering the Right Evidence for Any Dispute

A well-written rebuttal letter is crucial, but it’s the evidence you attach that will make or break your case. Think of your letter as the story you’re telling the bank reviewer, and your evidence as the undeniable facts that back it up. Without solid proof, your words are just claims. The goal is to build an airtight case that leaves absolutely no room for doubt.

This matters now more than ever. The entire chargeback landscape is getting more complicated and expensive for merchants like us. Globally, chargeback losses are projected to jump from $33.79 billion in 2025 to a staggering $41.69 billion by 2028—that's a 23% spike. This is happening because of the explosion in online shopping and, unfortunately, an increase in post-purchase disputes. To stay on the right side of these numbers, you need to master your evidence game.

Match Your Evidence to the Dispute Reason

Not all evidence is created equal. Sending a delivery confirmation for a dispute claiming a product was defective is a waste of everyone's time and a guaranteed loss. You have to be strategic and tailor your evidence to directly refute the cardholder's specific claim, which is identified by the chargeback reason code.

Here's a quick breakdown of how to think about the most common dispute types:

- For "Fraudulent Transaction" or "Unauthorized Charge" claims: Your mission is to prove the real cardholder was involved. You need to connect that person to the purchase with every piece of data you have.

- For "Product Not Received" claims: This is straightforward. Your entire case hinges on proving you delivered the item to the correct address. The more detailed your proof, the better.

- For "Product Not as Described" or "Defective Merchandise" claims: These are trickier. You need to show the product matched its online description and photos, and that your store policies are clear and were accessible to the customer.

- For "Subscription Canceled" or "Recurring Billing" claims: Here, it’s all about proving the customer knew what they were signing up for. Show that they agreed to your terms and were clearly notified about the billing schedule.

My Pro Tip: Don't just dump your evidence into the system. Call it out directly in your rebuttal letter. For example, "As demonstrated in Exhibit A, the AVS check returned a full match, confirming the billing address was known to the cardholder." This small step guides the reviewer and connects the dots for them, making their job easier.

Your Essential Evidence Checklist

Building a strong case file is about layering different pieces of proof to paint a complete picture of the transaction. For most e-commerce businesses, especially if you're handling a decent volume of orders, this is the evidence that consistently gets the best results with issuing banks.

Transaction and Authorization Data

This is the technical foundation of your case. It proves the charge itself was valid.

- AVS (Address Verification System) and CVV Match Results: This is non-negotiable. A "full match" on both is one of the strongest indicators you have that the legitimate cardholder placed the order.

- IP Address Geolocation: Show that the IP address used for the purchase matches the cardholder’s billing city or state. It’s another powerful data point linking them to the transaction.

- Device and Browser Information: Details like a device ID or browser fingerprint can be incredibly helpful, especially if you can show it matches previous, undisputed orders from that same customer.

Order and Fulfillment Records

This evidence shows you held up your end of the deal by shipping the right product to the right place.

- Order Confirmation Emails and Invoices: Always include copies of the receipts you sent to the customer’s email.

- Shipping and Delivery Confirmation: This is your primary weapon against "Product Not Received" claims. The best proof includes a tracking number, the full delivery address, and, ideally, a signature or photo confirmation from the carrier. GPS data from the delivery scan is exceptionally persuasive.

- Proof of Prior Undisputed Transactions: Has this customer ordered before without issue? If they have a history of successful deliveries to the same address, point it out. It makes a new "fraud" claim look highly suspicious.

Customer Interaction and Terms

This set of evidence proves the customer was informed, understood your policies, and had a chance to engage with you.

- Customer Service Communications: Provide complete, unedited transcripts of any emails, live chats, or support tickets. If a customer never bothered to contact you for help before filing a chargeback, make sure you highlight that fact.

- Proof of Service/Download Logs: For digital goods or services, this is your gold standard. Show logs proving the customer accessed their account, used the service, or downloaded the product after the purchase.

- Terms of Service and Refund Policy: Don't just send the policy; send a screenshot from your checkout page showing the customer had to check a box to agree to your terms, complete with a timestamp.

When you systematically gather and present these items, you're no longer just sending a letter. You're submitting a comprehensive, evidence-backed case file that an analyst can't ignore.

Actionable Rebuttal Letter Templates You Can Use Today

Alright, enough with the theory. Let's get down to what actually wins disputes: a rock-solid rebuttal letter. This is where you move from just knowing the rules to actually playing the game. A great rebuttal letter template is more than a fill-in-the-blank form; it’s a framework that walks the bank’s reviewer through your evidence, making your side of the story impossible to ignore.

Below are three templates I’ve seen work time and time again for some of the most common—and infuriating—chargeback scenarios. These aren't just generic scripts. I've added notes to guide you on exactly what information to plug in and which pieces of evidence will land the hardest.

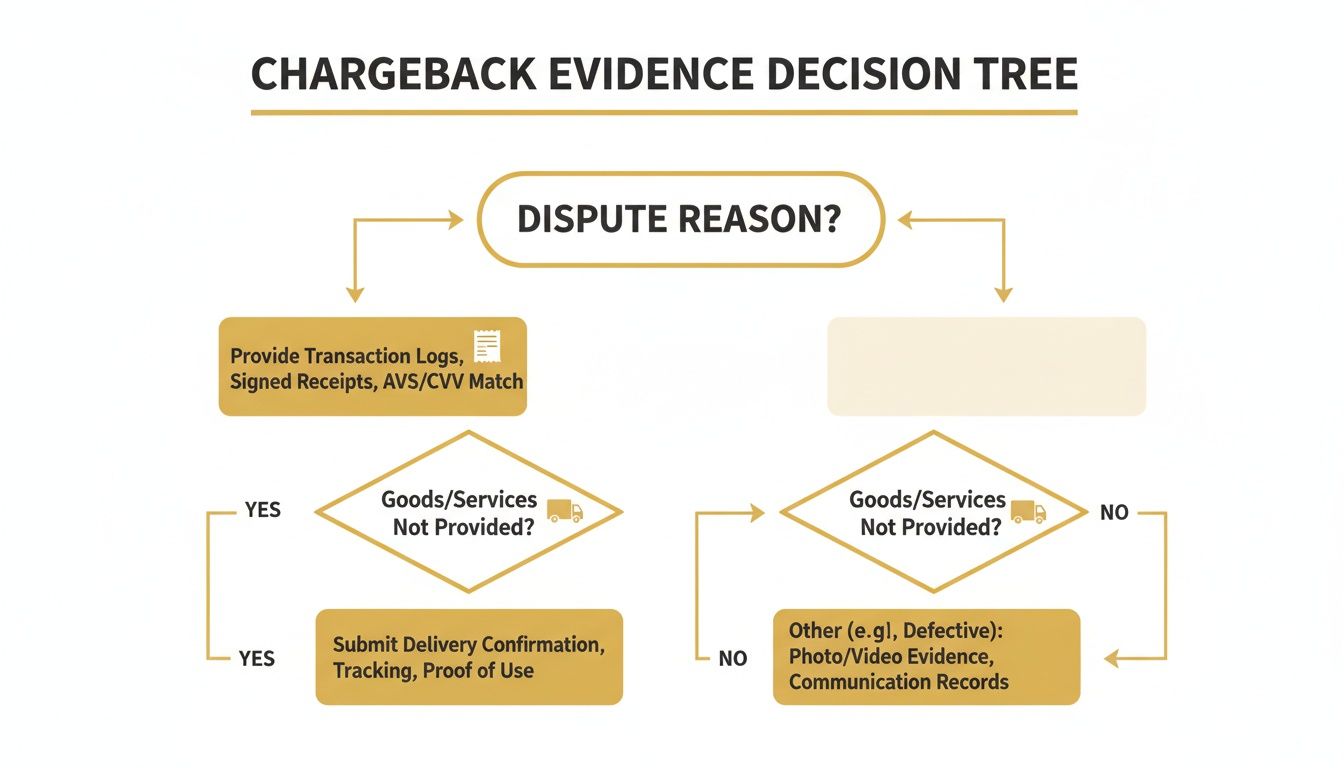

Before you even start writing, you have to know what proof you need. Choosing the right evidence is everything. This flowchart is a handy cheat sheet for matching your evidence to the dispute reason.

As the decision tree shows, it all starts with the reason code. Once you know why they're disputing the charge, you have a clear path forward for building your case.

Template 1: The "Card Not Present" Fraud Claim

This is the one we all love to hate. The customer claims they never made the purchase, and now the burden of proof is on you. Your single objective here is to prove the real cardholder was behind the transaction by connecting them to the purchase with every piece of data you have.

Rebuttal Letter for a Fraud Claim

Subject: Rebuttal for Chargeback Case #[Your Case Number]

To Whom It May Concern,

We are writing to dispute the chargeback for transaction #[Transaction ID] in the amount of $[Amount], dated [Transaction Date]. This was filed under reason code [Reason Code], claiming the purchase was unauthorized.

Our records show this transaction was legitimately placed by the cardholder. We have compiled compelling evidence connecting the customer to this specific order.

Here’s a quick summary of the transaction timeline and the proof we’ve attached:

- Order Placement: The order was placed on [Date] from IP address [IP Address], which geolocates to [City, State]—a direct match with the cardholder's billing address.

- Payment Verification: The payment was successfully authorized with a positive AVS match ([AVS Result]) and CVV match ([CVV Result]).

- Customer History: This customer has [Number] prior undisputed purchases with us, all shipped to the same verified address.

- Delivery Confirmation: The order shipped via [Carrier] (Tracking #[Tracking Number]) and was successfully delivered to the cardholder's address on [Delivery Date].

The attached documents confirm these facts:

- Exhibit A: Transaction receipt showing the AVS/CVV results.

- Exhibit B: Geolocation data for the IP address used at purchase.

- Exhibit C: Customer’s complete order history.

- Exhibit D: Proof of delivery with signature or photo.

Based on this evidence, it's clear the charge is valid. We respectfully request you reverse this chargeback.

Sincerely,

[Your Name] [Your Company]

Template 2: The "SaaS Subscription Canceled" Claim

If you run a subscription business, you've seen this one. A customer says they canceled but were billed anyway. To win this, you need to show they agreed to your terms, used the service during the disputed billing cycle, and never followed your cancellation policy.

Rebuttal Letter for a Subscription Cancellation Claim

Subject: Rebuttal for Chargeback Case #[Your Case Number]

To Whom It May Concern,

We are disputing the chargeback on transaction #[Transaction ID] for $[Amount] from [Transaction Date]. The customer filed under reason code [Reason Code], claiming they had canceled their recurring subscription.

Our evidence confirms the cardholder agreed to our terms, failed to cancel their account per our policy, and actively used our service during the billing period in question.

Please consider these key facts:

- Subscription Agreement: The customer signed up on [Signup Date], explicitly agreeing to our Terms of Service which state cancellations must be made through their account dashboard.

- Service Usage: Our logs show the user accessed their account multiple times after the disputed billing date. Their last login was [Last Login Date].

- No Cancellation Record: We have thoroughly checked our systems and have no record of a cancellation request from this customer—not in their account dashboard or via any of our support channels.

Our supporting documents are attached:

- Exhibit A: A screenshot of the checkout page where the customer agreed to our Terms of Service.

- Exhibit B: The customer’s service usage and login logs for the disputed period.

- Exhibit C: A clear copy of our cancellation policy.

The evidence points to a valid, active subscription and service usage. We request that this chargeback be reversed. For merchants looking to automate this process, it's worth exploring different chargeback representment campaigns to gain a strategic edge.

Sincerely,

[Your Name] [Your Company]

Template 3: The "Product Not as Described" Claim

This type of dispute can feel personal and subjective, but your defense has to be purely factual. The goal is to prove that your product page was accurate and that the customer knew exactly what they were buying.

Rebuttal Letter for a "Product Not as Described" Claim

Subject: Rebuttal for Chargeback Case #[Your Case Number]

To Whom It May Concern,

We are writing to dispute the chargeback for transaction #[Transaction ID] for $[Amount] on [Transaction Date]. The claim was filed under reason code [Reason Code], stating the "Product Not as Described."

We strongly contend this claim is invalid. The product delivered to the customer was identical to the description, specifications, and images on our product page at the time of their purchase.

Here is a breakdown of our evidence:

- Accurate Product Listing: We have attached screenshots of the live product page from the day the customer ordered, highlighting all features and specs.

- Customer Acknowledgment: The order confirmation email, sent on [Date], clearly restates the product details for their records.

- No Prior Contact: The cardholder never reached out to our customer service team to report an issue or to request a return under our clearly posted policy before initiating this chargeback.

The following evidence is attached for your review:

- Exhibit A: Screenshots of the product page as it appeared at the time of purchase.

- Exhibit B: A copy of the order confirmation email sent to the customer.

- Exhibit C: A copy of our return and refund policy.

This documentation proves the product was represented accurately and fairly. We ask that you please reverse this chargeback.

Sincerely,

[Your Name] [Your Company]

Submitting Your Rebuttal The Right Way

You’ve just put together a rock-solid rebuttal letter. That's a huge step, but it’s only half the job. Even the most bulletproof argument can be dead on arrival if it's submitted incorrectly, late, or in a file format the processor’s system rejects. Getting the submission right is a critical part of your defense, and you need to know that every platform—from Stripe to Shopify Payments to PayPal—has its own set of rules.

The one thing that's the same across the board? Deadlines are non-negotiable. Most processors give you a window of 7 to 21 days to respond. If you miss that deadline by even a minute, you automatically lose the dispute. The strength of your evidence becomes completely irrelevant. This is exactly why early chargeback alerts are so valuable; they give you a crucial head start to get your case in order long before the official clock starts ticking.

Navigating Processor Portals

Forget about mailing or emailing your rebuttal. These days, it’s all handled through your payment processor’s dispute management portal. You'll be uploading everything directly into their system.

- Stripe: The Stripe Dashboard is one of the more straightforward platforms. You can upload all your evidence directly into the specific dispute record. They really prefer a single, consolidated file.

- Shopify Payments: This is all managed from your Shopify admin panel. Look for the "Submit Response" button on the chargeback screen, which lets you add text and upload your documents.

- PayPal: The Resolution Center will walk you through the steps, but from my experience, it can be a bit more rigid about file types and sizes. Plan accordingly.

No matter which platform you’re using, there’s one golden rule: consolidate everything. Your rebuttal letter, receipts, screenshots, delivery confirmations—all of it—should be combined into one single, clean PDF file. This simple step ensures no documents get overlooked and makes life much easier for the person reviewing your case.

A disorganized submission with a bunch of scattered files just looks unprofessional. A single, well-organized PDF presents your argument as a cohesive, easy-to-review package that shows you’re serious.

Record-Keeping and Why It Matters

Once you hit that "submit" button, you’re not quite finished. Good record-keeping is a habit that pays dividends. Always, always save a copy of the final PDF you submitted for every single case.

This documentation is priceless. It helps you track your win rates, spot patterns in why customers are filing disputes, and continuously refine your rebuttal letter template.

This disciplined approach is more important than ever. With some studies suggesting that a staggering 45% of all disputes are fraudulent, you're up against a significant threat. This isn't just a minor cost of doing business; it's a massive problem that drains revenue and is projected to hit $28.1 billion in losses by 2026.

The principles of careful documentation apply across your business, from fighting chargebacks to correcting VAT errors. Your internal records become a library of past cases, helping your team learn and respond more effectively next time. And if you ever find yourself stuck on a tricky dispute, our team is here to help when you contact our support specialists. Having those detailed records ready makes it much easier for us to give you the best possible guidance.

Common Questions About Chargeback Rebuttals

Even with the best tools and checklists, the chargeback process can throw some curveballs. When you're in the thick of it, some practical, real-world questions always pop up. Getting these right can be the difference between winning and losing, so let's clear up a few of the most common ones I hear from merchants.

How Long Should My Rebuttal Letter Be?

Keep it to one single page. I can't stress this enough. The people reviewing your case at the bank are looking at hundreds of these a day. If you send them a novel, they're going to skim it, and your most important points will get lost in the shuffle.

Your letter needs a short, punchy summary right at the top. Then, use bullet points to call out your best evidence. Finish with a simple sentence stating why the chargeback should be reversed. All the supporting documents—your receipts, shipping confirmations, AVS match screenshots—should be attached separately and clearly labeled. Don't embed them in the letter.

Can I Use The Same Rebuttal Letter Template For Every Dispute?

Absolutely not. This is one of the fastest ways to lose a dispute. A good rebuttal letter template is a fantastic starting point, but you have to treat it like a blueprint, not a finished house.

Each chargeback has a specific reason code and its own story. You have to tailor your response to directly counter the cardholder's claim.

A rebuttal for a "Product Not Received" claim is all about proof of delivery. A rebuttal for a "Fraud" claim, on the other hand, needs to prove the real cardholder was the one who bought the item. Reviewers can spot a generic, copy-and-pasted letter from a mile away, and they are rarely convincing.

What Happens If I Lose The Chargeback Rebuttal?

If your rebuttal is denied, the bank finalizes the fund transfer back to the customer. That money is gone for good. On top of that, you're stuck paying the non-refundable chargeback fee your processor charged you.

The loss also counts against your chargeback ratio. This is a critical health metric for your merchant account, and if it creeps too high, you could face higher fees, or worse, lose your ability to process payments altogether.

Some card networks, like Visa and Mastercard, offer a second appeal stage called pre-arbitration. But honestly, it's a complicated, expensive, and time-consuming headache. Your best shot is always the first one, so make sure you put together a killer case from the get-go.

Is It Better To Refund A Customer Than To Fight A Chargeback?

This really comes down to timing. It's a strategic call.

Before a chargeback is filed: If a customer reaches out to you directly with a valid problem, issuing a quick refund is almost always the right move. You save the customer relationship, and more importantly, you avoid the chargeback, the fee, and the hit to your ratio.

After a chargeback is filed: If the dispute is clearly friendly fraud and you have the evidence to back it up, you should fight it. Fighting protects your revenue and shows fraudsters you're not an easy mark.

This is exactly why chargeback alert services are so valuable. They give you a 24-72 hour heads-up, letting you refund a disgruntled customer before the bank officially files the chargeback. You get to dodge the bullet completely.

Stop losing revenue to preventable disputes. Disputely integrates with top alert networks to notify you of customer issues before they become costly chargebacks, giving you the power to refund and protect your merchant account. Learn how you can reduce chargebacks by up to 99%.