The Time Limit for Chargeback on Credit Card Explained

Ever heard that the time limit for a chargeback on a credit card is a firm 120 days? It’s a common misconception, and believing it can be a costly mistake for any business. While 120 days is a good rule of thumb, it’s far from a universal standard. The real deadline can swing wildly depending on the card network—like Visa or Mastercard—and the specific reason the customer is disputing the charge.

Getting Ahead of the Chargeback Clock

For any ecommerce business owner, chargebacks are a constant headache, threatening both your revenue and the health of your merchant account. The whole process can feel like a race against a clock you can’t see, and misunderstanding the timelines is one of the easiest ways to lose a dispute.

It’s better to think of chargeback deadlines not as one single countdown but as a series of different timers, each one triggered by a unique event. The 120-day figure is just one of many possibilities.

Deconstructing the 120-Day Myth

The Fair Credit Billing Act (FCBA) is the law that gives U.S. consumers the right to dispute charges, but the major card networks write their own playbooks. These rulebooks are surprisingly detailed, with specific timelines designed to cover all sorts of situations because they know that not all problems pop up right after a purchase.

This creates a few different time windows you absolutely need to have on your radar:

- The Cardholder's Window: This is how long your customer has to call their bank and start the dispute process. It can be anywhere from 75 to a whopping 540 days after the transaction.

- Your Response Window: Once a chargeback is filed, the clock is on you. You get a tight, non-negotiable deadline of just 20-45 days to gather your evidence and fight back. Miss it, and you automatically lose.

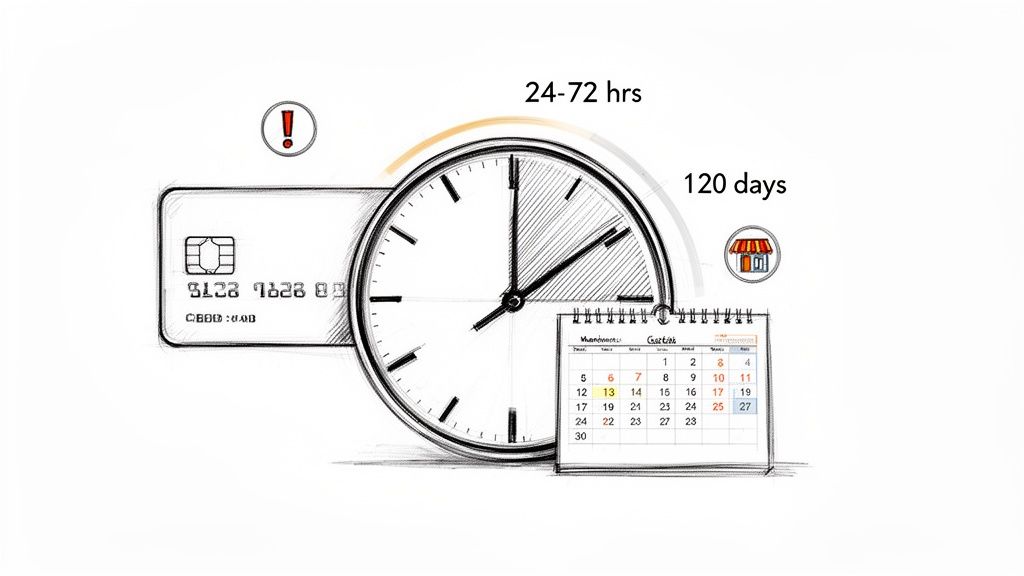

- The Golden Window: This is your best shot at avoiding a chargeback altogether. The first 24-72 hours after a customer has an issue is your prime opportunity to solve the problem directly before they even think about calling their bank.

Why You Can’t Afford to Wait

Ignoring the early warning signs is a huge financial gamble. Chargebacks are on the rise, with the global volume expected to jump by 24% between 2025 and 2028, hitting an incredible 324 million incidents. That growth translates into staggering costs, climbing from $33.79 billion to $41.69 billion over the same period. You can dig into more chargeback trends and their impact on businesses to see the full picture.

The smartest way to manage the time limit for a chargeback is to act before the official clock even starts. Proactive customer service in those first 72 hours can stop a simple complaint from turning into a costly blemish on your record.

With these basics covered, we can now dive into how the different card networks and reason codes change the game entirely.

How Card Networks and Reason Codes Define the Timeline

One of the most dangerous myths in ecommerce is believing there's a single, universal time limit for a chargeback on a credit card. The truth is, the deadline isn't set in stone. It’s a moving target defined by two crucial factors: the card network (like Visa or Mastercard) and the specific reason code tied to the dispute.

Think of reason codes as the "why" behind the chargeback. A customer's bank can't just claw back money; they have to categorize the dispute with a code, like "Fraudulent Transaction" or "Product Not Received." This code is what really starts the clock, and each one has its own unique timeline.

This system makes sense when you think about it. The card networks know that discovering a fraudulent charge happens on a different schedule than realizing a recurring subscription was never canceled.

The Role of Reason Codes in Setting the Clock

Reason codes are the official language of chargebacks. They’re the standardized way an issuing bank communicates the core of the customer's complaint. This classification doesn't just explain the problem; it dictates the entire timeline.

For merchants, getting a handle on these codes is like learning the other team's playbook. Knowing the reason code tells you not just why you got the chargeback, but also how long the customer had to file it. More importantly, it clues you in on exactly what kind of evidence you'll need to fight it successfully.

For example, a dispute over a defective product might give a customer 120 days to file, but that countdown often starts from the day they received the item, not the day they clicked "buy." That's a massive difference for any business with long shipping times.

How Timelines Vary Across Major Card Networks

While reason codes set the ground rules, each card network has its own interpretation. Visa, Mastercard, and American Express all play by their own rulebooks, which means the same dispute can have wildly different deadlines depending on the card used.

- Visa: Their general window is 120 days for most consumer disputes, but that’s a very loose rule. For something like "services not rendered," the clock can run for up to 540 days from the original transaction date.

- Mastercard: They also stick to a 120-day standard for many common issues. However, their rules have plenty of exceptions for things like processing errors or funky recurring billing, where the timeline might start from the day the cardholder spotted the problem on their statement.

- American Express: Amex is known for being more flexible and often more generous to its cardholders. They don't always use a strict day count and can review disputes on a case-by-case basis, which makes their process a bit of a black box for merchants.

The key takeaway here is simple: you can't use a "one-size-fits-all" approach. A chargeback for the same exact issue—say, a gym membership that kept billing after cancellation—could have a different filing deadline depending on whether the customer paid with a Visa or a Mastercard.

To make this crystal clear, let's break down a few common scenarios.

How Reason Codes Impact Chargeback Time Limits

This table shows just how dramatically the filing deadline can shift based on why the customer is disputing the charge.

| Dispute Reason | Visa Time Limit (General) | Mastercard Time Limit (General) | Key Merchant Considerations |

|---|---|---|---|

| Fraudulent Transaction | Typically 120 days from the transaction processing date. | Typically 120 days from the transaction processing date. | These timelines are very firm. Your job is to prove the legitimate cardholder authorized the purchase. |

| Merchandise Not Received | Usually 120 days, but the clock starts from the expected delivery date, not the purchase date. | Up to 120 days from the last expected delivery date or date services were supposed to be provided. | The date of purchase is almost irrelevant here. It’s all about your shipping and delivery records. |

| Incorrect Recurring Billing | Can be up to 540 days from the transaction date if the cardholder was unaware of the charge. | 120 days from the statement date on which the disputed transaction first appears. | Proving the customer agreed to the terms is everything, especially for disputes filed months after the initial sign-up. |

As you can see, the time limit for chargeback on credit card is far from a simple number. A customer who bought a custom-built table with a six-month delivery window has a much, much longer dispute timeframe than someone who bought a digital e-book.

The context, which is defined by the reason code, is everything. By getting comfortable with these nuances, you can start to anticipate risks and build a much stronger, more informed defense when a dispute inevitably lands on your desk.

When Does the Chargeback Clock Actually Start Ticking?

Knowing the official chargeback time limit is one thing, but the real trick is understanding the precise moment that countdown begins. It's a detail that trips up countless merchants, leaving them exposed to disputes they thought had long expired.

Many people fall into the trap of assuming the clock starts on the transaction date. While that’s sometimes true, it's a dangerously simple assumption for most ecommerce businesses. The trigger for the countdown is entirely situational—it all depends on what the customer is claiming went wrong.

Think of it like this: You can’t just know the length of the race. You have to know exactly when the starting pistol fires. That "pistol" could be the moment of purchase, the day a package was supposed to arrive, or even the afternoon a customer discovers a hidden flaw in a product.

This timeline illustrates just how different the starting point can be based on the type of dispute.

As you can see, a one-size-fits-all "start date" just doesn't apply in the world of chargebacks.

Decoding the Different Trigger Dates

To really get a handle on your risk, you need to get familiar with the common events that kick off the chargeback countdown. Each one creates a unique timeline and demands a different set of evidence from you to win the dispute.

Here are the most common triggers you’ll encounter:

- Transaction Processing Date: This is the most straightforward one. The clock starts the day the card is charged. It's typically used for disputes related to true fraud or processing errors where the problem is tied directly to the sale itself.

- Expected Delivery Date: This is the big one for "product not received" claims. A customer's window to file a dispute doesn't begin when they place the order; it starts on the day they were supposed to get their item.

- Date of Discovery: This trigger is for issues that aren't obvious right away. Think of a hidden product defect or an unauthorized recurring charge a customer just spotted on their statement. The clock can start ticking months after the original transaction.

For instance, say you sell a subscription box and promise delivery by June 15th. If the customer claims it never arrived, their 120-day window to file that claim starts on June 15th, not the day they ordered back in May. This effectively stretches out the total time you’re on the hook for a potential chargeback.

Juggling Two Different Clocks

Here’s a crucial concept every merchant needs to master: once a dispute is filed, there are two separate clocks running at the same time. Getting them mixed up is a surefire way to lose the case by default.

The cardholder gets months to file a dispute, but you only have a few short weeks to respond. This imbalance is exactly why you can't afford to be reactive. Miss your deadline, and you automatically forfeit the revenue, no matter how strong your evidence is.

The first clock is the cardholder’s filing window. This is the generous 75- to 540-day period we've been talking about, where they can contact their bank to initiate a chargeback.

The second, and far more urgent, clock is your merchant response window. As soon as that chargeback is filed and lands on your desk, this much shorter timer starts. You typically get just 20 to 45 days to gather your compelling evidence and submit your defense.

How Your Business Model Changes the Game

The impact of these trigger dates looks very different depending on what you sell.

- Ecommerce Brands: Your world revolves around that expected delivery date. Flawless shipping records, easily accessible tracking numbers, and solid proof of delivery are your best weapons against "product not received" claims that can pop up months after a sale.

- Subscription Services: For you, the date of discovery is a huge deal. A customer might not notice an incorrect recurring charge for a few billing cycles. Their dispute window often resets with each new transaction, meaning you could face a chargeback for last month’s payment, even if they signed up a year ago.

Getting a firm grasp on these trigger points isn’t just about following the rules; it's about smart risk management. When you know precisely when your liability starts and ends for every sale, you can build a much stronger, more resilient defense against disputes.

Exceptions and Special Conditions That Extend Deadlines

Just when you think you’ve got the standard timelines figured out, the chargeback system throws a few curveballs. There are a handful of special conditions that can stretch the filing window far beyond the usual limits, and if you aren’t aware of them, they can come back to bite you.

These exceptions exist for a good reason: sometimes, problems with a purchase don't show up right away. For a merchant, however, these gray areas are where a lot of the risk lives. A sale you thought was closed months ago could suddenly reappear as a costly dispute.

The most common reason the time limit for a chargeback on a credit card gets extended is when a product or service is delivered long after the customer pays. Think about custom-made goods, tickets to an event, or professional services scheduled for a future date. In these cases, the clock doesn't start ticking on the transaction date. Instead, it starts from the day the service was supposed to happen or the product was supposed to arrive.

This makes perfect sense from a consumer's perspective. How could someone know a concert will be canceled or a custom-built table will have a defect until the event date or delivery day? Understanding this delayed timeline is absolutely critical for any business with a long fulfillment cycle.

Delayed Delivery and Future-Dated Services

This is probably the most frequent exception you'll encounter. It covers any transaction where the customer pays now for something they'll receive later. We’re talking about pre-ordering a new video game, booking a hotel for a vacation six months away, or paying a deposit for a catering service.

The card network rules are built to protect the cardholder here. The countdown for filing a dispute only begins on the expected date of service or delivery.

- Example 1: The Annual Software Subscription. A customer buys a yearly license in January. In October, a critical bug makes the software unusable, and they can't get it resolved. Their window to file a "product not as described" chargeback starts in October, not way back in January when they first paid.

- Example 2: The Wedding Photographer. A couple pays a deposit a year in advance. On the big day, the photographer is a no-show. The chargeback clock starts ticking from the wedding date, giving the couple plenty of time to dispute the charge for services they never received.

The Nuances of International Transactions

Selling globally opens up your business to the world, but it also adds another layer of complexity to chargeback rules. When you and your customer are in different countries, you might be subject to different regional laws and card network policies.

For example, some consumer protection laws in Europe give cardholders much more generous timeframes for disputes than what's standard in the U.S. This means a customer in Germany could file a chargeback long after your domestic deadline has passed. If you have an international customer base, you have to be ready for this.

Navigating these exceptions all comes down to meticulous record-keeping. The burden of proof is on you, the merchant, to show you delivered on your promise, even if the dispute pops up many months after the initial transaction.

This documentation is your shield. Keeping clear records—like terms of service agreements, delivery confirmations, and all customer communications—is the only way to effectively fight a chargeback that falls outside the standard window. For merchants who find their funds frozen while dealing with these issues, learning how to manage a Shopify payment hold can offer some much-needed strategies.

When Compelling Evidence Becomes Your Best Defense

In these extended timeline scenarios, your most powerful weapon is compelling evidence. It’s not just about proving a transaction happened; you have to prove you delivered exactly what the customer paid for, when they expected it.

So, what does great evidence look like?

- Signed Contracts or Agreed Terms: Proof that the customer saw and agreed to the delivery schedule or service date.

- Proof of Delivery: A shipping confirmation with a tracking number showing the package arrived at the right address.

- Customer Communications: Emails, support tickets, or chat logs where the customer acknowledges they received the item or were happy with the service.

By planning for these exceptions and having your documentation in order from day one, you can protect your revenue from those surprise disputes that seem to come out of nowhere, long after you've considered a sale complete.

How to Proactively Beat the Chargeback Clock

Knowing the chargeback time limits is how you defend yourself, but preventing them in the first place is your best offense. It’s all about shifting from a reactive "wait-and-see" approach to a proactive strategy that protects your revenue and keeps your merchant account healthy.

Think about it: instead of getting hit with a formal dispute weeks after a transaction, what if you knew the second a customer complained to their bank? Modern tools make this possible.

This approach completely flips the script. Forget scrambling to meet a 30-day response deadline. This gives you a precious 24-72 hour window to make things right directly with the customer. It's the secret weapon for getting ahead of deadlines before they even start ticking.

Introducing Pre-Dispute and Alert Systems

Game-changing services like chargeback alerts and pre-dispute networks give you that critical heads-up. These systems, run by the card networks themselves, are essentially an early-warning alarm. The moment a cardholder calls their bank to raise an issue, the network sends an alert straight to you.

You're no longer in the dark, waiting for a formal notice to snail-mail its way from your processor. You get real-time intelligence that lets you act immediately.

The two main players you'll hear about are:

- Ethoca Alerts (owned by Mastercard): This network partners with thousands of issuing banks around the world, giving you near-instant notifications about pending customer disputes.

- Verifi CDRN (owned by Visa): The Cardholder Dispute Resolution Network (CDRN) works just like Ethoca, giving you a chance to resolve an issue before it ever becomes a full-blown chargeback.

By plugging into these alert systems, you can intercept a problem at the earliest possible moment. You have the power to simply issue a refund, solve the customer's problem, and neutralize the threat before it ever affects your business.

How Rapid Dispute Resolution Changes the Game

Building on this idea, Visa's Rapid Dispute Resolution (RDR) takes prevention to the next level. RDR is an automated tool that lets you set your own rules for handling these pre-disputes. Instead of having a team member review every single alert, you can tell the system how to respond automatically.

For example, you could create a rule to automatically refund any flagged transaction under $25. When an alert comes in that fits your rule, a refund is issued on the spot—no manual work required. This not only saves you from a chargeback but also frees up your team's time for more important tasks.

RDR transforms the entire dispute process. You go from a reactive, manual firefight to an automated, proactive defense. It’s the closest you can get to stopping a chargeback before it technically even exists.

This automated approach ensures you never miss that crucial 24-72 hour window. For high-volume businesses, it's a lifesaver. This kind of system is a cornerstone of any serious defense, which is why it's so critical for effective strategies like those needed for https://disputely.com/campaign/q4-representment.

The Payoff of a Proactive Strategy

Going proactive with alerts and RDR does a lot more than just stop a few chargebacks. It creates a ripple effect of benefits that protect your entire payment ecosystem.

- Protects Your Dispute Ratio: Every chargeback you deflect is one less hit to your merchant account. Keeping this ratio low is absolutely vital for avoiding penalties and staying in good standing with your payment processor.

- Avoids Costly Fees: Chargebacks always come with non-refundable fees, often ranging from $20 to $100 a pop. Preventing the dispute means you also sidestep that fee, saving you potentially thousands over time.

- Reduces Operational Burden: Fighting chargebacks is a frustrating, time-sucking process. When you resolve issues upfront, you cut down on the hours your team spends digging up evidence and writing responses.

- Improves Customer Satisfaction: A lot of the time, a fast refund is all the customer really wanted. By solving their problem instantly, you can turn a potentially bad experience into a positive one and maybe even keep them as a customer.

Ultimately, getting ahead of the clock requires a layered defense. By combining these alerts with solid ecommerce fraud prevention best practices and clear customer communication, you build a fortress that makes it incredibly difficult for preventable chargebacks to ever get through.

Answering Your Top Questions About Chargeback Time Limits

Even when you feel like you have a handle on the rules, the world of chargebacks can throw you a curveball. The complex timelines and competing deadlines often leave merchants scratching their heads. Let's clear the air and tackle some of the most common questions about the time limit for a chargeback on a credit card.

Think of this as your field guide to navigating the dispute process with a lot more confidence.

Can a Chargeback Happen After 120 Days?

Absolutely. A chargeback can, and often does, happen well after 120 days. Thinking of 120 days as a hard-and-fast rule is one of the most common—and costly—misconceptions in e-commerce.

What really matters isn't just the length of the window, but when the clock starts ticking. It's almost never the date of the transaction. For some Mastercard reason codes, a cardholder has up to 540 days to file a dispute.

Consider a few real-world examples:

- Non-Receipt of Goods: If a customer pre-orders an item that ships in three months, the chargeback clock doesn't start until after the promised delivery date has come and gone.

- Recurring Billing: For a subscription, a customer can dispute the latest charge months or even years after they first signed up. The clock resets with each billing cycle.

- Services Not Rendered: Imagine a customer pays for concert tickets six months in advance. If the show is canceled, their dispute window begins on the date the concert was supposed to happen, not the day they bought the tickets.

Sticking rigidly to a "120-day rule" is like inviting trouble. You have to look at the context of the entire transaction to understand your real-world risk.

What Is the Difference Between a Cardholder and Merchant Time Limit?

This is a crucial distinction, and mixing them up is a guaranteed way to lose a dispute. There are two completely separate clocks running, and they couldn't be more different.

The cardholder time limit is the generous window the customer has to call their bank and start a dispute. This is the one that can stretch from 75 to 540 days, giving them plenty of time to spot a problem.

The merchant response time limit is your clock. It's a much shorter, high-pressure window you have to fight back once a chargeback is filed. This deadline is typically just 20 to 45 days.

If you miss your response deadline, you automatically lose. It doesn't matter how strong your evidence is. This unforgiving clock is precisely why getting ahead of disputes is so critical.

The system is built to give the consumer the benefit of the doubt, putting all the pressure on you, the merchant, to be prepared and act fast.

How Do Chargeback Alerts Help Manage Time Limits?

Chargeback alerts flip the script entirely. They let you move from a reactive defense to a proactive offense. Instead of scrambling to meet a 30-day deadline after a chargeback hits, alerts give you a 24-72 hour heads-up to prevent the dispute from ever being filed.

Services like Visa's Rapid Dispute Resolution (RDR) and alerts from networks like Ethoca notify you the second a customer complains to their bank. This is your golden opportunity.

Here’s the play-by-play:

- A customer calls their bank to question a charge.

- Before a formal chargeback is created, the alert network pings you instantly.

- You now have a chance to issue a full refund and resolve the issue directly.

By refunding the customer, you stop the chargeback cold. You avoid the dispute fee, protect your merchant account's health, and never have to worry about the response deadline. You’re essentially beating the clock because the official timer never even starts. For a deeper dive into these strategies, our chargeback management blog has a ton of great info.

Does My Payment Processor Handle These Time Limits?

Think of your payment processor (like Stripe, Shopify Payments, or PayPal) as a messenger, not a manager. They facilitate the process, but they don't handle the deadlines for you.

Here's what your processor actually does:

- Notifies you that a chargeback has been filed.

- Gives you a portal to upload your evidence.

- Passes along the official response deadline from the card network.

Ultimately, the responsibility to gather compelling evidence and submit it on time is 100% on you. If you just wait for your processor's email, you're already on the back foot, fighting a formal chargeback. They manage the system's plumbing, but you're the one who has to build your case and win before time runs out.

Stop wasting time and money fighting lost causes. With Disputely, you can prevent up to 99% of chargebacks before they ever hit your account. Our platform plugs directly into alert networks to give you the power to resolve customer issues in real-time, protecting your revenue and your merchant account health. See how much you can save with Disputely and start defending your business proactively.