The Time Limit on Credit Card Chargeback Explained for Merchants

You've probably heard that the standard time limit for a credit card chargeback is 120 days. But if you're a merchant, relying on that simple number is a dangerous oversimplification. The reality is much more nuanced.

The "chargeback clock" doesn't always start ticking on the day of the sale. Depending on the situation, it might begin on the transaction date, the day the charge appears on a customer's statement, or even a future date when a product was supposed to be delivered.

Decoding the Chargeback Clock for Merchants

If you accept credit cards, getting a handle on chargeback timelines is non-negotiable. It's not just about following the rules; it's a core part of managing your cash flow and mitigating risk. Treating this as a fixed 120-day window is a common and often costly mistake.

Think of it less like a rigid deadline and more like a countdown timer that can be influenced by several players and specific circumstances. The entire process is a conversation between different parties, and each one has its own set of deadlines that all feed into the final timeline.

The Key Players in the Timeline

Three main groups dictate how this all plays out, and it's crucial to understand their distinct roles:

- Card Networks (Visa, Mastercard, etc.): They are the rule-makers. These networks set the maximum time a cardholder has to open a dispute.

- Issuing Banks (The Cardholder's Bank): This is the bank that gave your customer their credit card. They are responsible for actually starting the chargeback process based on the network's rules.

- Payment Processors (e.g., Stripe, PayPal): Your processor is the middleman. They pass the dispute information from the issuer to you, but they also set their own, much tighter deadlines for you to respond.

Imagine you're running a busy online shop. You're shipping out hundreds of orders a month, and things are going smoothly. Then, out of the blue, you get a chargeback notification for a sale you made almost four months ago. This is a real scenario.

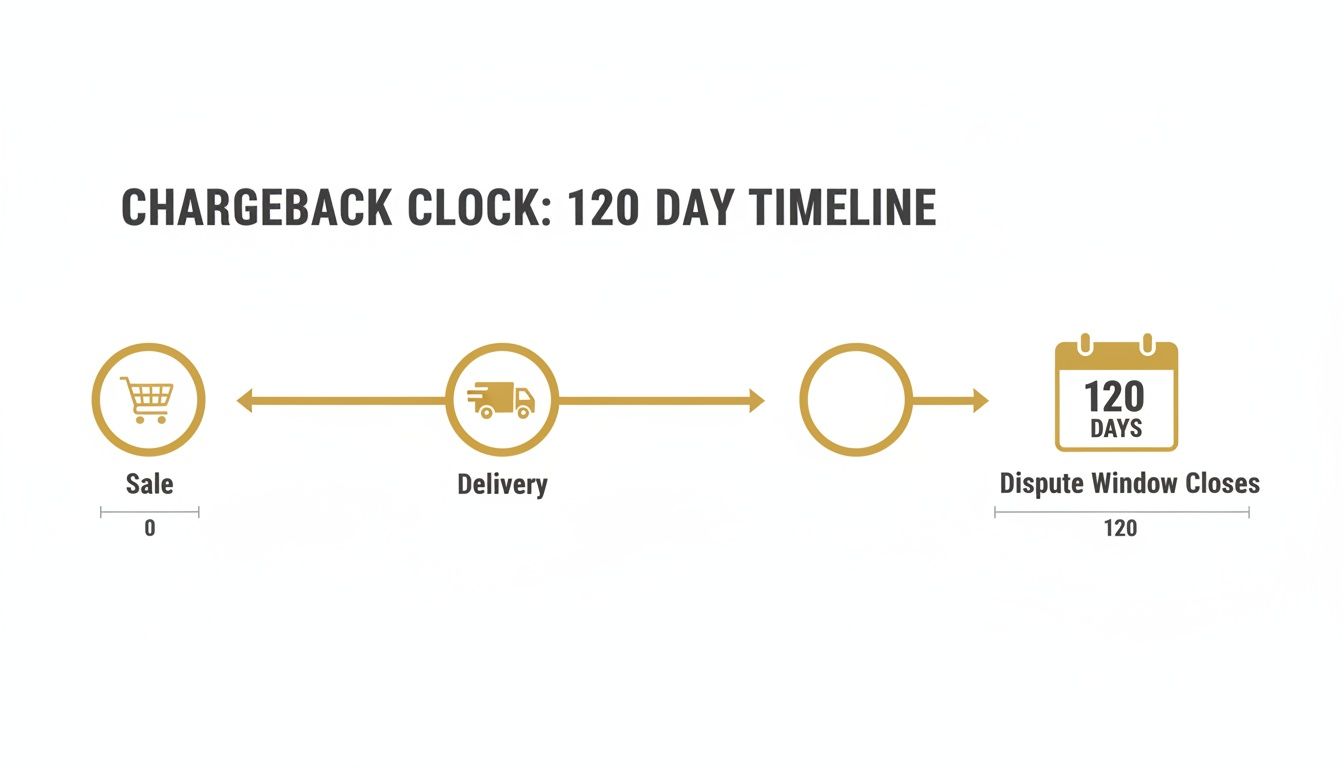

The 120-day window is the standard for Visa and Mastercard in major markets like the US and UK. Card network rules generally give consumers up to 120 days from the transaction date—or the expected delivery date, whichever is later—to file a claim. This is what allows a customer to dispute a charge for an "item not received" or "not as described" long after you've closed the books on that sale.

While the 120-day figure is a good benchmark for Visa, Mastercard, American Express, and Discover, the starting point for that countdown can differ. For instance, Visa and Mastercard often start the clock from the processing or delivery date, while AmEx tends to go by the date the transaction posts to the customer's statement. You can dig deeper into how chargeback windows are calculated on PayCompass.com.

Key Takeaway: The consumer’s timeline is a marathon, but the merchant’s response window is a sprint. While a customer may have months to file, you often have just a few weeks—or even days—to respond, making every moment count.

To get a clearer picture, it helps to see the standard consumer timelines side-by-side.

Standard Consumer Chargeback Filing Time Limits at a Glance

This table gives you a high-level look at the standard windows consumers have to initiate a chargeback with the major card brands.

| Card Network | Typical Consumer Filing Window | Clock Starts From |

|---|---|---|

| Visa | 120 Days | Transaction processing date or expected delivery date |

| Mastercard | 120 Days | Transaction processing date or expected delivery date |

| American Express | 120 Days | Transaction posting date (date it appears on statement) |

| Discover | 120 Days | Transaction processing date |

Remember, these are the maximums for the consumer. As we'll see, there are plenty of exceptions that can extend these timelines even further, and your window to fight back is always much, much shorter.

Navigating Card Network Timelines

That 120-day figure you often hear about? It’s a decent rule of thumb, but it's just the headline of a much more complicated story. In reality, the time limit on a credit card chargeback is a moving target, and it depends on two huge factors: the card network (Visa, Mastercard, AmEx, Discover) and the reason for the dispute.

Think of each card network as having its own rulebook for disputes. While they often have similar chapters, the small print can make all the difference. The clock might start ticking at different times, and some types of disputes have much shorter windows than others. A one-size-fits-all approach is a fast track to lost revenue.

This visual shows the classic chargeback timeline, from the moment of sale to the end of that standard 120-day consumer dispute window.

What jumps out here is that the clock often doesn't start until the customer receives the item, which means your financial risk can hang around a lot longer than the initial transaction date.

Visa and Mastercard Timelines

Visa and Mastercard are the giants, processing the vast majority of card transactions worldwide. Their timelines are similar, but the details matter. For both, the standard window for a customer to file a dispute is typically 120 days.

But the real key is the "reason code" that comes with the dispute—that's what truly sets the deadline.

- Consumer Disputes: For common issues like "product not as described" or "product not received," the 120-day clock usually starts from the transaction processing date or, more often, the expected delivery date.

- Authorization Issues: If the problem is technical, like an authorization error, the timeline can shrink dramatically, often to just 90 days.

- Fraud Disputes: Transactions flagged as fraudulent also tend to fall within that 120-day window from the transaction date.

This is where things get tricky. While 120 days is the standard for many consumer issues, disputes related to fraud or authorization can be capped at 75-90 days. For example, Visa's standard might be 120 days, but it drops to 75 days for invalid data. Mastercard follows a similar pattern, with a 120-day general rule but shortening it to 90 days for authorization errors. This can feel like a maze, but you can find a solid breakdown of regional chargeback timelines on Clear.Sale.

Here's a real-world example: A customer orders a jacket online on January 1st. The expected delivery date is January 15th. If the jacket never shows up, that 120-day clock starts ticking on January 15th, not January 1st. This gives them until mid-May to file a chargeback—a much longer risk window than many merchants expect.

American Express and Discover Differences

American Express and Discover play by slightly different rules because they often act as both the card network and the issuing bank. This unique structure can sometimes give their cardholders more flexible timelines.

While they also generally stick to a 120-day standard for customers to file, their internal processes can create exceptions. American Express, in particular, is famous for its customer-first philosophy, which can lead to them being more lenient with deadlines.

For you as a merchant, this means you can't just assume a dispute is "too old" because it’s past the 120-day mark. There might be other factors in play, especially with AmEx and Discover.

The main takeaway is this: you can't apply a single timeline to every dispute. Each chargeback has its own unique expiration date, dictated by the network, the reason code, and the story behind the transaction. Getting a handle on these rules is the first step to building a defense strategy that actually works.

The Merchant Response Window: A Race Against Time

Once a customer files a chargeback, the long, flexible timeline they had to work with comes to a screeching halt. The spotlight swivels directly to you, the merchant, and a new clock starts ticking—loudly. While a cardholder might have several months to get a dispute rolling, you get just a fraction of that time to build your defense.

Think of the consumer’s time limit as a marathon. They can pace themselves, consider their options, and file when they're ready. Your response window, on the other hand, is a high-stakes sprint. Missing this deadline isn’t just a minor setback; it's an automatic forfeit of the dispute and the revenue that goes with it.

The Sprint Against the Clock

For merchants, the response window is shockingly brief. Visa generally gives you 30 days from the day you’re notified to submit your compelling evidence. And the pressure is mounting: starting in 2025, Mastercard is tightening its timeframe from 45 days down to 30 days for many disputes, especially those related to digital goods and services.

This compressed schedule leaves virtually no room for error. You have to scramble to pull together all the necessary documents—receipts, shipping confirmations, customer service emails, IP logs—and assemble them into a cohesive and persuasive rebuttal. It’s a constant fire drill, and for businesses in high-risk industries like travel or subscription boxes, it can feel completely overwhelming.

But here’s the critical detail that catches so many merchants off guard: the card network’s deadline isn't always your real deadline.

Key Insight: Your payment processor almost always gives you a shorter response window. While Visa might offer 30 days on paper, your processor could demand your evidence within just 7-10 days. They create this buffer for their own internal processing, but it dramatically cranks up the urgency on your end.

Why This Short Window Is So Challenging

That tight deadline creates a domino effect of operational headaches. It’s not just about finding a single receipt; it’s about constructing a rock-solid legal case under intense pressure.

Here are the main hurdles you'll be up against:

- Evidence Gathering: You need to dig up transaction details, shipping tracking numbers, delivery confirmations, AVS/CVV match results, and any and all communication you had with the customer. For a busy online store, this is a huge administrative weight.

- Formatting and Submission: Every card network and processor has its own strict rules for how evidence must be formatted and submitted. You could have a slam-dunk case, but if you don’t present the proof correctly, it can get thrown out.

- Resource Drain: Pulling your team off their regular duties to fight chargebacks means they aren't focused on what actually grows your business, like sales and customer support. The true cost of a lost chargeback isn’t just the sale amount—it’s the payroll hours you burned trying to fight it.

Failing to meet these deadlines has serious consequences. Every missed deadline is a guaranteed loss, which directly hammers your chargeback ratio. If that number climbs too high, you’re looking at steep penalties, higher processing fees, or even losing your merchant account entirely. The pressure to be fast and accurate is immense, making a well-oiled internal process absolutely essential for survival. To learn more, check out our guide on how to prepare for a successful representment.

Exceptions That Change the Chargeback Rules

Just when you think you've got the standard 120-day time limit on a credit card chargeback down, the rulebook throws a curveball. The reality is, that deadline is more of a guideline than a hard-and-fast rule. A few common exceptions can stretch, shift, or even restart the clock, catching even seasoned merchants completely off guard.

If you're just circling a date on the calendar to manage your risk, you're setting yourself up for lost revenue. To truly protect your bottom line, you need to get familiar with these special circumstances that can keep a transaction in jeopardy long after it has cleared.

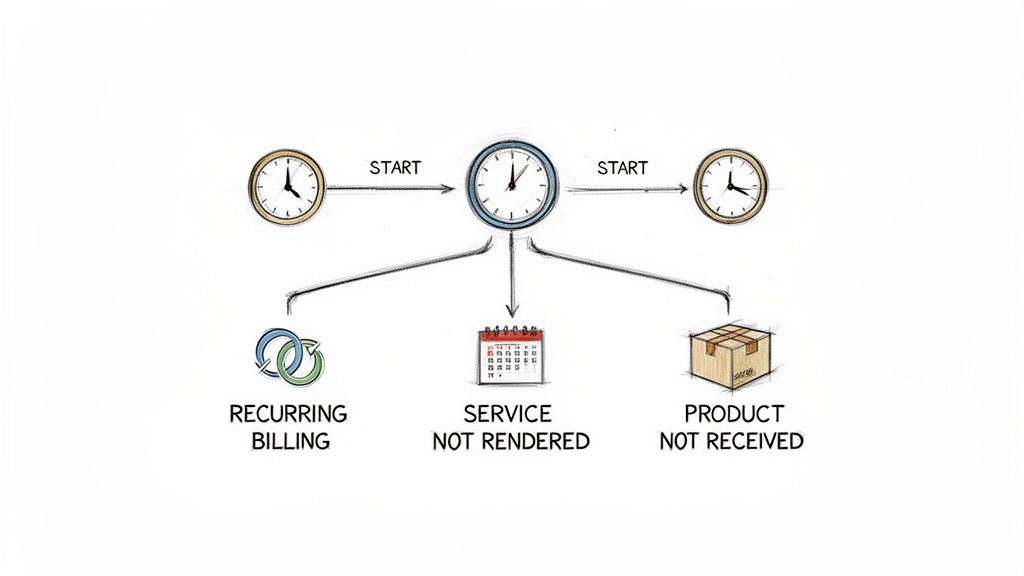

Recurring Billing and Subscription Models

For any business running on subscriptions, the chargeback clock works on a totally different wavelength. The card networks treat every single recurring payment as a brand-new transaction. This means the time limit on a credit card chargeback resets every time you bill the customer.

Think about it this way: a customer signs up for your monthly software service in January. By August, they realize they haven't logged in for months and decide to dispute the latest charge. Even though the original purchase was eight months ago, the dispute for their August payment is completely valid. Why? Because the 120-day clock for that specific transaction just started ticking.

This creates a rolling window of risk that lasts as long as the subscription is active. It's a critical vulnerability for any business that depends on recurring revenue.

Key Takeaway: For subscription merchants, chargeback risk doesn't vanish 120 days after sign-up. It renews with every single payment, meaning a dispute tied to the most recent bill can pop up many months, or even years, down the road.

Services Not Rendered or Goods Not Delivered

Here's another big one: what about services or deliveries scheduled for the future? In these situations, the chargeback clock doesn't start on the day the customer paid. It starts on the date the service was supposed to happen or the product was expected to arrive.

This rule makes sense, as it’s designed to protect people who pay for things far in advance. Let's break it down with a few real-world examples:

- Event Tickets: Someone buys concert tickets in March for a show in October. If the band cancels and there's no refund, the customer's 120-day window to file a chargeback starts in October, not back in March.

- Custom Furniture: A buyer orders a custom-built sofa with a 16-week delivery estimate. If the couch is a no-show, the clock starts ticking at the end of that 16-week period.

- Travel Bookings: A family pays for a hotel stay six months before their vacation. Any dispute about the room not being available would be tied to the check-in date, not the booking date.

Because of this delay, merchants can find themselves liable for a chargeback nearly a year after they processed the payment.

Defective Merchandise and Late Discovery

What happens if a product has a hidden flaw that doesn't show up right away? The card networks have an answer for this, too, often called a "date of discovery" provision.

Imagine a customer buys a new gadget, and it works flawlessly for five months before a manufacturing defect causes it to fail. In many cases, the chargeback clock will start from the day they discovered the problem, not the day they bought it. This can easily push the dispute window way past the standard time limit on a credit card chargeback.

While you can certainly fight these claims by pointing to your warranty policies, you still have to go through the dispute process. It’s just more proof that the financial risk of a sale doesn't magically disappear after four months. These exceptions show that managing chargebacks has to be a continuous effort, not just an item on a calendar.

Getting Ahead of the Clock with Proactive Alerts

Trying to keep up with the different chargeback timelines for every card network and reason code can feel like you're always playing defense. You're stuck waiting for a dispute to hit your account, and only then can you scramble to fight back against a ticking clock. But what if you could stop that clock before it even starts?

This is where proactive alert systems completely change the game. Instead of gearing up for a long, evidence-heavy battle, you get a small window to resolve customer issues before they ever become a formal, damaging chargeback.

From Reactive Defense to Proactive Resolution

Think of a traditional chargeback as a lawsuit. A customer files a formal complaint, and you're suddenly forced to dig up evidence and build a case within a strict timeframe. It's an adversarial, expensive process with absolutely no guarantee that you'll win.

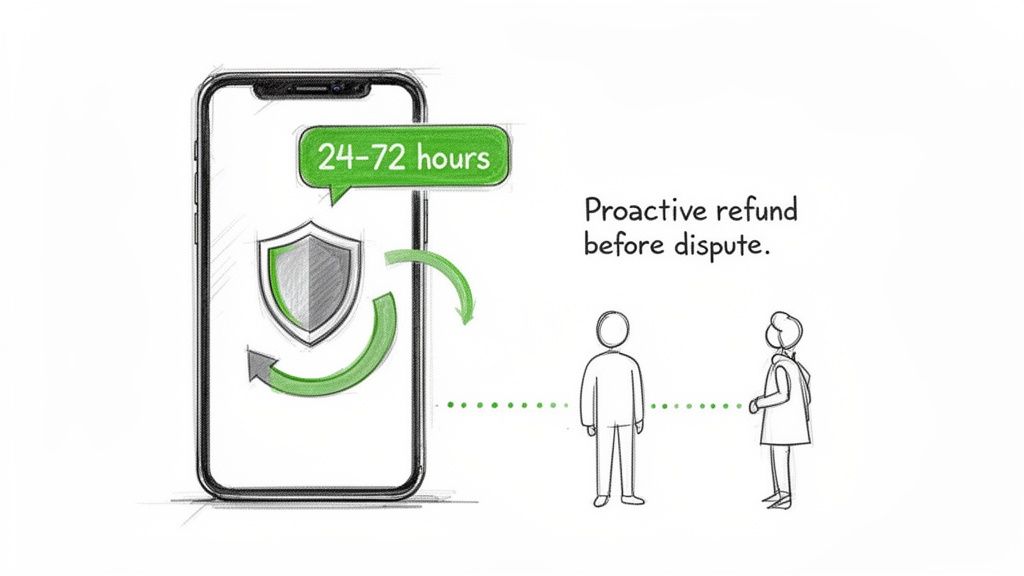

Proactive alerts, on the other hand, are more like pre-dispute mediation. When a customer calls their bank to question a charge, the bank—instead of immediately opening a chargeback—sends an alert through networks like Visa’s Rapid Dispute Resolution (RDR) or Mastercard’s Ethoca.

This alert creates a crucial 24 to 72-hour window for you to act. You get an immediate notification about the customer's problem, giving you a chance to issue a refund and fix it on the spot. If you do, the chargeback is never filed. The problem is solved, and the whole dispute process stops dead in its tracks.

Key Takeaway: Proactive alerts shift your strategy from fighting chargebacks to preventing them. This controlled approach lets you handle customer service issues directly, bypassing the entire formal dispute system and its punishing timelines.

The Power of the 24-72 Hour Window

That small window of opportunity is incredibly powerful. It transforms a potential month-long fight into a simple, automated decision. Rather than scrambling to find shipping proof from four months ago, you just have to decide whether to refund the transaction right now.

Here’s a practical look at the benefits of this approach:

- Avoid the Chargeback Entirely: This is the biggest win. The dispute never lands on your merchant account, so it can't harm your business's reputation with the processors.

- Protect Your Dispute Ratio: Payment processors watch your chargeback-to-transaction ratio like a hawk. If it creeps over their threshold (often around 1%), you can be hit with fines or even have your account terminated. Alerts keep this ratio safely in the green.

- Eliminate Processor Penalties: Every single chargeback comes with a non-refundable fee from your processor, usually between $25 and $100, whether you win or lose. Preventing the chargeback means you sidestep that automatic penalty.

- Prevent Costly Account Holds: High dispute rates are a major red flag for processors, often leading them to place a hold or reserve on your funds and strangle your cash flow. If you've ever had a surprise payment hold, you know how disruptive it is. Learn more about how to handle a Shopify Payments hold in our detailed guide.

Making the Strategic Choice

Of course, this doesn't mean you have to refund every single alert. A smart alert system lets you set up rules to automatically filter and manage these notifications. For instance, you could decide to automatically refund all transactions under $30 but flag any larger amounts for a manual review.

This gives you strategic control. You can weigh the cost of the refund against the guaranteed cost of a chargeback fee, the time you'd waste fighting it, and the potential damage to your merchant account. For most businesses, refunding a questionable transaction is a far smarter, more cost-effective outcome than rolling the dice in the high-stakes chargeback process.

Ultimately, using pre-dispute alerts means you're no longer a victim of the confusing time limit on credit card chargeback rules. You get out in front of the problem, take control of the outcome, and protect your revenue for the long haul.

Answering Your Top Questions on Chargeback Time Limits

Trying to pin down chargeback timelines can feel like chasing a moving target. Just when you think you have the rules figured out, a weird exception pops up and leaves you scrambling. It’s a common frustration for merchants, so let's clear the air.

This section tackles the most frequent and tricky questions we hear about chargeback time limits. Think of it as a practical field guide to help you move from reacting to disputes to proactively protecting your bottom line.

Can a Chargeback Really Be Filed After 120 Days?

Yes, and it happens more often than you'd think. The 120-day benchmark is thrown around a lot, but treating it as a hard-and-fast rule is a surefire way to get blindsided. In reality, that clock doesn't always start on the day of the transaction.

Several common scenarios can stretch this window out significantly. For instance, if you sell tickets to an event six months from now, the countdown for a dispute usually begins after the event date has passed. For subscription models, every single recurring payment is a new transaction, each with its own timeline.

The Bottom Line: The 120-day rule is a guideline, not a guarantee. Things like future delivery dates, recurring billing, and even the late discovery of a product defect can all push the filing deadline far beyond the standard timeframe.

On top of that, the card networks themselves have specific rules for things like criminal fraud that can allow for much longer periods. This is exactly why simply marking your calendar for 120 days is a risky business strategy.

Does My Payment Processor Set Its Own Time Limits?

This is a huge point of confusion, and getting it wrong is costly. Your payment processor—whether it's Stripe, PayPal, or another gateway—does not set the customer's deadline to file a dispute. That’s the card network's job.

However, your processor absolutely sets its own, much shorter, deadline for your response.

It works like this: Visa might give you 30 days to submit your evidence, but your processor will demand it from you in 7, 10, or 15 days. Why? They build in a buffer for their own internal paperwork and to make absolutely sure they don't miss the final network deadline.

Your only job is to obey the deadline you see in your processor's dashboard. Miss it, and you automatically lose the dispute, no matter how solid your evidence is. The revenue is gone.

How Do Chargeback Alerts Affect These Timelines?

This is where you get to take back control. Chargeback alerts from services like Ethoca and Verifi let you sidestep these frantic deadlines completely by giving you a heads-up before a dispute is formally filed.

Here’s the simple breakdown:

- A customer calls their bank to question one of your charges.

- Instead of launching a chargeback, the bank sends an alert through the network.

- You get a notification and have a short 24-72 hour window to just refund the customer.

By issuing the refund, you stop the chargeback cold. It never gets filed, you never have to scramble to gather evidence, and most importantly, it never damages your all-important chargeback ratio. It’s the difference between firefighting and fire prevention. You can dive deeper into these strategies on the Disputely chargeback prevention blog.

What Is the Difference Between a Chargeback Time Limit and a Statute of Limitations?

It's easy to mix these two up, but they operate in completely different worlds.

- A chargeback time limit is an internal industry rule created by private companies (Visa, Mastercard, etc.). It’s their playbook for handling disputes between banks and merchants.

- A statute of limitations is an actual law passed by a government that sets the deadline for filing a lawsuit in a court of law.

These two timelines are not connected. In theory, a customer could be too late to file a chargeback but still have time to sue you. In practice, for most small consumer transactions, that's incredibly rare. For your day-to-day operations, the chargeback time limit is the one that really matters.

Stop letting complex timelines and sudden disputes dictate your cash flow. Disputely gives you the power to prevent chargebacks before they happen with real-time alerts. Connect your payment processor in minutes and automate your refund process to protect your merchant account and secure your revenue. Take control of your disputes today by visiting https://www.disputely.com.