Your Merchant Guide to the Visa Acquirer Monitoring Program

The Visa Acquirer Monitoring Program, or VAMP, is Visa's way of keeping an eye on merchants who have a bit too much fraud and too many customer disputes. Think of it as a health check for your payment processing. If your business crosses certain thresholds, it raises a red flag, and that’s when penalties start to kick in. The whole point is to protect the Visa network by making sure both merchants and their payment processors are pulling their weight.

What is the Visa Acquirer Monitoring Program?

Picture Visa as the guardian of a massive, bustling marketplace. In this market, VAMP acts as the set of community guidelines that every shop owner (merchant) needs to follow to keep things safe and trustworthy for shoppers. If one shop starts having a lot of problems—say, repeated theft (fraud) or a constant stream of unhappy customers (disputes)—the market guardian has to step in.

But this isn't just about coming down on merchants. It's about spotting risky patterns before they get out of hand and shake everyone's confidence in the system. VAMP also holds the merchant's financial partner, their acquirer, responsible for helping manage that risk. To really get a handle on VAMP, you have to first understand the role of merchant acquirer banks in this whole ecosystem.

A New, Unified Approach to Risk

The VAMP we see today is a big step up from how Visa used to handle risk. For years, they ran two separate programs:

- Visa Dispute Monitoring Program (VDMP): This program focused only on customer disputes, better known as chargebacks.

- Visa Fraud Monitoring Program (VFMP): This one zeroed in on the amount of reported fraudulent transactions.

Having two separate buckets was clunky. A merchant could be squeaky clean on the fraud side but drowning in disputes, or the other way around. This siloed approach made it tough to see the complete risk picture.

To give you a better sense of this evolution, here’s a quick breakdown of the old vs. the new.

VAMP at a Glance Key Program Changes

| Aspect | Old Programs (VFMP & VDMP) | New Program (VAMP) |

|---|---|---|

| Structure | Two separate programs for fraud and disputes. | A single, consolidated program. |

| Evaluation | Merchants were monitored against separate fraud and dispute thresholds. | Merchants are evaluated using a single, unified metric. |

| Focus | Addressed fraud and disputes as distinct issues. | Provides a more holistic view of merchant risk. |

| Simplicity | More complex for acquirers and merchants to track and manage. | Simplified monitoring and enforcement process. |

This consolidation means that Visa is now looking at your business through a single, wider lens, giving them a much clearer, more accurate picture of your overall risk.

In April 2025, Visa combined the VDMP and VFMP into the single Visa Acquirer Monitoring Program. The move was a direct response to rising fraud in online, card-not-present sales, with the goal of tackling four times more fraud and potentially saving over $2.5 billion in global losses each year.

For any business operating online, where "card-not-present" is the norm, getting a handle on this new, combined formula is critical. The only way to steer clear of the hefty fines and restrictions that VAMP brings is to be proactive. If you're wondering where you stand, our guide on how a Q4 audit can help you stay ahead of these compliance thresholds is a great place to start. You can check it out here: https://disputely.com/campaign/q4-audit.

How Visa Calculates Your Merchant Risk Score

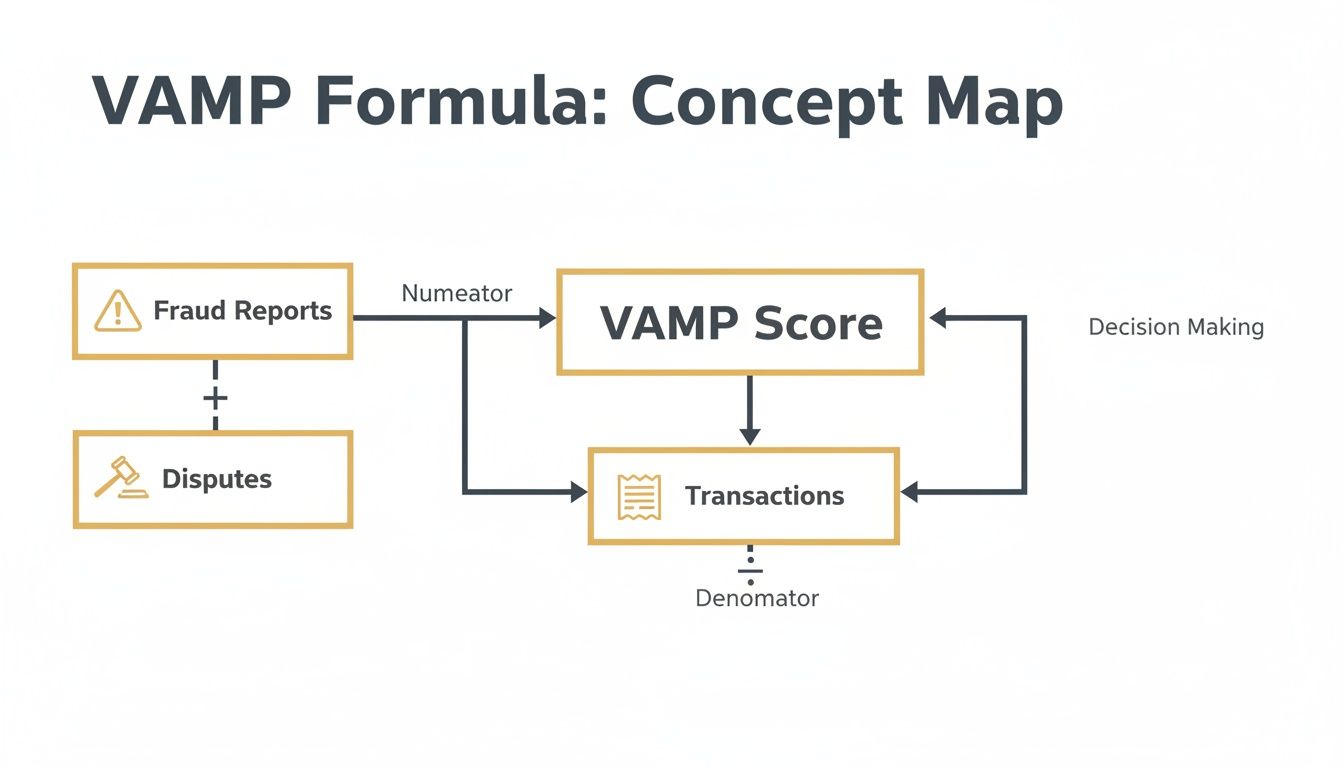

To steer clear of the Visa Acquirer Monitoring Program (VAMP), you've got to get a handle on the math behind it. Think of it this way: Visa acts like a credit bureau for merchants, using a specific formula to generate a "risk score" that grades your business. Luckily, it’s not some black-box algorithm—it's a straightforward calculation based on your monthly transactions.

At the heart of your VAMP score is one key formula:

(Fraud Reports + Total Disputes) ÷ Total Transactions = Your VAMP Ratio

This simple equation takes two of the most critical negative signals—TC40 fraud reports and all customer disputes (chargebacks)—and measures them against your total sales for the month. It gives Visa a single, clear number to gauge the health of your merchant account.

The Double-Counting Problem

Here’s where things get tricky—and frankly, a bit frustrating for merchants. A major flaw in this formula is the potential for double-counting. This happens when a single fraudulent transaction gets flagged twice, once as a fraud report and again as a dispute.

Imagine a fraudster buys something from you with a stolen card. The real cardholder notices the charge, calls their bank to report the fraud, and also files a dispute to get their money back. In Visa's system, that one bad sale just created two separate strikes against you. This quirk can quickly inflate your VAMP ratio, pushing you toward the penalty box even though it was just one incident.

Double-counting is a serious vulnerability for merchants. It means one fraudulent order can hit your VAMP ratio twice, making it absolutely essential to have a proactive strategy that stops fraud before it becomes a dispute.

This is why just reacting to chargebacks as they come in isn't a sustainable strategy. You have to get ahead of the problem.

The VAMP Thresholds You Can't Ignore

Visa has drawn some very clear lines in the sand to define what's acceptable versus what's considered excessive risk. Crossing these lines is what gets you officially enrolled in the VAMP.

Here are the main thresholds every merchant needs to know:

- Minimum Activity: To even be on the VAMP radar, you need to have at least 1,500 combined fraud and non-fraud disputes in a single month. This is designed to keep very small businesses from being penalized for a handful of isolated incidents.

- VAMP Ratio Threshold: This is the number that really matters. For merchants in North America, the EU, and Asia Pacific, the "excessive" threshold is 1.5%. If your ratio climbs past that mark, your acquirer gets a notification, and you're in the program.

These aren't suggestions; they are hard-and-fast rules enforced across the entire Visa network.

Card-Testing Attacks and the Enumeration Ratio

Beyond standard fraud, VAMP has a laser focus on shutting down card-testing attacks, also known as enumeration. This is a common tactic where fraudsters bombard a merchant's payment gateway with tiny transactions, testing thousands of stolen card numbers to see which ones still work.

To fight this, Visa rolled out a separate metric: the enumeration ratio. This is especially critical for businesses that process a high volume of transactions. VAMP's monitoring for this is incredibly strict, targeting card-testing with a 20% ratio for merchants processing under 300,000 monthly transactions. This initiative is powered by Visa's VAAI system, which has been shown to cut false positives by 85%. The rollout began on April 1, 2025, with full enforcement hitting major global markets on October 1. You can learn more about how Visa is tackling enumeration attacks and what it means for your business.

The thresholds for these attacks are set at two levels:

- Standard Level: This is triggered at 5,000 blocked enumeration transactions or a 5.00% rate.

- Excessive Level: Things escalate quickly here, with a trigger at 50,000 blocked enumeration transactions or a 10.00% rate.

These specific rules make it clear: Visa is serious about stopping card-testing at the source. If your systems aren't effectively blocking these attacks, you'll find yourself under the VAMP microscope in no time.

The True Cost of a VAMP Violation

Tripping the wire on Visa's Acquirer Monitoring Program isn't just a slap on the wrist. It’s a direct hit to your company's financial health and stability, setting off a chain reaction of penalties that can strangle your revenue and sour your relationship with your payment processor.

The first and most obvious hit comes from direct financial penalties. Once your acquirer gets the notice that you’ve crossed the VAMP line, they'll start passing Visa's escalating monthly fines straight down to you. These aren't just one-and-done fees; they are recurring charges that get steeper the longer you're stuck in the program, systematically eating away at your profits.

But the fines you see on your statement are just the beginning. The real damage often comes from the hidden costs lurking beneath the surface.

Beyond the Fines: The Operational Damage

Landing in the Visa Acquirer Monitoring Program essentially puts a "high-risk" sign on your back for the entire payments world to see. This new reputation carries heavy operational consequences, chief among them being a sudden, sharp drop in your transaction approval rates.

For high-risk merchants, especially those in ecommerce or running subscription models, the fallout can be brutal. With full VAMP enforcement kicking in October 2025, Visa has reported that acquirers in the program already see up to 10% fewer approved transactions than their compliant counterparts. This drop directly cuts into the revenue of any merchant whose acquirer's portfolio goes over the 0.5% threshold. You can dig into the specifics in Visa's VAMP updates and their impact on merchants.

Why does this happen? It all comes down to increased scrutiny. Your acquirer, now feeling the heat from Visa, will likely tighten their risk filters for your account. This means more of your legitimate customer transactions get flagged and declined as "false positives."

The moment you enter VAMP, your payment processing becomes less reliable. A 5% to 10% decline in approval rates can translate into tens of thousands of dollars in lost monthly revenue, derailing growth forecasts and frustrating loyal customers.

This is the simple but powerful formula Visa uses to calculate your risk, weighing your fraud reports and disputes against your total transactions.

As you can see, every single fraud report and dispute pushes your ratio higher, inching you closer to the threshold with each incident.

From Frozen Funds to Account Termination

The heightened scrutiny doesn't just stop at transaction declines. To protect themselves, your payment processor will probably take more drastic defensive measures. This can look like a few different things:

- Higher Rolling Reserves: Your processor might start holding back a bigger chunk of your revenue—think 10% or more—for an extended period of 90-180 days. This is to cover any potential future chargebacks, but it also ties up your working capital, making it tough to manage cash flow, pay vendors, or reinvest in your business.

- Frozen Funds: In more serious cases, your acquirer could freeze your account altogether. All incoming money is held while they conduct a formal risk review, which can bring your operations to a screeching halt overnight.

- Account Termination: This is the absolute worst-case scenario. If you can't get your metrics under control and exit the program in time, your acquirer may simply cut ties and terminate your merchant account. Losing your primary payment processor is a catastrophic event, as finding a new one willing to take on a business labeled "high-risk" is incredibly difficult and almost always more expensive.

To put it plainly, a VAMP violation is not a problem you can afford to ignore. It is a five-alarm fire for your business, demanding a swift and strategic response to protect your revenue and your very ability to operate.

To give you a clearer picture of how this unfolds, here’s a breakdown of the typical enforcement stages and what you can expect at each level.

VAMP Violation Tiers and Associated Penalties

| Violation Stage | Timeline | Acquirer Action | Potential Merchant Fines |

|---|---|---|---|

| Notification | Month 1 | The acquirer is notified by Visa. The acquirer then informs the merchant and provides resources to create a remediation plan. | Warning; no fines yet, but the clock is ticking. |

| Early Warning | Months 2-4 | Acquirer must submit a detailed remediation plan to Visa. Increased monitoring of the merchant's account begins. | Acquirer may pass on penalties starting at $25,000/month. |

| Enforcement | Months 5-7 | If thresholds are still exceeded, Visa imposes higher fines. The acquirer may implement stricter processing limits or higher reserves. | Acquirer penalties can escalate to $50,000/month or more. |

| Termination Risk | Month 8+ | Visa may disqualify the acquirer from processing for the merchant. The acquirer is highly likely to terminate the merchant account. | Fines can reach $100,000+ per month, plus the devastating cost of account closure. |

As the table shows, the consequences build quickly. What starts as a warning can spiral into a business-ending event in just a few months if left unaddressed.

Your Step-by-Step VAMP Remediation Playbook

Getting hit with a Visa Acquirer Monitoring Program (VAMP) notification feels like your whole operation is suddenly under a microscope. It’s Visa’s way of pulling you over on the payment processing highway, with fines looming and scrutiny at an all-time high. But it’s not a dead end. Think of it as a mandatory pit stop—a clear signal that you need a solid plan to get back in the race.

Panic won't help. What you need is a methodical playbook to figure out what's causing your high dispute and fraud ratios, fix the underlying problems, and prove to your acquirer that you’ve corrected course. This is your guide to doing just that and getting out of VAMP for good.

The first move isn't about technology or data; it's about people.

Get on the Phone with Your Acquirer—Now

In this scenario, your acquiring bank isn't your enemy. They're actually your most important ally. Visa holds them responsible for your numbers, so believe me, they are just as motivated as you are to get this sorted out. The moment you get that VAMP notification, you need to be proactive and open a line of communication.

Don’t sit back and wait for them to dictate the terms. Get a call on the calendar and come prepared to be completely transparent about the situation. The goal here is to work together on an official, written remediation plan that can be submitted to Visa.

This plan absolutely needs to cover:

- The exact steps you’re taking to bring down disputes and fraud.

- A realistic timeline for putting these changes into action.

- The specific metrics you'll use to measure success.

Putting this in a formal document shows both your acquirer and Visa that you're taking this seriously and have a structured, professional approach to solving the problem.

Become a Detective: Dig Into the Root Causes

You can't fix a problem you don't truly understand. A high VAMP ratio is just a symptom; your job is to find the disease. It’s time to conduct a deep-dive root cause analysis on your chargeback and fraud data to find out what’s actually going wrong.

Start slicing and dicing your dispute data. Are the chargebacks clustered around a specific product? A certain marketing campaign? A particular country? When you start looking for patterns, the culprits often jump right out.

Some of the most common hidden causes we see are:

- Mysterious Billing Descriptors: If customers see a charge they don't recognize on their statement, their first call is to the bank to dispute it.

- Sneaky Policies: Is your subscription renewal policy buried in the fine print? Is canceling a service a huge hassle? This is a recipe for "friendly fraud."

- Shipping Bottlenecks: When products don't show up on time, "merchandise not received" disputes are sure to follow.

- Frustrating Customer Service: If a customer can't easily get in touch with you for a refund, they'll simply bypass you and file a chargeback.

This kind of analysis is non-negotiable. It turns your remediation plan from a series of wild guesses into a targeted, data-backed strategy.

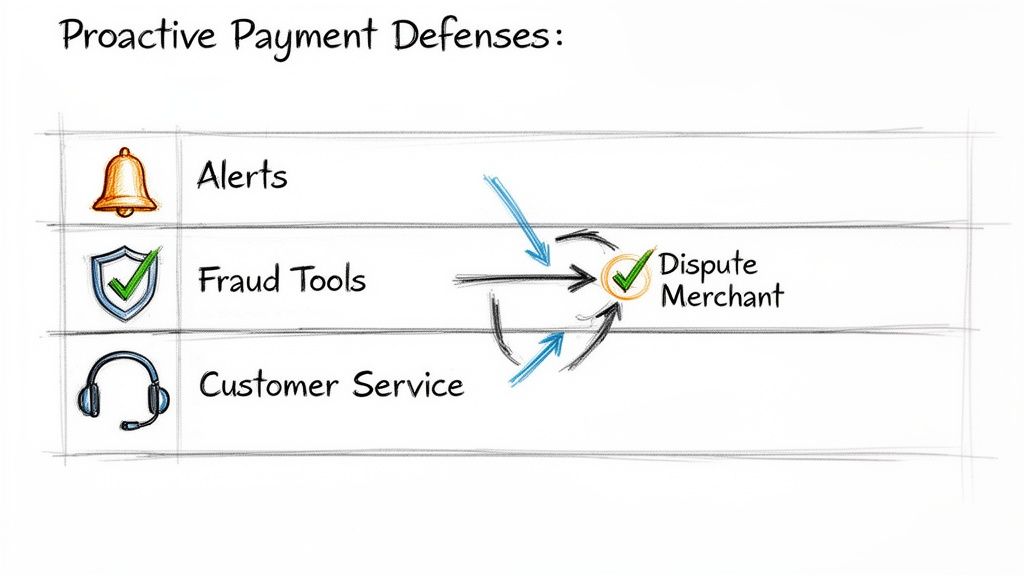

Stop the Bleeding with Pre-Dispute Prevention

While you work on fixing the big-picture issues, you have to stop the immediate damage. This is where pre-dispute prevention tools become your most valuable asset. Technologies like chargeback alerts and Visa’s own Rapid Dispute Resolution (RDR) can step in and resolve a customer complaint before it ever becomes a formal chargeback that dings your VAMP ratio.

It's basically an early-warning system. A customer contacts their bank to complain, and an alert is fired off directly to you. This opens up a critical 24-72 hour window for you to issue a full refund and automatically resolve the problem. The dispute is deflected, and your VAMP numbers are safe.

Solutions that integrate with Visa RDR, such as Disputely, are essential for VAMP remediation. They act as an automated safety net, deflecting disputes in real-time and providing the immediate ratio relief needed to get below program thresholds.

Getting these quick wins is crucial for showing your acquirer that you're making progress. It buys you the breathing room you need to implement the deeper, more permanent fixes you identified in your analysis.

Monitor, Report, and Adjust Your Game Plan

Getting out of VAMP isn't a "set it and forget it" task. Once your plan is rolling, you have to become obsessed with your numbers. Track your dispute ratio, fraud rate, and alert volume every single day.

Share your progress with your acquirer consistently—a weekly report is a great way to build trust and prove you're making real headway. And be ready to adjust your strategy. If one change isn't moving the needle, pivot. Maybe that new billing descriptor is still causing confusion, or maybe you need to tighten up your fraud filters even more.

This constant cycle of monitoring and reporting is the final piece of the puzzle. It provides the hard evidence Visa and your acquirer need to see, showing them you’ve solved the underlying problems and are ready to graduate from the Visa Acquirer Monitoring Program for good. For merchants who want to sharpen their evidence-gathering skills, learning how to build a strong case for Q4 chargebacks can provide some great insights into what makes for effective representment.

How to Stay Off Visa’s Radar and Avoid VAMP Altogether

The best way to deal with the Visa Acquirer Monitoring Program (VAMP) is to never end up in it in the first place. While having a remediation plan is critical if you get flagged, a strong, proactive defense is infinitely better for your bottom line and your sanity. This isn't about one magic fix; it's about building a multi-layered system to stop disputes before they ever start and to intelligently fight the ones that are just plain wrong.

Think of it like securing your home. You don't just count on a good front door lock. You have motion-sensor lights, maybe a security camera, and a noisy alarm system. Each layer serves a different purpose, but together, they create a formidable defense. Your merchant account deserves the same level of protection.

A truly proactive approach focuses on nipping disputes in the bud, making it ridiculously easy for customers to talk to you instead of their bank, and using modern tools to head off trouble before it escalates.

Harness the Power of Chargeback Alerts

If there's one tool that can single-handedly save you from VAMP, it's a chargeback alert platform. These services are your early-warning system, giving you a heads-up the moment a customer calls their bank to complain about a charge.

That notification kicks off a critical 24-72 hour window. It's your golden opportunity to issue a refund and solve the customer's problem before it officially becomes a chargeback. The dispute is deflected, and it never touches your VAMP ratio. It’s the difference between hearing a smoke alarm and seeing the fire department at your door—one gives you a chance to act, while the other means the damage is done.

Platforms like Disputely tie directly into bank-level networks, including Visa’s Rapid Dispute Resolution (RDR), to make this whole process automatic. This real-time defense is your first and best line of protection against runaway dispute counts.

Optimize Your Customer Touchpoints

So many disputes, especially the "friendly fraud" kind, are born from simple confusion or frustration. A few straightforward tweaks to your customer-facing information can wipe out a surprising number of these chargebacks.

Start with your billing descriptor—that little line of text on a customer's credit card statement. If it's vague or doesn't match your brand, customers won't recognize it and will jump to the conclusion that it’s fraud.

- Make it Recognizable: Your descriptor needs to scream your business name. Use something clear like "DISPUTELY.COM" instead of a generic parent company name like "PAYMENT SVCS INC."

- Include Contact Info: Add a phone number or a support URL right in the descriptor. This gives customers a direct line to you for questions, cutting off a call to their bank at the pass.

Beyond the descriptor, make your customer service impossible to miss. Your website needs a clear "Contact Us" or "Support" link in both the header and footer. If a customer can find your phone number, email, or live chat in seconds, they're far more likely to come to you for a solution.

A huge chunk of chargebacks stem from basic confusion. When you make your billing descriptor and customer support crystal clear, you eliminate the friction that pushes a frustrated customer to file a dispute.

Getting this foundation right lowers the number of disputes you have to deal with, period. That's a win for your whole system. It's not uncommon for merchants to have their funds frozen by processors like Shopify because of high dispute rates; you can learn more about how to resolve a Shopify payment hold while putting these preventative measures in place.

https://disputely.com/shopify-hold

Leverage Advanced Fraud Prevention Tools

Chargeback alerts are fantastic for handling customer service-related disputes, but you still need a heavy-duty fraud filter to stop criminal fraud before a transaction ever goes through. Tools like Visa Account Attack Intelligence (VAAI) are built specifically to sniff out and block card-testing attacks and other nasty fraud patterns. As part of a comprehensive approach to mitigating risks, acquirers can implement robust application monitoring practices to ensure system stability.

By integrating modern fraud tools, you can:

- Block Enumeration Attacks: Stop fraudsters from using your site to test lists of stolen card numbers, which keeps you from triggering VAMP's strict enumeration thresholds.

- Reduce TC40 Fraud Reports: A smart fraud tool kills bad transactions on sight, which means fewer TC40 reports filed against your merchant account.

- Prevent Double-Counting: By blocking fraud at the source, you avoid the nightmare scenario where one fraudulent transaction becomes both a TC40 report and a chargeback, hitting your VAMP ratio twice.

Fight Smarter with Compelling Evidence 3.0

Finally, you shouldn't just roll over and refund every dispute. When you get a chargeback that you know is bogus—like a customer claiming non-delivery when you have a signed proof of delivery—you need to fight it.

Visa's Compelling Evidence 3.0 (CE3.0) initiative actually gives merchants a better shot at winning these friendly fraud battles. The program allows you to submit specific evidence, like IP address matches and previous transaction history, to prove a charge was legitimate. Winning these representments doesn't just get your money back; it helps scrub your dispute history clean.

By combining these layers—proactive alerts, clear communication, powerful fraud prevention, and intelligent representment—you build a complete defense system that keeps your business safe, stable, and far away from the Visa Acquirer Monitoring Program.

Got Questions About VAMP? We’ve Got Answers.

When you're trying to make sense of the Visa Acquirer Monitoring Program, a few key questions always come up. It can feel like a maze of rules and ratios, but getting straight answers is the first step to protecting your business.

We've broken down the most common VAMP questions we hear from merchants. Let's clear the air so you can focus on what you do best.

Does VAMP Only Apply to Online Sales?

Yes, for the most part. The Visa Acquirer Monitoring Program is designed specifically for card-not-present (CNP) transactions. Think of all your online sales, mail orders, and any payments you take over the phone.

VAMP was created to keep an eye on the higher risk that comes with e-commerce and other remote payment channels. When a customer physically taps or swipes their card in your store, those transactions don't count toward your VAMP ratios.

How Can Visa RDR Keep Me Out of the Program?

Visa's Rapid Dispute Resolution (RDR) is your best line of defense against VAMP. It's a system that lets you automatically refund a customer's transaction the moment they try to start a dispute with their bank.

The magic is that any dispute resolved this way is never counted as an official chargeback. So, it never hits your VAMP calculation.

Think of RDR as a circuit breaker for disputes. It stops the problem before it can escalate into a full-blown chargeback that dings your record. By deflecting these issues in real-time, you can keep your dispute rate well below the VAMP danger zone.

Tools like Disputely make this completely hands-off by automating the RDR process, ensuring you’re always protected without lifting a finger. It’s a simple, effective way to avoid the massive headaches that come with landing in the Visa Acquirer Monitoring Program.

What is Double-Counting and Why is it So Bad for My VAMP Ratio?

Double-counting is a nasty quirk in how VAMP works, and it can seriously mess up your numbers. It happens when a single fraudulent order gets flagged twice: once as a TC40 fraud report by the customer's bank, and again as a customer dispute (a chargeback).

When this happens, Visa’s system counts both events against you. You’re essentially getting penalized twice for the same transaction.

This can quickly inflate your VAMP ratio, pushing you toward the monitoring thresholds much faster than you’d expect, even if your actual fraud volume isn’t that high. It’s a perfect example of why you have to get ahead of fraud before it happens.

I’m a Small Business. Do I Really Need to Worry About VAMP?

Absolutely. While it’s true that VAMP has a minimum volume requirement (you need at least 1,500 combined fraud and non-fraud disputes in a month), you’re not off the hook just because you're small.

Remember, your acquirer (your payment processor) is watching their own numbers. They have to keep their entire merchant portfolio under a 0.5% VAMP ratio. If your account—even a small one—starts generating a lot of disputes, you become a risk to them.

They won't hesitate to put you under review or even terminate your account to protect their own standing with Visa. Smart dispute management is crucial for every business, no matter its size.

Stop letting chargebacks threaten your business. With Disputely, you can automatically resolve disputes before they ever hit your merchant account, keeping your ratios low and your payment processor happy. See how much you could save and protect your revenue by visiting https://www.disputely.com today.