What Is a Bank Chargeback and How Can You Prevent It?

A bank chargeback is what happens when a customer sidesteps you entirely and goes straight to their bank to dispute a transaction on their card statement. It’s a forced reversal of funds, yanking the money right out of your merchant account.

This isn't like a refund, where you and the customer sort things out. A chargeback is a formal process, and it often feels like you're presumed guilty until proven innocent.

What a Bank Chargeback Really Means for Your Business

Let's walk through a common scenario. A customer buys something from your online store. A few weeks later, instead of asking you for a return, they call their credit card company and say they never authorized the purchase.

Just like that, their bank pulls the money from your account and hands it back to them as a "provisional credit." On top of losing the sale, you're hit with a separate, non-refundable chargeback fee.

While this system was created to protect consumers from genuine fraud, it's become a major headache for honest merchants. You lose the revenue, you're out the product you shipped, and you have to pay a penalty for the trouble. This isn't a small problem, either. Global chargeback volume is projected to hit a staggering 337 million cases by 2025—that's a 27% jump from 2022. You can dig deeper into these chargeback statistics to grasp the full scale of the issue.

The Key Players Involved

To really understand what a bank chargeback is, you have to know who's in the room when it happens. It's never just a simple back-and-forth between you and your customer. There's a whole cast of characters, each with their own part to play.

Think of a chargeback less as a single action and more as a slow, formal relay race. The baton gets passed from the cardholder to their bank, then to your bank, and finally to you—all under the strict rules of card networks like Visa and Mastercard.

This chain of communication is precisely why the process feels so bureaucratic and takes so long to resolve. Let's break down who these key players are and what they actually do.

Key Players in the Chargeback Process

| Player | Role in the Process |

|---|---|

| Cardholder | The customer who made the purchase. They start the whole process by calling their bank to dispute the charge. |

| Issuing Bank | This is the cardholder's bank (think Chase, Bank of America, etc.). They issue the card, give the customer a provisional credit, and officially file the chargeback against you. |

| Acquiring Bank | This is your bank, the one that provides your merchant account. They're the ones who receive the chargeback notice and pull the funds from your account. |

| Merchant | That's you! You're the one who has to decide whether to accept the loss or fight back by submitting evidence to prove the transaction was legitimate. |

Each of these players has a distinct responsibility, and understanding their roles is the first step toward navigating the dispute process effectively.

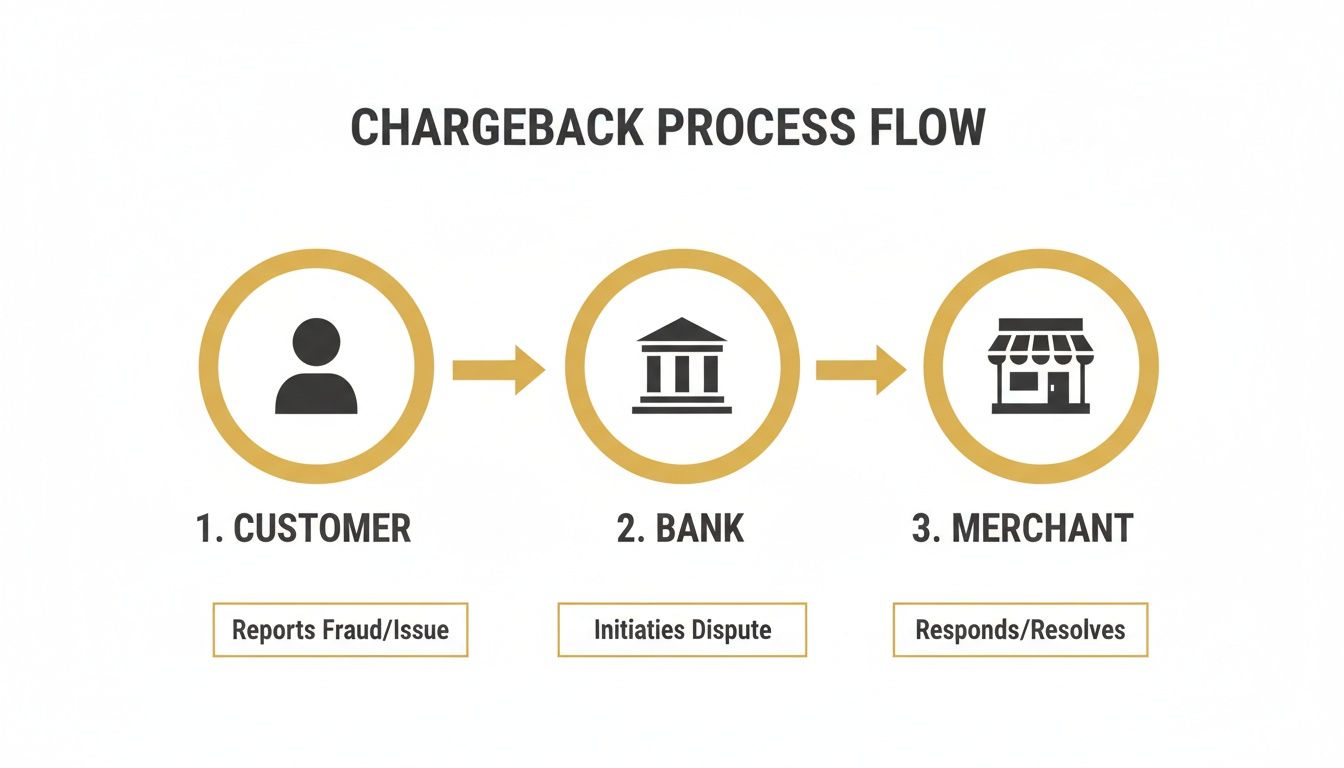

Mapping the Bank Chargeback Journey

A chargeback isn't a single event; it's a journey. It’s a slow, formal process that kicks off with a customer's complaint and, if you're not careful, ends with money being pulled directly from your account. Think of it as an official chain of communication, where each step adds another layer of time and complexity. Knowing how this journey unfolds is the first step to figuring out how—and when—to step in.

It all starts the moment a cardholder picks up the phone or logs into their banking app to question a charge. That one action sets off a domino effect, pulling in everyone from the card networks (like Visa and Mastercard) to your own payment processor.

This flow diagram breaks down the typical path a chargeback takes, from that initial customer complaint all the way to the final resolution.

As you can see, the information moves in one direction, which is why the merchant is almost always the last to know. That built-in delay is a huge problem because the clock is already ticking.

The Cardholder Kicks Things Off

It all begins with your customer. They might not recognize a charge, claim they never received their order, or simply have a case of buyer's remorse. Whatever the reason, they contact their own bank (the issuing bank) to dispute the transaction on their statement.

The bank takes a look at the claim and matches it to an official reason code. Let's be honest, they almost always give their customer the benefit of the doubt and green-light the chargeback.

Right away, the customer often gets a provisional credit. The bank temporarily puts the money back into their account while the "investigation" happens, making them feel like the problem is solved.

The Dispute Snakes Through the System

Once the issuing bank files the chargeback, it sends the request through the card network—think Visa, Mastercard, or Amex. The network acts like a switchboard, routing the dispute over to your bank (the acquiring bank).

Your acquiring bank gets the notice, immediately yanks the disputed amount from your merchant account, and slaps on a separate chargeback fee. This fee can be anywhere from $15 to $50, sometimes even more.

Here's the kicker: The money is gone from your account before you've even had a chance to tell your side of the story. You're effectively treated as guilty until proven innocent.

Only after all of this has happened are you, the merchant, finally notified. This notification can show up days, or even weeks, after the customer first made the complaint. You're already behind, and a strict countdown begins—you typically have just 20 to 45 days to gather your evidence and fight back.

Why Your Customers Are Filing Chargebacks

To get a handle on chargebacks, you have to get inside your customer's head. People don't file disputes out of the blue; something always sets it off. These triggers generally fall into one of three buckets, and knowing which one you're dealing with is key to figuring out how to stop it from happening again.

The reason could be a simple, honest mistake on your part, or it could be straight-up criminal activity. But most of the time, the truth is a bit murkier, blurring the line between a real problem and a customer just wanting their money back. Getting to the bottom of these drivers is the first real step in building a solid defense.

Merchant Error and Simple Mistakes

Let's be honest: sometimes, it's our fault. These are often the easiest chargebacks to prevent because they come from things like confusing policies, a communication breakdown, or a simple operational slip-up. A customer might file a dispute just because they felt like they had no other way to get your attention and solve their problem.

Common examples of merchant error include:

- Unrecognizable Billing Descriptors: The customer checks their statement and sees a charge from "SP*PRODUCTSINC" instead of your store's name. They don't recognize it and immediately assume it's fraud.

- Poor Customer Service: The customer reaches out for help, but your support team is slow, unhelpful, or just plain unresponsive. A chargeback becomes their last resort.

- Unclear Policies: Your refund or shipping policies are hidden in the fine print or written in confusing legal jargon. When a customer's expectations aren't met, frustration leads to a dispute.

- Shipping or Fulfillment Delays: The package shows up weeks late. The customer, feeling ignored or misled, disputes the charge.

Criminal Fraud

This is the classic scenario most people imagine when they hear "chargeback": a thief using a stolen credit card. When this happens, the real cardholder is the victim, and the chargeback is the right tool for them to get their money back. As a merchant, trying to win these disputes is a lost cause.

Your goal here isn't to fight the chargeback itself, but to stop the fraudulent purchase from ever going through. This is where strong fraud detection tools are non-negotiable. If you're running into issues, you might find our guide on how to deal with a Shopify payment hold helpful for protecting your store.

A fraudster uses a stolen credit card to buy a high-ticket item from you. The actual cardholder spots the charge, reports it to their bank, and a chargeback is filed. You're out the product, the money, and you get slapped with a fee. It’s a total loss.

The Challenge of Friendly Fraud

Here it is—the most common, and by far the most maddening, reason for a chargeback. Friendly fraud is when a real customer makes a perfectly legitimate purchase, receives the product, and then disputes the charge anyway.

They might claim they don't recognize the transaction, have a sudden case of buyer's remorse, or they might just be gaming the system to get a free product.

This isn't a rare occurrence; it's an epidemic. Friendly fraud can make up a staggering 70% of all disputes. What's even more painful is that merchants only win about 45% of the friendly fraud cases they decide to fight. You can dig into more of these eye-opening chargeback trends and their impact on businesses to see the full picture. This is precisely why proactive tools are so critical—they can help you resolve a customer's issue long before it turns into a damaging chargeback on your record.

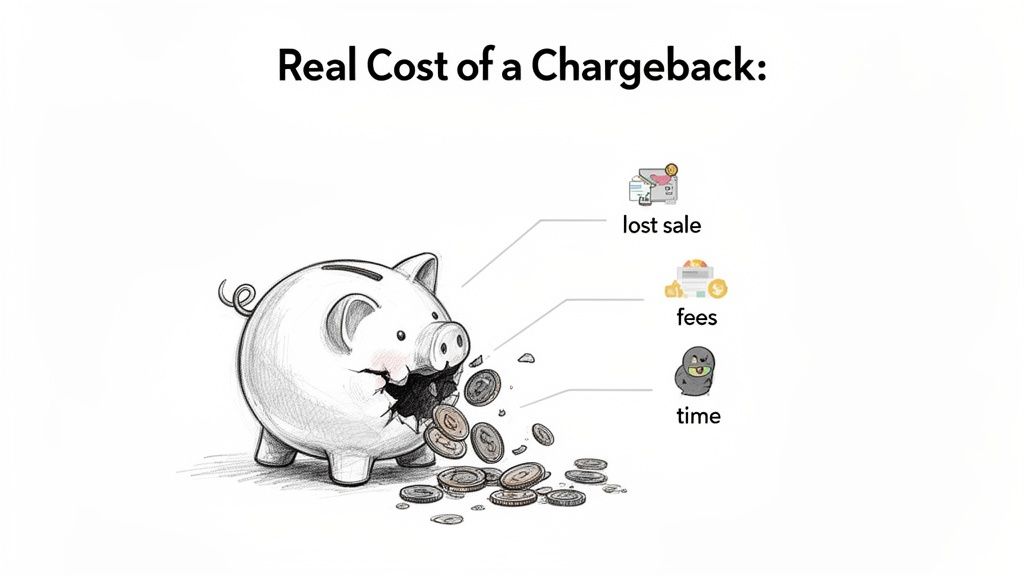

Calculating the Real Cost of a Chargeback

When a chargeback hits your account, it's easy to fixate on the lost sale. You see a disputed $50 purchase and think, "Okay, I lost $50." But that's a dangerously simple way to look at it. The real financial gut punch from a single bank chargeback is much, much worse.

This isn’t just about one bad transaction; it's a snowball of hidden costs and operational headaches that make that initial sale amount look like pocket change.

Unpacking the Hidden Financial Damage

To truly understand what’s at stake, you have to look beyond the obvious. The real cost of a bank chargeback is a messy mix of direct hits and indirect expenses that pile up fast.

Here are the most immediate hits to your bottom line:

- The Original Transaction Amount: The entire sale value is gone. Poof.

- The Lost Product: Your merchandise is usually gone for good, with no chance to resell it.

- The Chargeback Fee: On top of everything else, your payment processor slaps you with a penalty fee—typically $15 to $50 per dispute—and you have to pay it even if you win.

But believe me, the financial bleeding doesn't stop there. Several other factors come into play that really amplify the damage.

The True Cost Formula

Here’s a rule of thumb I’ve seen hold true for years: for every dollar you lose to a chargeback, your business actually loses far more. The widely accepted industry calculation is that the true cost is 2 to 3 times the original transaction value.

For a $100 transaction, a chargeback doesn't cost you $100. It costs you closer to $250. This formula accounts for lost product, marketing spend, operational overhead, and processor fees.

This multiplier effect is where the real danger lies. Just a handful of disputes can completely wipe out the profits from dozens of legitimate, successful sales. It’s a threat to your entire financial stability. To see how you can manage these costs predictably, check out Disputely's straightforward chargeback alert pricing.

And this isn't just a small business problem; it's a massive global issue. A 2025 analysis from Mastercard shows that while a dispute might cost a bank around $9 to $10, the impact on merchants like us is far more brutal once you factor in the lost revenue and administrative time.

Globally, chargeback values are set to explode from $33.8 billion in 2025 to $41.7 billion by 2028. U.S. merchants are getting hit especially hard, facing the highest average chargeback value of $110. They're projected to lose an astonishing $170 billion annually from fraud and misuse alone. You can dig deeper into the numbers by reading about the true costs of chargebacks in 2025.

Your Game Plan for Fighting Chargebacks

When that chargeback notification hits your inbox, it's easy to see it as a lost cause. But just accepting every bank chargeback as an automatic loss is a surefire way to drain your profits.

With the right game plan, you can absolutely fight back and win. Better yet, you can learn how to avoid the fight altogether.

The traditional path is called representment. This is your formal chance to "re-present" the transaction to the cardholder's bank. You're essentially building a case file, complete with compelling evidence, to prove the original charge was completely valid.

Think of it as your day in court. But be warned—the clock is ticking. Miss the deadline, which is typically 20 to 45 days, and you automatically lose the dispute and the money.

Building Your Case with Compelling Evidence

To win a representment, you need to directly shut down the customer's claim. A generic response just won't work. Your evidence needs to tell a crystal-clear story of a legitimate transaction, leaving the issuing bank with no doubt.

Here's the kind of proof that builds a rock-solid case:

- Proof of Delivery: Shipping confirmations are your best friend, especially for "product not received" claims. A "delivered" status with the customer's matching address is golden.

- Customer Communications: Dig up any emails, chat logs, or support tickets. Did the customer ask a question about their order? Did they confirm they got it? It's all evidence.

- Transaction Data: This is the digital fingerprint. AVS (Address Verification System) and CVV match results, paired with the customer’s IP address and a transaction timestamp, prove the cardholder was there.

- Order and Product Details: Invoices and clear descriptions of the purchased items are crucial for fighting "not as described" claims.

The entire strength of your case rests on the quality of your evidence. A single signed delivery receipt or an email from the customer saying, "Thanks, I got it!" is often all it takes to win the dispute.

The Modern Strategy: Sidestepping the Fight Entirely

Winning a representment feels great, but it’s not a complete victory. That chargeback still dings your dispute ratio, and you'll never see that processing fee again. This is why the smartest play is to stop a dispute from ever becoming an official chargeback in the first place.

This is exactly what chargeback alerts are for. A service like Disputely plugs directly into the card networks and notifies you the moment a customer starts a dispute. This opens a critical 24-72 hour window for you to act.

Instead of gearing up for a fight, you simply refund the customer. The refund stops the dispute process cold before it gets filed. It's a proactive move that turns a potential battle into a simple, clean resolution.

To learn more about putting together a winning response, you can check out our guide to winning chargeback representment.

While you still lose the sale, you completely dodge the hefty chargeback fee, protect your merchant account's good standing, and save yourself from the time and stress of the representment process.

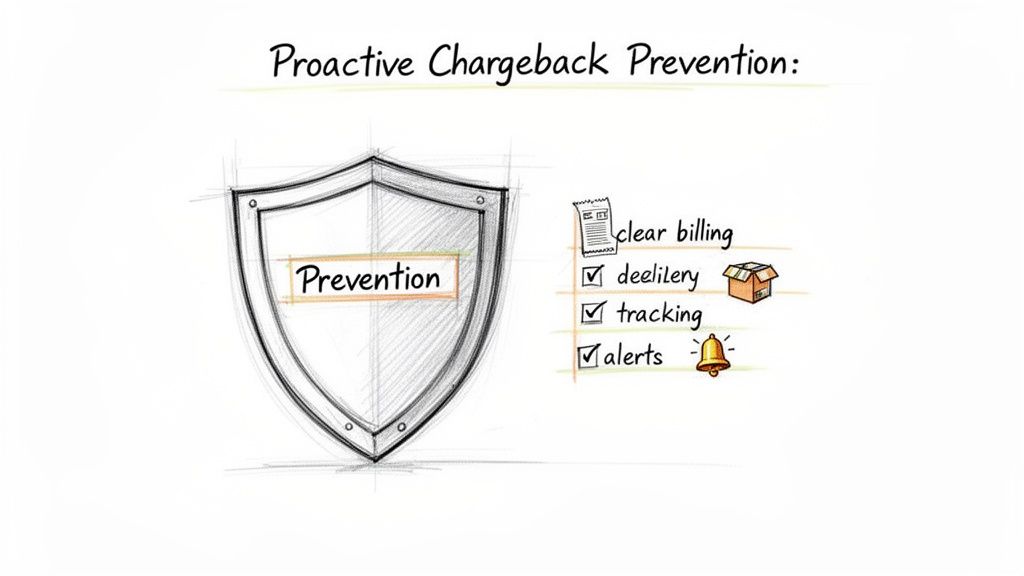

How to Proactively Prevent Chargebacks

When it comes to chargebacks, the best defense is a good offense. Instead of just reacting when a dispute hits your account, the most effective strategy is to stop it from ever happening in the first place. This means building a business foundation that gets ahead of the common root causes of disputes.

One of the simplest yet most powerful things you can do is focus on clarity. Are your refund, return, and shipping policies buried in fine print, or are they front and center? Ambiguity is a chargeback's best friend. When customers are confused, they're much more likely to just call their bank.

Strengthen Your Customer Service

Think of your support team as your first line of defense. When a customer can easily connect with a helpful person, they’ll almost always try to solve the problem with you directly. Making your support accessible and responsive is a game-changer. Consider what the top customer support companies do to keep their customers happy and you'll see a pattern of easy, direct communication.

Another huge, and often overlooked, trigger for disputes is the billing descriptor. If a customer looks at their credit card statement and sees a cryptic charge like "SP*PRODUCTSINC" instead of your actual store name, their first thought is fraud. Make sure your descriptor is crystal clear and immediately recognizable.

Key Takeaway: Proactive prevention isn't about getting rid of every single dispute—that's impossible. It's about eliminating the ones that are entirely preventable. By focusing on clear communication, stellar service, and the right tools, you can slash the number of chargebacks caused by friendly fraud and simple merchant errors.

The numbers tell a stark story. While 40% of businesses aim for a chargeback rate under 0.1%, fewer than 20% ever hit that target. This is where modern tools like real-time chargeback alerts make all the difference. They give you a heads-up the moment a customer initiates a dispute, offering a small window to issue a refund and stop the issue before it escalates into a formal, damaging chargeback. This simple step saves you from fees, protects your all-important dispute ratio, and turns a potential battle into a quick, painless resolution.

Common Questions About Bank Chargebacks

Let's wrap things up by tackling some of the most common questions merchants have about the whole chargeback ordeal. Getting a solid grasp on these fundamentals is the first step to handling disputes with confidence.

What Is the Difference Between a Chargeback and a Refund

Think of a refund as a handshake. It's a straightforward agreement between you and your customer where you willingly give their money back. It's often a sign of good faith and part of great customer service.

A bank chargeback, on the other hand, is more like a forced eviction. It’s a payment reversal kicked off by the customer's bank, pulling you into a formal process with card networks and acquiring banks. This not only costs you extra fees but also hurts your business's health by driving up your dispute ratio.

How Long Do I Have to Respond to a Chargeback

Once a chargeback is officially filed, you generally have a window of 20 to 45 days to fight back. The exact timeline depends on the card network—Visa, Mastercard, etc.—and the specific reason for the dispute.

But here’s the critical part: that 45-day clock is for reacting to a problem. Modern alert systems give you a much shorter, but far more valuable, window of 24-72 hours to issue a simple refund and stop the dispute before it ever hits your record as a chargeback.

Jumping on that early window is your single best move to protect your merchant account.

Can I Prevent All Chargebacks

Aiming to prevent 100% of chargebacks is, unfortunately, a losing battle. You'll always have to contend with determined fraudsters. However, you absolutely can prevent the vast majority of them.

By combining top-notch customer service with clear, upfront policies and smart tools like real-time dispute alerts, you can slash your chargeback rate. These strategies are especially powerful for heading off friendly fraud and simple customer mix-ups before they spiral into damaging, expensive disputes.

Stop losing revenue to preventable disputes. Disputely integrates with Visa and Mastercard to alert you in real-time, giving you the power to refund a customer and avoid chargebacks entirely. Protect your business with Disputely today.