What is a bank identification code: A guide to secure international payments

A Bank Identification Code (BIC) is the banking world's equivalent of a postal code. It’s a standard format code that financial institutions use to identify a specific bank anywhere in the world, making sure international payments land in the right place. You’ll often hear it called a SWIFT code—they're the same thing.

Decoding Your Bank Identification Code

Ever wondered how your money zips across oceans and continents to land in the correct account? The magic behind that is the Bank Identification Code (BIC). It acts as a precise address, guiding funds to the right bank. For any business that sends or receives money internationally, understanding the BIC isn't just helpful; it's absolutely critical.

Think about sending a package without a zip code. It would probably get delayed, lost, or sent right back to you. The same logic applies to a BIC in a financial transaction. An incorrect or missing code can cause a cascade of problems that hit your bottom line.

- Payment Delays: The funds can get stuck in limbo for days, or even weeks, as banks manually try to figure out where the money is supposed to go.

- Extra Fees: When a payment goes astray, intermediary banks often charge for their time and effort to redirect it. These fees are usually just deducted from the amount being sent.

- Failed Transactions: Worst-case scenario? The payment gets rejected outright and bounced back to the sender, which is a terrible experience for a customer waiting on a payment or refund.

For an ecommerce merchant, these issues are more than minor headaches. A refund that fails because of a bad BIC can quickly escalate into a customer dispute or a costly chargeback. Getting this code right from the start is a simple step that prevents lost funds, protects your revenue, and keeps your international operations running like a well-oiled machine.

Breaking Down the BIC and SWIFT Code Structure

A Bank Identification Code might look like a random string of characters at first glance, but it’s actually more like a highly specific postal code for your money. Think of it as a precise global address, with each part of the code telling the financial system exactly where to send a payment.

This system is the backbone of international finance. With over 40,000 live SWIFT codes in use around the world, this standardized format (known officially as ISO 9362) is what allows a bank in Tokyo to talk to a bank in Toronto without any confusion.

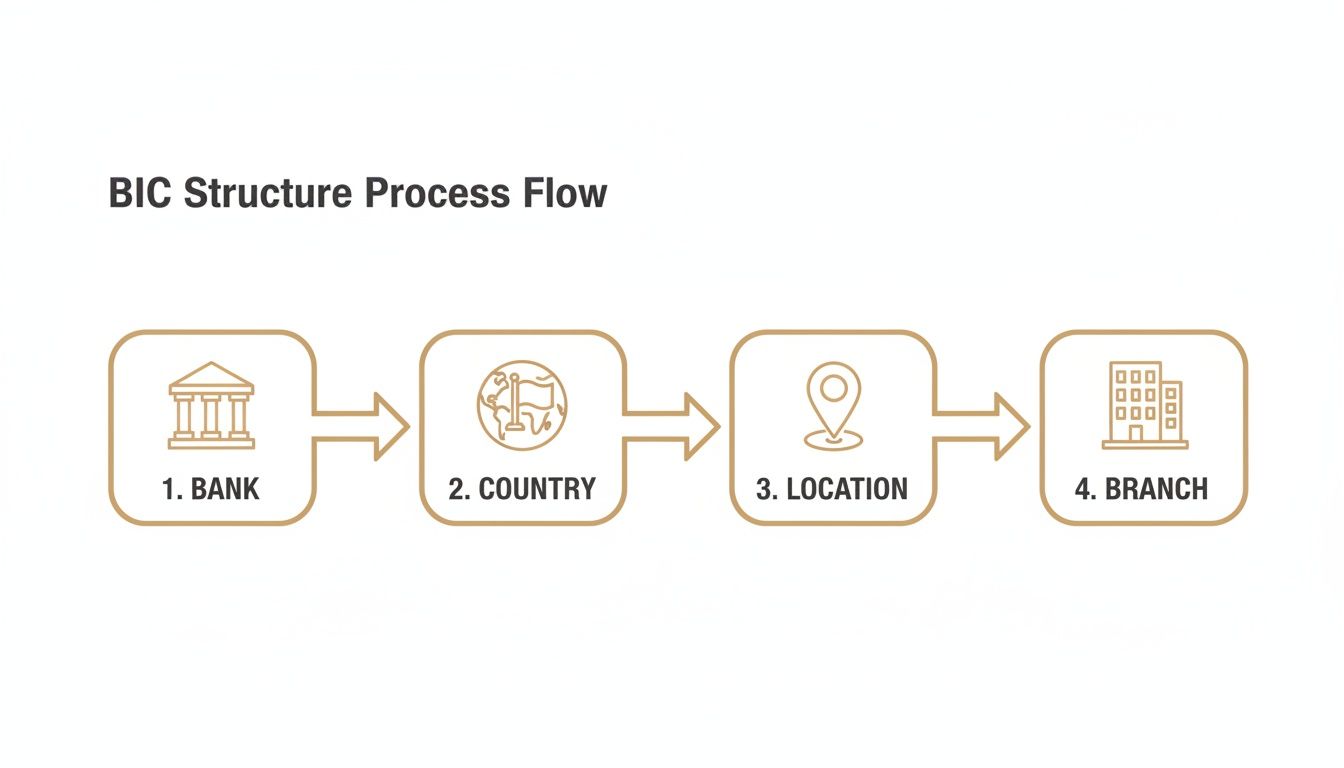

The Anatomy of a BIC

Every BIC, whether it's 8 or 11 characters long, is packed with information. Each little piece of the code has a job to do.

The diagram below shows you how a standard 11-character BIC is put together.

As you can see, the code is made of four distinct parts that zero in on the destination, starting broad and getting more specific.

A simple way to remember the structure is: Bank > Country > City > Branch. It’s a logical trail that guides your transaction from anywhere in the world to one specific bank counter.

Let's look at a real-world example to see how it works. We'll use the BIC DEUTDEFF500.

- DEUT (Bank Code): These first four letters are unique to the financial institution. Here, 'DEUT' is the identifier for Deutsche Bank.

- DE (Country Code): The next two letters tell us the country, based on the standard ISO 3166-1 alpha-2 list. 'DE' is the code for Germany.

- FF (Location Code): These two characters point to the city or region where the bank is based. In this case, 'FF' stands for Frankfurt.

- 500 (Branch Code): This last three-digit piece is optional and specifies a particular branch. If you see 'XXX' here, or if the code is only 8 characters long, it just means the payment is headed for the bank's main headquarters.

So, an 8-character code like DEUTDEFF would send money to Deutsche Bank's head office in Frankfurt. But the 11-character version, DEUTDEFF500, routes it to a very specific branch. Understanding this structure is key to seeing how the whole system works, especially when you consider what a SWIFT payment is and the role these codes play.

How BICs Power International Payments

Think of a Bank Identification Code (BIC) as the global postal code for money. When you send a package internationally, you need a precise address. It's the same for sending funds across borders—the BIC tells the financial system exactly which bank, in which country, and even which specific branch your money needs to reach.

Without this code, an international payment is lost in transit. Your bank uses the recipient's BIC to plot the most efficient route through a network of correspondent banks. These intermediary banks act like layover airports, passing your money along until it lands safely in the right account. It’s a highly coordinated handoff, and the BIC is the playbook.

This diagram shows how each piece of the code works together to create that unique financial address, guiding funds from the institution level right down to the local branch.

As you can see, the code is structured logically. It starts broad with the bank's identity and country, then narrows down to a specific city and branch. Simple, yet incredibly effective.

The Cost of a Wrong Turn

So, what happens if you get the BIC wrong? For an ecommerce business operating globally, even a single incorrect character can turn a simple transaction into a costly mess. It’s like sending a package to the wrong city—it’s going to cause problems.

Here’s what you can expect when a BIC is invalid:

- Rejected Payments: The transfer will likely fail and bounce back, often with processing fees deducted by every bank that touched it along its failed journey.

- Serious Delays: Your money could get stuck in limbo for days or weeks while banks try to manually sort out where it was supposed to go.

- Lost Funds: In a worst-case scenario, the funds can end up in a general suspense account, making recovery a long and frustrating ordeal.

For an online merchant, a failed refund due to an incorrect BIC is a direct path to a chargeback. The customer, not receiving their money, is likely to dispute the charge, turning a simple refund into a much more damaging and expensive problem.

This is why BIC validation isn't just a "nice-to-have." It’s an essential part of your payment process. Getting it right every time saves money, prevents customer frustration, and keeps your international operations running smoothly.

Why BICs Matter for Ecommerce and Chargeback Prevention

For anyone running an online store, a Bank Identification Code is far more than just a jumble of letters and numbers. Think of it as a critical piece of your revenue protection toolkit. While its main job is to make international payments happen, its real value becomes crystal clear when things go sideways—specifically with refunds and payment disputes.

A simple typo in a BIC can quickly escalate a routine refund into a full-blown customer service meltdown, often ending in a chargeback.

Picture this: a customer wants their money back. You start the refund process, but the BIC is wrong. The money gets lost in transit, and as far as the customer is concerned, you've broken your promise. Frustrated, they file a chargeback, which hits your business much harder than the original refund ever would. Using the correct BIC from the start ensures that money lands in the right account, cutting off this all-too-common chargeback trigger at the source.

This kind of accuracy is the bedrock of good dispute management. When a dispute does occur, the BIC is like a direct phone line, making sure every message and every dollar moves correctly between your payment processor and the customer's bank.

Making Dispute Resolution Smoother

Knowing exactly which bank you're dealing with is the first step to resolving any dispute. Using the right Bank Identification Code guarantees your evidence and any fund transfers go straight to the correct institution, no detours allowed. This simple act speeds up the whole process, cutting down on the manual work and administrative headaches for your team.

The official standard for BICs, ISO 9362, includes codes for banks on the SWIFT network and "non-connected" codes used for reference. For disputes, using the correct connected BIC is what matters. It routes everything to the right place, shrinking processing times from days down to a matter of hours. You can find more detail on BIC and SWIFT bank codes on gocardless.com.

This efficiency is especially important for subscription businesses, where payment failures can quickly inflate dispute ratios and land you in costly monitoring programs with Visa and Mastercard.

A smooth refund and dispute process is essential for keeping your merchant account in good standing. By preventing payment failures from bad BICs, you're directly lowering your dispute ratio and reducing the risk of your processor putting a hold on your funds.

In the end, getting BICs right isn't just a technical detail. It's about building a solid payment system that protects your bottom line, keeps customers happy, and helps you steer clear of the painful consequences of too many chargebacks—like the dreaded Shopify Payments hold.

How to Find and Verify a Bank Identification Code

Finding a Bank Identification Code isn't usually difficult, but getting it right is absolutely critical. A simple typo can derail a transaction, leading to frustrating delays, extra fees, or even a complete rejection. For a business, this can turn a routine payment or customer refund into a real headache.

The best place to find a BIC is straight from the source. Check a recent bank statement or log in to your online banking portal—it's almost always listed there. You can also typically find it on the bank's official website, often in a section dedicated to international payments or wire transfers.

Securely Validating Your BIC

Got the code? Great. Now, take a moment to verify it before you hit "send." Online BIC validation tools are fantastic for this, but you have to be smart about how you use them.

These checkers cross-reference the code against the official ISO 9362 standard, instantly confirming that the bank, country, and location details match up. The catch? Scammers sometimes create fake validation sites to phish for sensitive financial data.

To stay safe, stick to these simple rules:

- Never enter a full account number. A real validation tool only needs the BIC to do its job.

- Avoid sites that ask for personal details. There's no reason a BIC checker would need your name, address, or password.

- Use well-known, reputable services. Stick to established financial information providers you trust.

For companies with an eye on global markets, getting these details right is part of the process. For example, knowing how to open a bank business account in UAE means getting familiar with their specific banking identifiers from day one.

Crucial Tip: Always double-check the BIC a customer or supplier gives you. A quick confirmation email can save you from the high cost and hassle of a failed transfer and a potential dispute.

If you run into trouble with payments or need help navigating disputes that stem from these kinds of errors, feel free to reach out to our dedicated support team for assistance.

Frequently Asked Questions About BICs

Even when you've got a handle on the basics of a Bank Identification Code, a few common questions still tend to pop up. Let's clear up the details around BICs, IBANs, and what happens when things go wrong.

Are BIC and SWIFT Codes the Same Thing?

For all practical purposes, yes. Think of SWIFT code as a specific brand of BIC. It’s the type of BIC that connects a bank to the huge SWIFT network, which is the system banks use to securely message each other about money transfers.

While every SWIFT code is a BIC, not every BIC is a SWIFT code. But in the real world, when a form asks you for a BIC to make an international payment, they're almost certainly asking for the bank's SWIFT code.

What Is the Difference Between a BIC and an IBAN?

Here’s a simple way to think about it: imagine you're mailing a package to a friend who lives in a massive apartment complex. The BIC is the street address of the building, while the IBAN is your friend's specific apartment number.

- BIC (Bank Identification Code): This code identifies the correct bank.

- IBAN (International Bank Account Number): This one pinpoints the specific account at that bank.

You absolutely need both for a payment to land in the right place. The BIC gets the money to the right financial institution; the IBAN makes sure it hits the right person's account. Miss one, and the payment will likely fail.

A helpful analogy is that the BIC is like the city and zip code, while the IBAN is the street address and apartment number. Both are required for precise delivery.

What Happens If I Use the Wrong BIC Code?

Punching in the wrong Bank Identification Code can set off a chain reaction of problems, from a simple delay to a major financial headache. It affects both the sender and the person waiting for the money.

For starters, your payment will almost certainly be delayed. We're talking days, sometimes even weeks, as banks along the way try to figure out the mistake. If they can't sort it out, the transaction gets rejected and the money is sent back—minus any fees the intermediary banks charged for their time.

For an ecommerce merchant, this is a recipe for an unhappy customer. A refund that fails because of a bad BIC can quickly turn into a chargeback, which is a much bigger, more expensive problem for your business. To get ahead of these issues, take a look at our guide on chargeback representment strategies.

Protect your business from costly chargebacks before they happen. Disputely integrates directly with Visa and Mastercard to alert you to disputes in real-time, giving you the chance to refund and avoid the chargeback entirely. Learn how Disputely can save your merchant account.